Still wondering what is BLR when comparing housing loans? This 2026 guide explains how Malaysia moved from BLR to BR and now SBR, how each system links to the OPR, and why that matters for your monthly instalments. Learn the key differences, how rate changes affect repayments, and what to check before choosing or refinancing a home loan.

Many Malaysians still search for what is BLR, especially when comparing mortgage packages or refinancing older loans. Over the past decade, the Malaysian mortgage system has progressed from the Base Lending Rate (BLR) to the Base Rate (BR) and, since 2022, to the Standardised Base Rate (SBR).

While new loans today use SBR as the reference benchmark, many existing borrowers continue paying older loans tied to BR or BLR. This can make it challenging to understand how rates move, how the system works, and how to identify the most competitive housing loan.

This guide explains what is BLR, how the system evolved to SBR, how OPR vs BLR affects loan costs, and what borrowers should consider before choosing a housing loan.

Understanding BLR, BR and SBR in Malaysia

The journey from BLR to BR to SBR reflects Bank Negara Malaysia’s long-term effort to improve:

- Transparency

- Consumer protection

- Pricing consistency

- Market competitiveness

The three main systems are:

- BLR (Base Lending Rate): Malaysia’s core mortgage benchmark before 2015

- BR (Base Rate): The rate framework used from 2015 to 2022

- SBR (Standardised Base Rate): Used for all new floating-rate consumer loans from 1 August 2022

Although SBR now dominates new financing, consumers still frequently ask what is BLR, particularly when analysing refinancing options or comparing cost differences over time. Understanding the evolution of BLR vs BR vs SBR also explains how interest rates impact real affordability for homebuyers in Malaysia.

What Is BLR?

Before 2015, the Base Lending Rate (BLR) was the main reference rate used by Malaysian banks to price floating-rate mortgages. If banks offered home loans priced as “BLR–x%”, consumers could calculate the interest charged by comparing the discount with the applicable BLR.

For example:

- BLR = 6.60%

- Discount = 2.20%

- Effective rate charged = 4.40%

The appeal of BLR was that it created a standardised reference point across all banks. It was directly influenced by the Overnight Policy Rate (OPR), set by Bank Negara Malaysia. This meant:

- When OPR increased, BLR typically increased

- When OPR decreased, BLR usually decreased

However, BLR eventually became less effective for comparison as banks offered varying discounts, making real loan costs hard to judge. This led BNM to introduce the Base Rate (BR) in 2015 and later the Standardised Base Rate (SBR) in 2022, which is pegged to OPR and shared across all banks, making new loans easier to compare.

What Is BR?

Bank Negara Malaysia introduced the Base Rate (BR) in January 2015 to replace BLR and improve transparency in how banks price housing loans. Under this system, each bank was allowed to set its own BR based on its cost of funds, statutory reserve requirements, and operational expenses.

Unlike BLR, BR separated the reference rate from the bank’s margin. Housing loans were priced using the formula:

BR + Spread = Effective Lending Rate (ELR)

This helped borrowers better understand how much of their interest rate was driven by bank-specific costs and risk. However, because banks could revise their BR even when the Overnight Policy Rate (OPR) remained unchanged, loan comparisons across lenders were still inconsistent. This limitation eventually led to the introduction of SBR.

What Is SBR?

The Standardised Base Rate (SBR) became the mandatory reference rate for all new floating-rate consumer loans from 1 August 2022. Unlike BR, SBR is standardised across all banks and is directly pegged to the Overnight Policy Rate set by Bank Negara Malaysia.

Under SBR, banks are not allowed to adjust the base rate independently. Instead, they compete only on the spread, which reflects their costs, risk assessment, and profit margin. Loan pricing follows a simple structure:

SBR + Spread = Effective Lending Rate (ELR)

This system makes it much easier for borrowers to compare housing loan packages and clearly understand how OPR changes affect monthly instalments. While existing BLR and BR loans remain unchanged unless refinanced, SBR has significantly improved transparency and fairness in Malaysia’s home financing landscape.

What Is OPR?

The Overnight Policy Rate (OPR) is Bank Negara Malaysia’s key benchmark for lending between banks. It influences loan and deposit rates, including housing loans.

As of late 2025, the OPR is 2.75%. When OPR rises, borrowing costs increase and mortgage instalments may go up. When it falls, loans become more affordable. Understanding OPR vs BLR helps borrowers see how policy affects repayments.

The OPR not only impacts housing loans but also other consumer financing, such as personal loans and car loans. Changes in the OPR signal the central bank’s monetary policy stance, tightening to control inflation or easing to stimulate the economy.

By monitoring OPR movements, borrowers can anticipate potential changes in their monthly repayments and plan their budgets more effectively.

How SBR Works in 2026

The SBR model simplifies mortgage pricing and makes the cost structure more transparent.

