Following Bank Negara Malaysia’s July 2025 OPR cut to 2.75 per cent, 2026 presents a timely opportunity to refinance your home loan. Discover the benefits, costs, risks, and step-by-step process of home loan refinance in Malaysia, from lowering repayments to accessing equity wisely.

Refinancing, or more precisely, how to refinance housing loans, is on many Malaysian homeowners’ mind in 2026. With the recent cut in the overnight policy rate (OPR), combined with shifting property values and evolving bank offers, now could be a favourable time to review your existing housing loan.

Before you dive in, note that refinancing means replacing your existing home loan with a new one, often from another bank under new terms. The goal may be to reduce monthly repayments, shorten tenure, access equity, or switch loan type.

What Has Changed & Why Now Is a Key Moment

In July 2025, Bank Negara Malaysia (BNM) reduced the Overnight Policy Rate (OPR) from 3.00 per cent to 2.75 per cent.

Because most home loans, including floating‑rate and many Islamic financing products, are linked to base rates derived from the OPR, this cut has had a ripple effect across the property finance market. Banks promptly adjusted their base rates downward, making borrowing more affordable.

For many homeowners, understanding how to refinance housing loan now means lower monthly repayments or the opportunity to secure better terms, especially if your current loan has a high interest rate or long tenure.

Consequently, 2026 offers a timely window to explore home loan refinance Malaysia options seriously, whether you want to ease your monthly cash flow, reduce your interest burden, or tap into your home’s equity.

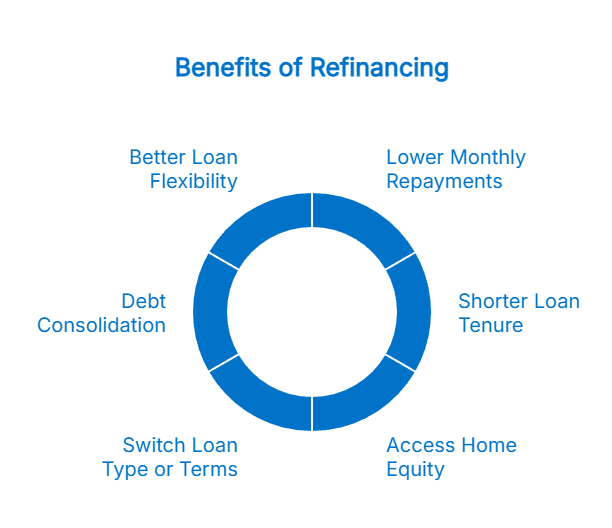

Why Refinance a Home Loan: Potential Benefits

Refinancing can serve different financial goals. Here are the main advantages you may unlock by understanding how to refinance housing loan and taking the time to do it carefully:

- Lower Monthly Repayments: If your new loan comes with a lower interest rate, you may pay less each month, freeing up cash for other expenses or investments.

- Shorter Loan Tenure: Refinancing may allow you to shorten the tenure, meaning you pay off your home loan faster and save on total interest over the loan’s life.

- Access Home Equity (Cash‑out Refinance): If your property value has appreciated, refinancing may let you borrow beyond the outstanding loan, giving you cash to fund renovations, education, investments, or simplify other debts.

- Switch Loan Type or Terms: You might want to move from a fixed‑rate loan to a variable‑rate loan (or vice versa), or convert conventional financing to Islamic financing (or the reverse), depending on your preference.

- Debt Consolidation or Financial Re‑structuring: In some cases, homeowners use refinancing to combine other debts (e.g. personal loans, credit card debts) under a single lower‑cost home loan, simplifying repayments and potentially saving on total interest.

- Better Loan Flexibility or Features: Newer loan packages might offer flexibility such as semi‑flexi or flexi options, redraw facilities, or better prepayment features, which may not have been available when you first took the loan.

Refinancing is not a one‑size‑fits-all solution, but when you understand how to refinance housing loan for the right reasons and under the right conditions, it can be a powerful financial move.

