Discover how Malaysia’s Overnight Policy Rate (OPR) shapes housing loan interest rates, monthly instalments, and loan approvals in 2026. Learn how OPR movements affect affordability, fixed versus floating loans, and what buyers should consider before securing a mortgage.

Are rising monthly loan repayments squeezing your budget? The Overnight Policy Rate (OPR) plays a key role in determining how much you pay on your housing loan, yet many Malaysians find its impact confusing and overwhelming. This blog will be your go-to guide to understanding how OPR affect housing loan interest rates, loan tenure, and affordability.

By breaking down relatable insights, we will help you navigate your housing finance decisions with confidence and clarity. Say goodbye to uncertainty and make informed choices about your home loan journey.

What Is the Overnight Policy Rate (OPR)?

The Overnight Policy Rate (OPR) is the interest rate set by a country’s central bank at which commercial banks lend or borrow funds from the central bank overnight. In Malaysia, the OPR is set by Bank Negara Malaysia (BNM). It serves as a key monetary policy tool that helps regulate liquidity in the banking system.

It also functions as a base rate that shapes other interest rates in the economy, including Malaysia housing loan interest rates. Essentially, it guides short-term interest rates and helps the central bank regulate money supply, inflation, and overall economic stability. Changes in the OPR can affect borrowing costs for individuals and businesses, with an increase typically leading to higher loan repayment costs.

Why Bank Negara Malaysia Adjusts the OPR?

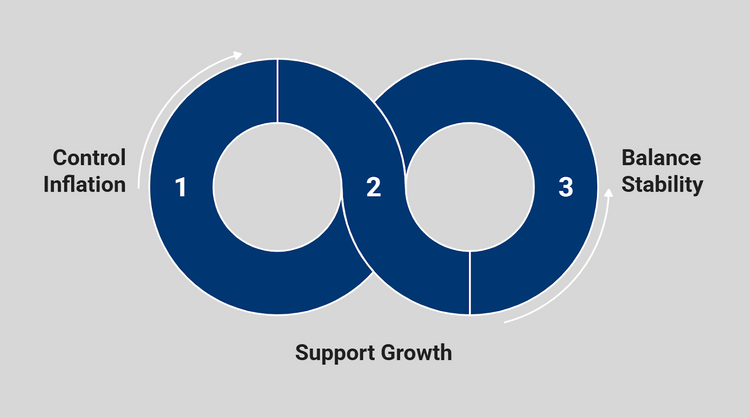

Bank Negara Malaysia adjusts the OPR to keep the economy stable and ensure money flows smoothly through the financial system.

- Keeping Inflation Under Control

When prices rise too quickly, BNM may raise the OPR. A higher rate slows spending and borrowing, helping prevent goods and services from becoming too expensive.

- Supporting Growth During Slow Periods

When the economy is experiencing slower growth, heightened global uncertainties, or weaker consumer spending, BNM may lower the OPR. A lower rate encourages borrowing and boosts economic activity.

- Balancing Overall Economic Stability

Adjusting the OPR helps manage inflation, employment levels, and GDP performance, keeping Malaysia’s economy steady despite changing global conditions.

The OPR adjustments help BNM maintain a stable, healthy, and sustainable economic environment.

Use the mortgage calculator to estimate your monthly payments quickly and accurately.How OPR Influences the Banking System and Borrowing Costs?

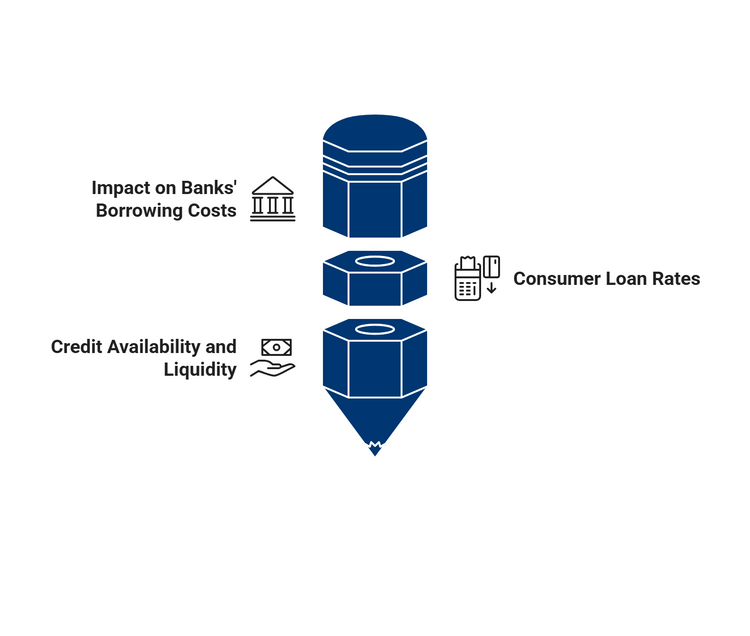

The OPR acts as the base rate that guides how banks price their loans and manage their daily borrowing costs.