Under SBR:

Reference Rate (SBR) + Spread = Effective Lending Rate (ELR)

Where:

- SBR depends fully on the Overnight Policy Rate

- Spread reflects the bank’s costs, risks, and expected returns

For example:

- SBR = 3.00%

- Spread = 1.40%

- ELR = 4.40%

If BNM raises the OPR by 0.25%, the SBR will increase by 0.25%, and so will the borrower’s effective rate. This direct relationship strengthens the OPR vs BLR understanding:

- When monetary policy tightens, mortgage repayment costs rise

- When OPR softens, borrowers benefit through lower instalments

This clarity is one of the main reasons SBR has improved transparency in Malaysia’s lending ecosystem.

Get expert property tips with property guides.OPR vs BLR: How They Are Linked

Borrowers often search OPR vs BLR to understand how changes in lending rates affect their wallets. The simplest explanation is this:

- OPR is Malaysia’s key monetary benchmark, set by BNM

- BLR traditionally followed OPR, moving upward when OPR increased, and downward when OPR decreased

This means:

- When OPR went up, BLR increased

- Loan instalments became more expensive

- Borrowers had less repayment flexibility

Even though new loans no longer use BLR, thousands of older mortgages continue reacting under the OPR vs BLR dynamic. This remains highly relevant for households budgeting under different interest rate environments or considering refinancing.

Under today’s rules:

OPR → determines SBR → affects mortgage pricing

This stronger link provides greater assurance that loan pricing reflects national monetary policy rather than internal bank adjustments, which was a key issue under BR.

Understanding what is BLR in this larger context helps borrowers compare old and new products objectively and recognise the long-term cost implications of different loan frameworks.

Key Differences Between BLR, BR and SBR

Understanding the differences between BLR, BR and SBR helps Malaysian homebuyers compare mortgage packages and plan repayments. Each system has a unique structure, transparency level, and connection to the Overnight Policy Rate (OPR), which affects interest costs.

Below is a comparison that simplifies the structural differences for homebuyers evaluating loans:

Comparison Table:

| Feature | BLR | BR | SBR (Current System) |

| Applicable years | Before 2015 | 2015 – July 2022 | August 2022 onwards |

| Used for new loans today? | No | No | Yes |

| Set by | Linked with BNM benchmarks | Each bank individually | Pegged directly to OPR |

| Can banks adjust without OPR change? | Rarely | Yes | No |

| Transparency | Moderate | High | Highest |

| Ease of comparison | Low | Medium | Very easy |

| ELR formula | BLR – discount | BR + spread | SBR + spread |

Knowing what is BLR and how it differs from BR and SBR helps borrowers make smarter loan choices. While BLR and BR could vary across banks, SBR offers a standardised and transparent rate, making it easier to compare loans and plan for future repayments.

Comparison of BLR, BR and SBR Rates in Malaysia in 2026

This table provides a snapshot of typical Base Lending Rate (BLR), Base Rate (BR), and Standardised Base Rate (SBR) figures in 2026 for major Malaysian banks. Note that actual Effective Lending Rates (ELR) will vary depending on the loan spread and borrower profile.

Rate Comparison Table:

| Bank | BLR (Historical/Legacy) | BR (2015–2022/Legacy) | SBR (2026) | Typical Spread | ELR Example |

| Maybank | 6.40% | 2.75% | 2.75% | ~1.15% – 1.35% | 3.90% – 4.10% |

| CIMB | 6.60% | 3.75% | 2.75% | ~1.30% – 1.45% | 4.05% – 4.20% |

| Public Bank | 6.40% | 3.27% | 2.75% | ~1.20% – 1.35% | 3.95% – 4.10% |

Notes:

- BLR is no longer applicable for new loans, but remains relevant for older mortgages.

- BR applied to loans taken between 2015 and 2022.

- SBR is now the benchmark for all new floating-rate home loans.

- Effective Lending Rate (ELR) = Reference Rate + Spread; actual rates may vary based on borrower risk profile and bank policies.

SBR provides a consistent, transparent base for new loans, making it easier for borrowers to compare offers across banks. For older loans, understanding what is BLR and how OPR vs BLR affects your repayments remains essential.

How OPR Changes Affect Monthly Loan Instalments

Housing loans remain highly sensitive to OPR changes, whether based on BLR, BR or SBR. A change in OPR directly influences the effective lending rate, which then recalculates the monthly instalment.

Example Scenario – OPR Increase

- Property loan: RM 450,000

- Tenure: 35 years

- OPR increases by 0.25%

Expected impact:

- Monthly instalment increases by RM 50 – RM 90

If OPR increases 0.75% over 12 months, borrowers may feel substantial pressure, especially those with larger mortgages or lower disposable income.

Why Instalments Increase

A change in OPR affects:

- SBR value

- Effective Lending Rate

- Monthly repayment amounts

Borrowers may choose to maintain their existing instalment amount after an increase, but this usually results in:

- Longer loan tenure

- Higher total interest paid

- Slower principal reduction

Before making such a choice, borrowers should request a full explanation from their bank and understand the long-term cost trade-offs.

Learn your borrowing capacity, use the home loan eligibility calculator.What Borrowers Should Check Before Applying for a Housing Loan

Whether taking a new loan under SBR or considering refinancing, several key checks help borrowers make smarter decisions.