Make informed decisions for your next home with property guidesTypes of Refinance Options in Malaysia

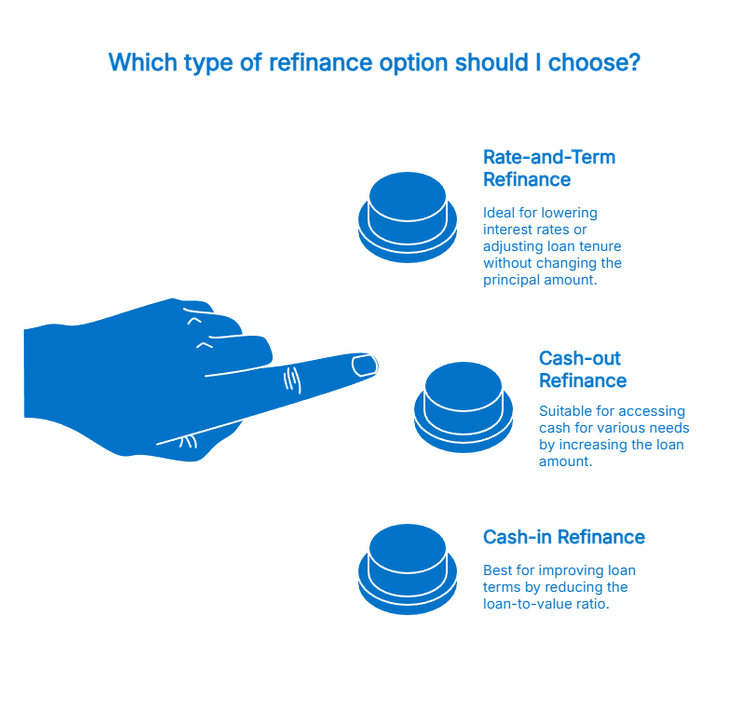

When you decide to refinance housing loan, you need to understand the kind of refinancing available. Common types of home loan refinance Malaysia options include:

- Rate‑and‑Term Refinance: Replace the current loan with one having a lower interest rate or different tenure while the principal remains roughly the same.

- Cash‑out Refinance: Based on the current property valuation, you refinance for a higher amount than the outstanding loan and receive the difference as cash. Useful if you need funds for renovation, investment, or other financial needs.

- Cash‑in Refinance: You pay in a lump sum towards the principal before refinancing. Banks might offer better rates or terms when the loan-to-value ratio improves.

Each option carries different implications for cash flow, total interest over time, and financial flexibility, so understanding how to refinance housing loan can help you choose according to your long-term financial goals.

What You Should Consider Before Refinancing

Refinancing can be advantageous, but only if done with full awareness of costs, obligations, and personal circumstances. Before you refinance, knowing the options for home loan refinance Malaysia will help you carefully weigh the following factors:

- Lock‑in Period and Early‑Exit Penalties: Many home loans come with a lock‑in period (commonly three to five years). Exiting or refinancing before this period may trigger an exit penalty of 2–5 per cent on the outstanding loan amount.

- Refinancing Costs (Moving Costs): Expect charges for valuation, legal fees, stamp duty, disbursement fees, new sale and purchase agreement (SPA), and possibly new home insurance or Mortgage Reducing Term Assurance (MRTA). These costs typically amount to around 2–3 per cent of the loan amount.

- Debt Service Ratio (DSR) and Eligibility: Your ability to refinance depends on your current debt commitments, income, credit profile and outstanding loan balance. Banks will review your ability to service the new loan under DSR guidelines.

- Property Value and Equity: A rising property value improves the potential amount you can refinance for (especially for cash‑out), provided your outstanding loan and loan-to-value ratio permit.

- Type of Interest Rate (Fixed vs Variable): If you switch to a variable rate, your repayments will fluctuate with future rate changes. Fixed rates offer stability but may have higher initial costs. When exploring home loan refinance Malaysia, consider which rate type aligns best with your financial goals and risk tolerance.

