Home prices in 2026 can be confusing, especially when bank valuations differ from asking prices. This guide explains how property valuation in Malaysia works, how banks assess value, key methods used, 2026 market factors, common mistakes, and how to improve your valuation outcome.

Malaysia’s housing market saw residential property transactions rise by 7.8% year-on-year, with average prices in key areas like Kuala Lumpur increasing by 4.2%. For many prospective buyers and homeowners, understanding how home values are determined amid fluctuating prices and market dynamics can be confusing and overwhelming.

This article will clarify the key factors influencing property valuation Malaysia, demystify 2026 pricing trends, and provide practical insights to help you confidently navigate home pricing decisions.

What Is Property Valuation?

Property valuation in Malaysia 2026 is the process of estimating a property’s current market value through a detailed assessment by a certified Real Estate Agent. This process examines factors such as location, size, property condition, recent comparable sales, market demand, to determine a fair and unbiased value for buying, selling, refinancing, insurance, and taxation purposes.

Property valuation Malaysia is carried out by registered valuers accredited by the Board of Valuers, Appraisers, Estate Agents, and Property Managers (BOVAEP), using recognised methods such as the comparison approach and considering the asset’s legal, economic, and physical aspects.

Why Valuation Matters for Buyers and Owners?

Property valuation is crucial for buyers and owners because it provides a precise, impartial estimate of a property’s actual market value, helping you avoid overpaying as a buyer or underselling as an owner.

- Accurate valuation builds confidence in negotiations, ensures fair pricing, and is required by banks to secure proper financing and determine home loan amounts.

- For owners, knowing your property’s real value is key when refinancing, planning renovations, setting a competitive selling price, or calculating property taxes that depend directly on your property’s assessed value.

- By relying on professional valuations, both buyers and owners can make well-informed decisions that protect their financial interests and maximise investment returns.

How Valuation Affects Loan Approval and LTV Limits?

Valuation plays a direct role in the amount of financing a bank is willing to offer. Banks use the valuation figure, not the seller’s price, to calculate your loan amount. This is where LTV limits come in, helping banks decide the safest financing range for your property.

- For most Malaysian citizens, LTV ratios can reach 90% for first- and second-residential home loans, meaning buyers may secure financing for up to 90% of the property’s appraised value, subject to income assessment and credit checks.

- For foreign buyers, banks and lenders typically set lower LTV limits (60 to 70% of appraised value), limiting access to financing and increasing upfront cash requirements.

How Property Valuation Works in Malaysia

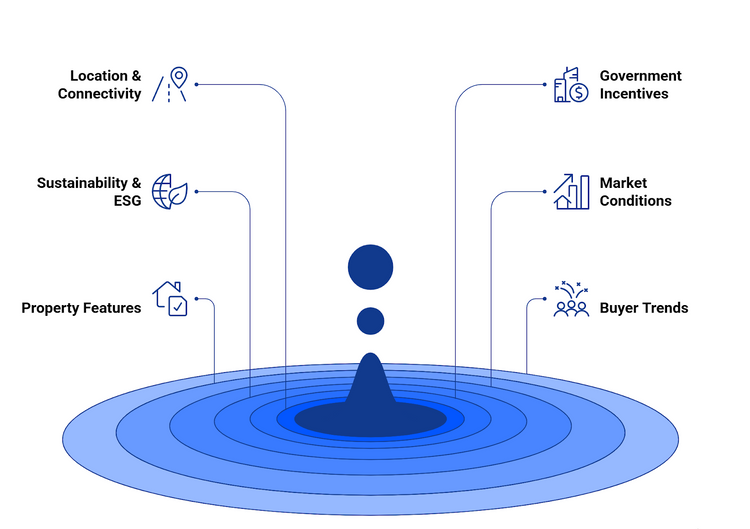

Property valuation in Malaysia involves a systematic, professional assessment grounded in the fundamentals of property valuation, determining a property’s fair market value as of a specific date, typically performed by a registered valuer. The valuer examines several key factors:

1. Location & Connectivity

Homes near major highways, new public transit lines (LRT, RTS), and business districts command higher valuations due to greater accessibility and increased demand. Developments in Klang Valley, Johor, and Penang lead in price appreciation thanks to ongoing infrastructure upgrades and their proximity to urban amenities.

2. Government Incentives & Taxes

Budget 2026 extends incentives for first-home buyers, including stamp duty exemptions for houses priced below RM500,000 until 2027, supporting continued demand in the affordable segment. Middle-income buyers gain loan interest relief for homes priced between RM500,000 and RM750,000. Conversely, foreign buyers now face double the stamp duty rate (from 4% to 8%), dampening the luxury and speculative segments and stabilising prices in premium areas.