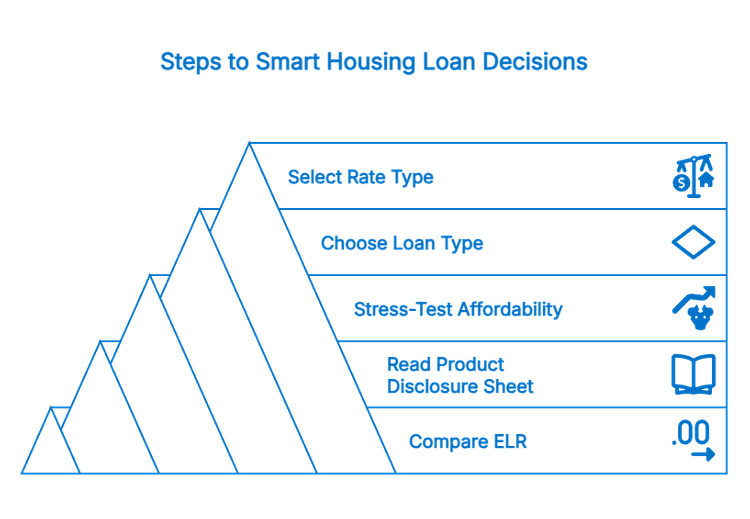

1. Compare the Effective Lending Rate (ELR)

Since all banks share the same SBR, the deciding factor becomes:

- The spread

- Additional fees

- Flexibility of the loan product

Consumers focused on BLR should shift their comparison from base rates to the final interest cost payable after including spreads.

This reflects the patient reality of how repayments behave in practice, over years, not months.

2. Read the Product Disclosure Sheet (PDS)

Required by BNM, the PDS includes:

- The ELR

- Total repayment projections

- Lock-in terms

- Late payment penalties

- Instalment impact under different OPR scenarios

Borrowers should never sign a loan package without reading the PDS in full.

3. Stress-Test Repayment Affordability

Because of the OPR vs BLR style movement still present in SBR, borrowers should ask:

“Can I still afford the loan if rates rise by 0.25%, 0.50%, 1.00% or more?”

This ensures financial resilience during times of rising interest rates.

4. Decide Between Flexi vs Non-Flexi Loans

Flexi home loans allow borrowers to:

- Make additional payments

- Withdraw excess balances

- Save interest on a daily calculation basis

Non-flexi loans are simpler but less adaptable during rate increases.

For many Malaysians, flexi packages offer a safer hedge in volatile OPR vs BLR and SBR rate climates.

5. Choose Between Fixed and Floating Rates

A fixed-rate mortgage offers price certainty. A floating-rate loan means repayments change with OPR. Borrowers should decide based on:

- Their income security

- Risk tolerance

- Market views on interest direction

If OPR is expected to remain elevated for longer, fixed-rate packages may offer breathing room.

Should You Refinance an Old BLR or BR Loan in 2026?

Many Malaysians researching what is BLR today are doing so because they still hold BLR-based mortgages taken before 2015 or BR-based loans between 2015 and 2022.

Refinancing to SBR may provide better value, but not always.

Refinancing may be worth it if:

- Your existing loan spread is high

- Another bank offers a lower ELR

- You have 10+ years left on your loan

- You want flexi redraw or other modern features

Even a modest reduction of 0.30% in the effective rate can translate to:

- Thousands saved annually

- Tens of thousands over long tenures

Refinancing may not be ideal if:

- Your current interest rate is already competitive

- You have less than 4–6 years remaining

- Cost of refinancing outweighs savings

Costs to consider before refinancing:

Refinancing may involve:

- Legal documentation fees

- Property valuation costs

- Potential lock-in penalties

- Stamp duty on new agreements

Before signing, borrowers should always:

- Request a settlement statement from their current bank

- Obtain a PDS from the new bank

- Compare total repayment differences, not just monthly instalments

This ensures financial clarity and protects borrowers from moving solely based on headline rates.

Making a Smart Home Loan Decision

Understanding what is BLR, and how it differs from BR and today’s SBR, allows homebuyers to make smarter and more confident mortgage decisions. Over time, the Malaysian lending framework has shifted towards:

- Greater transparency

- Standardised comparison

- Reduced bank-level manipulation of reference rates

- A cleaner connection between OPR vs BLR, OPR vs BR, and OPR vs SBR

To make the best decision, borrowers should always:

- Focus on the Effective Lending Rate (ELR)

- Understand how OPR movements impact affordability

- Consider long-term costs instead of only monthly instalments

- Select loan structures aligned with financial stability and future plans

With housing prices, interest rates and living costs continuing to shift in 2026, financial literacy plays a major role in long-term property ownership success. For those with BLR-based or BR-based loans, evaluating whether refinancing now leads to meaningful savings could unlock better financial outcomes for the next decade.

Quickly estimate your monthly repayments and see how different loan amounts and rates affect your budget. Use the Home Loan Calculator on iProperty.