- Break-even Period (Long-term Cost vs Short-term Benefit): Calculate how long it will take for savings from lower repayments to offset refinancing costs. Refinancing may not make financial sense if you plan to move out or sell soon.

- Total Loan Tenure and Interest Cost: Extending the loan tenure may reduce monthly amounts but increase total interest paid over time. Be clear on your long-term repayment and financial goals.

Understanding all costs, risks, and benefits is crucial before making a decision. By learning how to refinance housing loan and exploring home loan refinance Malaysia options, you can make an informed choice that aligns with your financial goals. Careful planning ensures refinancing works to your advantage, whether for lower repayments, shorter tenure, or accessing equity.

Explore newly launched properties across MalaysiaStep-by-Step Guide: How to Refinance Housing Loan in 2026?

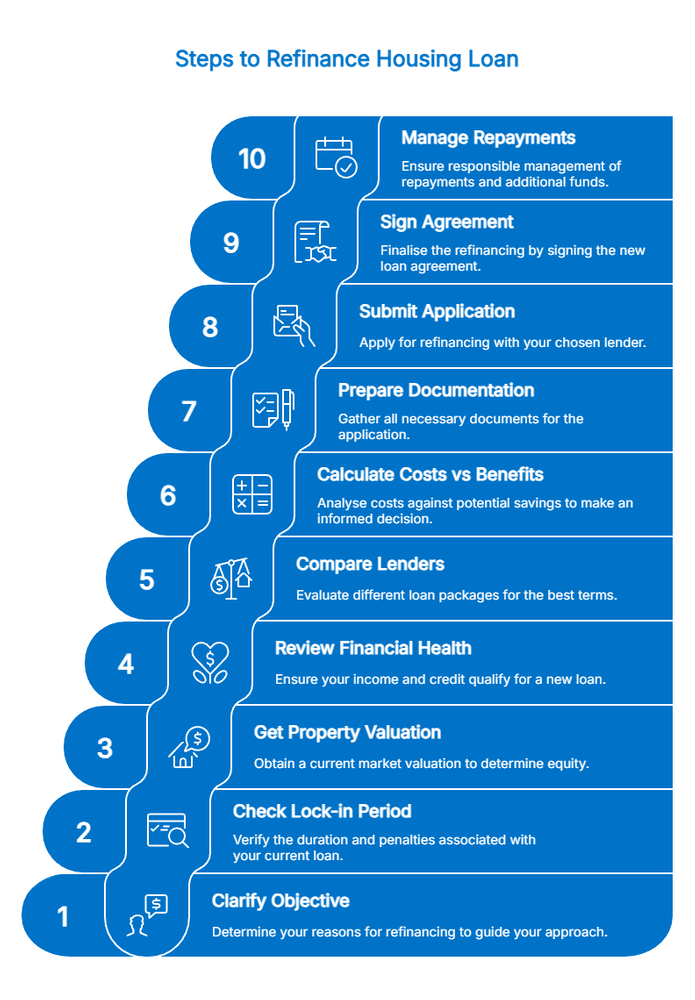

Thinking of refinancing? Follow this practical, step‑by‑step guide on how to refinance housing loan to make the process smoother and more effective. By understanding each stage clearly, you can save time, reduce costs, and make informed decisions for your home loan.

- Clarify Your Objective

Decide why you want to refinance. Are you after lower monthly repayments, shorter tenure, extra cash, or switching loan type or terms? This clarity will guide your approach. - Check Your Loan’s Lock‑in Period

Review your original loan agreement. If you are still within the lock‑in period, calculate whether the exit penalty and costs justify refinancing. - Get a Current Market Valuation of Your Property

Request a formal valuation or estimate the market value using recent transacted prices in your area. This helps determine your equity and potential loan-to-value ratio. - Review Your Financial Health: Credit History, Income & DSR