3. Sustainability & ESG Compliance

Homes with green building features, such as solar panels, efficient cooling, water-saving fixtures, and ESG certifications, are valued higher and favoured for financing as Malaysia shifts toward sustainable urban development. Non-compliant or energy-inefficient properties risk depreciation or expensive retrofitting.

4. Market Conditions & Affordability

Interest rates (now around 4.2 to 4.4% per year) and tighter lending requirements affect affordability and buyer demographics. Properties in the RM300,000 to RM500,000 range in growth corridors remain attractive to both owner-occupiers and investors. Transaction volumes remain highest in the sub-RM500,000 segment.

5. Property Features and Supply

Size, age, renovation status, and physical condition influence valuation. New developments, repurposed commercial-to-residential conversions, and properties with hybrid workspace flexibility or enhanced security remain especially attractive in 2026.

6. Buyer Trends and Demographics

80% of Gen Z and young buyers increasingly prefer high-rise and apartment living; 70% of 2024 transactions were for units below RM500,000. Demand for homes with flexible workspaces, proximity to retail, healthcare, and reliable security continues to grow.

Check your eligibility before you apply using our eligibility calculator.How Banks Assess Your Property Before Financing

Banks in Malaysia assess your property before financing by commissioning an independent valuation carried out by a registered and qualified property valuer.

This expert examines factors such as location, property size and layout, age, condition, recent comparable sales, market demand and supply, and current economic conditions to establish the property’s fair market value.

The valuation process typically involves:

- Physical inspection of the property and review of legal/title documents.

- Use of standardised methods such as the comparison (market data) approach, cost method (land plus building cost, less depreciation), and, for income-generating properties, the investment or income approach.

- Preparation of a formal valuation report detailing the methodology, market analysis, and estimated value, which is then submitted to the bank.

The bank relies on this valuation report, not the purchase price, to set the maximum loan amount (usually up to a set loan-to-value percentage), ensuring the financing remains adequately secured and aligns with current market conditions, a key element in understanding the housing loan process.

Suppose the valuation comes in below the purchase price. In that case, buyers must top up the difference before financing is approved, ensuring the loan is adequately secured and aligns with current market conditions.

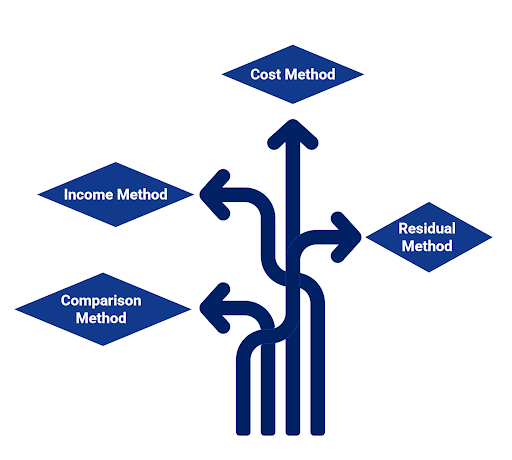

Property Valuation Methods in Malaysia

Property valuation methods in Malaysia are standardised to provide accurate and fair market values, and the principal approaches include:

1. Comparison Method

Known as the market data or sales comparison approach, this is the most widely used technique for residential and commercial properties.

The valuer analyses the sale prices of similar properties that have recently transacted in the area and makes adjustments for differences in size, condition, location, and timing. This method is preferred for resale homes, apartments, shops, and offices.

2. Income Method

Used primarily for investment properties such as offices, retail spaces, and complexes, this method assesses a property’s potential to generate rental income. It applies a capitalisation rate (or yield) to estimate its value. Subtypes include:

- Investment Method

This estimate is based on expected rental income and an appropriate capitalisation rate.

Property Value = Net Operating Income (NOI)

Capitalisation Rate

- Net Operating Income (NOI) = Annual rental income minus operating expenses (excluding finance and tax costs)

- Capitalisation Rate (%) = Required rate of return based on market evidence.

- Discounted Cash Flow (DCF) Method

This method discounts future cash flows (rents) to their present value using a discount rate.

Where:

CFₜ = Net cash flow (rental income – expenses) in year t

r = Discount rate (reflecting market risk/required yield)

n = Holding period (years)

TV = Terminal value (estimated resale value at the end of year n)

- Profit Method

Used for specialised properties (hotels, petrol stations):

Property Value = Gross Receipts − Operating Expenses − Tenant’s Share − Allowances

This method estimates value based on the business’s ability to generate profit in that location, less all costs and a reasonable return to the tenant/operator. The residue is then capitalised to obtain value.

3. Cost Method:

The valuer calculates the cost to rebuild the property (including materials, labour, and fees), subtracting depreciation for age and wear, and adding land value. This approach is suitable for unique or rarely traded properties (e.g., special buildings, public facilities).

4. Residual Method:

Applied mainly to development sites or unimproved land, this method calculates the gross development value of the completed project, subtracts development costs and profit, and discounts it to present value. It helps assess land value for future redevelopments.

Malaysia’s Standard Practice:

Valuers are mandated to comply with the Malaysian Valuation Standards set by the Board of Valuers, Appraisers, Estate Agents, and Property Managers (BOVAEP), ensuring reliability for banks, legal proceedings, and property transactions.

What Appears in a House Valuation Malaysia Report

A house valuation report in Malaysia includes comprehensive details to provide a fair and transparent estimate of property value, as required by the Malaysian Valuation Standards (MVS):

- Purpose of Valuation: The reason for the report (e.g., sale, purchase, mortgage, legal, insurance).

- Property Details: Full description including address, title, tenure, build-up area, land area, type, age, and condition.

- Valuation Date: The exact date when the inspection and valuation are conducted.

- Market Analysis: Details about the neighbourhood, location, accessibility, recent sales of similar properties, and prevailing market trends.

- Basis/Method of Valuation: States which method(s) are used (comparison, income, cost, residual, etc.) and explains why.

- Legal and Planning Details: Information on titles, tenure, zoning, and compliance with local planning requirements.

- Tenancy/Lease Info: Lists tenants, lease terms, rents, and tenancy agreements (where relevant).

- Opinion of Value: The valuer’s estimated fair market value and rationale (with calculations and adjustments made).

- Supporting Documents: Maps, floor plans, photos (internal, external, and surrounding environment), previous sale transactions, and approvals.

- Valuer’s Declaration: Name, signature, credentials, and a formal declaration of compliance with Malaysian standards.

A house valuation report provides a clear, accurate view of a property’s worth, helping all parties make informed decisions based on standardised, transparent information.

What’s Shaping Malaysia’s Property Market in 2026?

Malaysia’s property market moves toward affordability, stability, and practical value for both buyers and investors. Government support, steady demand, and sustainability-focused development continue to shape home prices nationwide.

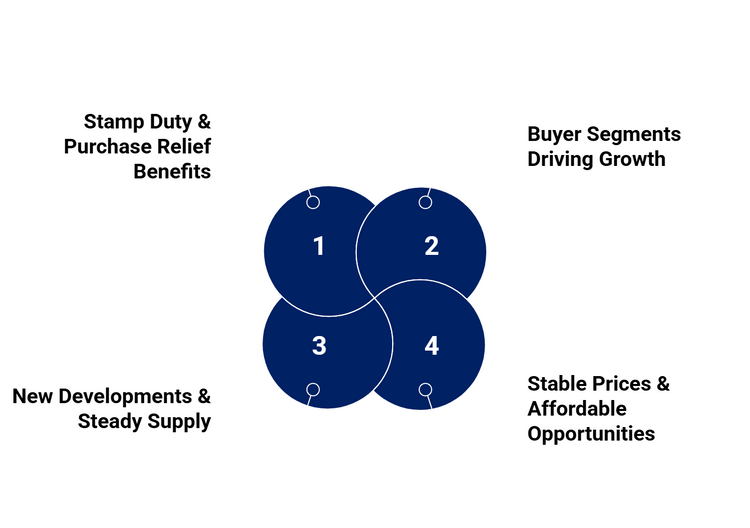

Government Support Strengthens Affordability

- Stamp duty exemptions remain for first-time buyers purchasing homes up to RM500,000.

- Buyers of homes priced between RM500,000 and RM750,000 receive purchase relief of up to RM5,000.

- These measures help eligible groups lower transaction costs by an estimated 15 to 20%.

Market Demand Focuses on Entry-Level and Mid-Market Homes

- Most residential transactions fall below RM500,000, making this segment the main driver of growth.

- Transaction volumes are expected to rise by 3 to 5% compared to 2025.

- Luxury properties see less speculative activity due to the 8% stamp duty for foreign buyers.

Supply Growth Supports Price Stability

- New housing completions and repurposed commercial spaces add a healthier supply to the market.

- These shifts help maintain stable pricing as Malaysia emphasises sustainable urban development.

- First-time buyers, young families, and upgraders enjoy improved affordability and easier access to financing.

More Predictable and Inclusive Pricing in 2026

- Market conditions remain steady, practical, and inclusive.

- Affordable homes gain strong government backing, while demand stays firm in well-connected urban areas.

- Investors benefit from a stable market with gradual appreciation in key growth corridors.