Ensure your income, existing debts, and credit record qualify you for a new loan. Banks will verify your debt servicing ability before approval. - Compare Multiple Lenders and Loan Packages

Do not settle on the first offer. Compare interest rates (fixed vs variable), fees, flexibility (prepayment, redraw), and loan tenure options. - Calculate Costs vs Benefits (Break-even Analysis)

Factor in all costs, including valuation, legal fees, stamp duty, processing fees, and any early‑exit penalties, and compare them against your potential monthly savings or cash‑out amount. - Prepare Required Documentation

Gather necessary documents such as National Registration Identity Card (NRIC), recent payslips or bank statements, existing loan statements, Sale and Purchase Agreement (SPA), property title/Memorandum of Transfer (MOT), and any insurance or additional financing paperwork. - Submit Application to New Bank / Lender

Once you select a suitable package, submit your refinancing application. The bank will likely order a property valuation, conduct credit and eligibility checks, and then process approval. - Sign New Loan Agreement and Complete Legal Formalities

After approval, sign the agreement (often with a lawyer appointed by the bank). The new bank will settle your existing loan and disburse any remaining funds (in cash‑out cases). - Start New Repayment Schedule and Manage Cash Responsibly

If you opted for a longer tenure or cash‑out, ensure you manage repayments and the additional cash prudently.

Refinancing a property can be a strategic financial move when done carefully. By following this step‑by‑step guide, you can understand the process, evaluate costs and benefits, and make informed choices that suit your needs. For those exploring options, home loan refinance Malaysia offers a variety of packages to help you reduce repayments, shorten tenure, or access equity effectively.

Find available plots and parcels for agricultural use in MalaysiaWhen Refinancing May Not Be Worth It

Refinancing housing loan can be beneficial, but it is not always the best path. In certain situations, you may be better off continuing with your existing loan. Understanding how to refinance housing loan can help you decide better. Consider the following:

- You are still within the lock‑in period, and the early‑exit penalty is high.

- The outstanding loan amount is low, or you have little equity, refinancing may not significantly improve terms.

- You plan to sell or move property soon, refinancing costs may not be recouped.

- Extending the loan tenure may reduce monthly payments but will increase the total interest cost over time.

- If your income or debt situation worsens, refinancing could strain your future cash flow.

- Variable‑rate loan might expose you to interest rate hikes if OPR increases.

If any of these apply, a refinancing may not deliver real benefit or could even be counter-productive. Reviewing available home loan refinance Malaysia plans can help you determine whether refinancing is truly suitable for your situation.

In Summary: Should You Refinance Your Home Loan?

Deciding whether to refinance housing loan ultimately comes down to evaluating your financial goals, current loan conditions, and long-term plans. Here’s a practical summary to help you decide and explore home loan refinance Malaysia opportunities:

Refinance If:

- You can secure a lower interest rate than your current loan, which reduces monthly repayments.

- You want to shorten your loan tenure to save on total interest.

- Your property has appreciated in value, allowing for a cash-out refinance to fund other needs.

- You are looking to switch loan type (e.g., conventional to Islamic financing) or access more flexible loan features.

- Your financial health is strong, with a healthy debt-to-income ratio and good credit history.

Do Not Refinance If:

- You are still within the lock-in period, and penalties are high.

- Your loan balance is low or equity is minimal, then the benefits may not justify the costs.

- You plan to sell or move soon, then refinancing costs may not be recouped.

- Extending the loan tenure reduces the monthly repayment but increases the total interest paid significantly.

- Your financial situation is uncertain, making new monthly obligations risky.

Always perform a break-even analysis. Calculate all refinancing costs against potential monthly savings or cash-out benefits. Refinancing is most effective when it aligns with your financial strategy and long-term property goals.

By weighing the pros and cons and carefully considering your objectives, you can make a confident decision about how to refinance housing loan in 2026 and determine if it is the right move for you. Ready to plan your home financing? Use the iProperty Home Loan Calculator to estimate your monthly repayments and explore suitable loan options.