What Should Buyers Know About Home Pricing in 2026?

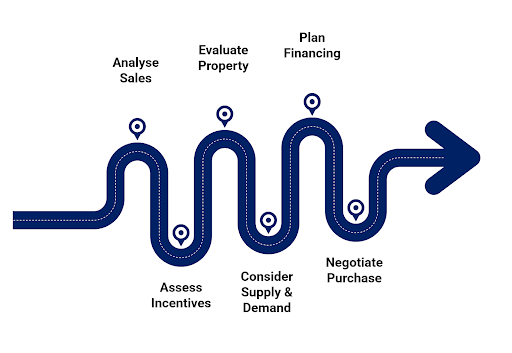

Understanding home pricing in Malaysia for 2026 requires a combination of market awareness, knowledge of valuation criteria, and proactive financial planning. Here are practical insights for navigating home pricing decisions:

- Analyse Recent Comparable Sales

Check the prices of similar properties in your target area within the last 6 to 12 months, factoring in location, size, age, and amenities. Use property portals or request recent transacted prices from agents to set a realistic budget and negotiation target.

- Assess Government Incentives and Costs

Take advantage of ongoing stamp duty exemptions for homes under RM500,000 and purchase relief if buying in the RM500,000 to 750,000 range. Calculate all transaction costs, especially legal fees, stamp duties, and renovation expenses, to determine your total upfront outlay.

- Evaluate Property Condition and Features

Inspect properties for condition, renovation quality, maintenance, and green features (e.g., efficient cooling, solar panels) as sustainable upgrades can positively impact valuation and lower long-term costs.

- Consider Future Supply and Demand

Prioritise homes in areas with upcoming infrastructure, new amenities, and steady population growth (Klang Valley, Iskandar Johor, Penang). Properties near well-connected transport routes typically retain value better.

- Plan for Financing and Loan-to-Value (LTV)

Banks in Malaysia grant loans based on appraised value, not asking price. Check your eligible LTV ratio, have funds ready for the down payment difference, and consider pre-approval to strengthen your bargaining power.

- Negotiate and Time Your Purchase

With a steady supply and moderate price growth forecast in 2026, buyers have room to negotiate, especially for new projects or units remaining in mature condos. Avoid emotional pricing decisions by basing offers on evidence, not on fear of missing out.

Your dream home in Johor is just a click away, and you can explore available listings today.Common Mistakes Buyers Make About Valuation

Many buyers misunderstand how house valuation works in Malaysia, resulting in costly missteps during property transactions. Common errors include:

- Relying solely on automated valuation models without considering local market trends and unique property features can lead to inaccurate property valuation Malaysia outcomes.

- Using inappropriate comparables (comps), such as properties from different areas, conditions, or transaction dates, often produces misleading results for house valuation Malaysia.

- Overlooking physical property condition, recent upgrades, and legal restrictions, these factors can either inflate or depress value.

- Ignoring market cycles and current property trends may lead to expectations that don’t align with bank valuations or approved loan amounts.

- Assuming renovations or personal design choices will fully translate into market value rather than aligning with buyer demand.

- Failing to account for all transaction and ownership costs (stamp duty, renovation, legal fees, maintenance, taxes) when calculating affordability.

Tips to Improve Your Home’s Valuation Score

To enhance your property valuation Malaysia report and fetch a stronger market price, consider these proven tips:

- Maintain, repair, and properly upgrade your home. The condition, presentation, and modern features (energy efficiency, smart tech) are directly factored into house valuation Malaysia.

- Provide complete documentation and access for valuers, including renovation records, permits, and clear external/internal photographs.

- Choose upgrades with high return on investment for your local market (kitchen, bathrooms, curb appeal, security systems), and avoid overcapitalising on niche customisations.

- Highlight unique selling points such as proximity to new transport links, green/ESG certifications, or strong rental demand.

- Ensure quick resolution of legal, title, and zoning issues; clear titles or optimal zoning consistently improve house valuation Malaysia.

- Present your home well for inspections, emphasising cleanliness, decluttered spaces, and natural lighting for the valuer.

Optimising your understanding of valuation processes and strategically improving property features can make a substantial difference to your final house valuation Malaysia report.

What Should Buyers Take Away from Malaysia’s 2026 Property Valuation Landscape?

Understanding property valuation is key to making informed decisions in Malaysia’s 2026 market. By considering market trends, government incentives, property condition, and financing options, buyers and owners can confidently navigate pricing. They can also negotiate effectively and secure long-term value from their investments.

From buying to selling, our property guides cover everything you need to know. Read them now.

Stay updated on Malaysia’s latest property launches and explore fresh investment opportunities today.