- Impact on Banks’ Borrowing Costs

When the OPR increases, banks pay more to borrow funds from each other or from BNM. This naturally leads to higher lending rates. When the OPR drops, banks enjoy lower funding costs and can offer more competitive loan rates.

- Effect on Consumer Loan Rates

Higher OPR means higher interest rates for housing loans, personal loans, and business financing. Monthly instalments rise as a result. Lower OPR brings the opposite outcome; borrowers pay less interest and enjoy cheaper financing.

- Influence on Credit Availability and Liquidity

Changes in the OPR also affect banks’ liquidity and profit margins. A higher rate may tighten credit availability, while a lower rate encourages more lending across the market.

The OPR plays a significant role in shaping borrowing costs and determining how banks price their financial products.

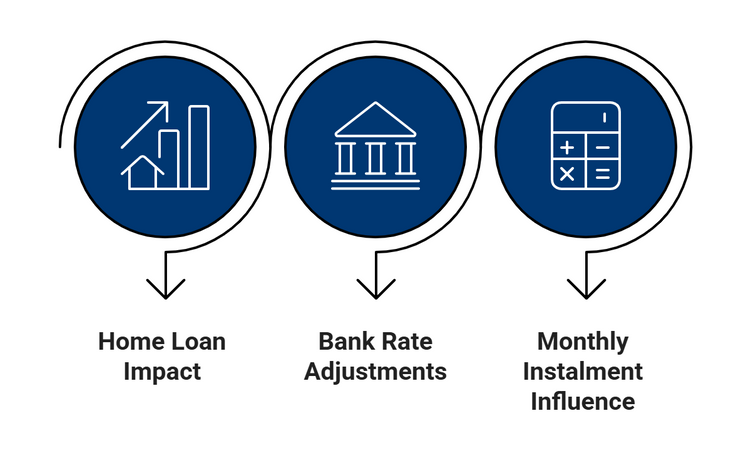

How OPR Affects Malaysia Housing Loan Interest Rates?

The Overnight Policy Rate (OPR) directly influences home loan interest rates in Malaysia by setting the benchmark for banks’ lending costs. When Bank Negara Malaysia raises the OPR, banks tend to raise interest rates on housing loans, increasing monthly repayments for borrowers. Conversely, an OPR reduction encourages banks to lower rates, making mortgages more affordable and stimulating loan demand.

Impact on Fixed vs. Floating Rate Home Loans

Malaysia Housing loan interest rates respond differently to OPR changes depending on whether the borrower chooses a fixed or floating rate package.

- Fixed-rate loans keep the same interest rate throughout the lock-in period. Monthly instalments stay constant even when the OPR moves, giving borrowers predictable repayments.

- Floating-rate loans are linked to the OPR, SBR, or BR. Whenever banks adjust their reference rates after an OPR announcement, borrowers with floating-rate loans see their instalments increase or decrease accordingly.

Fixed rates provide stability, while floating rates directly reflect OPR movements.

How Banks Adjust Their Base Rate (BR) and SBR?

Banks use the OPR as the starting point when setting the reference rates that determine floating loan pricing.

- Banks revise their Base Rate (BR) and Standardised Base Rate (SBR) whenever the OPR changes. These updates influence the interest rates offered for new and existing floating-rate home loans.

- The SBR, introduced after 2022 to improve transparency, follows OPR changes more closely. This makes it easier for borrowers to understand why their loan rates rise or fall.

Any OPR movement triggers corresponding shifts in BR and SBR, which, in turn, shape floating loan rates across the market.

How OPR Changes Influence Monthly Instalments?

A slight shift in the OPR can make a noticeable difference in monthly home loan payments.

- Higher OPR Means Higher Instalments

An increase in the OPR leads to higher interest rates on floating-rate loans. For example, if the OPR rises by 0.25%, someone with a RM500,000 loan over 30 years might see:

- Monthly instalment: +RM71

- Total extra interest paid: more than RM25,000

- Lower OPR Reduces Borrowing Costs

When the OPR decreases, interest rates drop as well. This results in lower monthly payments and a reduced overall loan cost, improving affordability for homebuyers.

Simply put, OPR movements directly influence how much borrowers pay every month and over the entire loan period.

How OPR Affect Housing Loan Approval in 2026?

In 2026, the Overnight Policy Rate (OPR) will continue to shape not just the interest you pay, but also your chances of securing a housing loan approval in Malaysia. As banks adjust to OPR movements, many homebuyers are left wondering if higher or lower rates will make it easier or harder to qualify for the loan amount they need.

Tighter Lending Criteria When OPR Is High

- When OPR is raised, banks often tighten their lending criteria to manage risk in a higher-rate environment.

- Borrowers may face requirements such as higher down payments, stronger credit scores, or lower debt-to-income ratios.

- Higher OPR also means costlier loans, which can affect your loan eligibility if repayments exceed the bank’s acceptable income threshold.

Easier Approvals When OPR Drops

- A lower OPR signals cheaper borrowing costs and encourages greater loan uptake.

- Banks may ease approval criteria, allow higher loan amounts, or accept slightly riskier profiles.

- For Malaysians, this could mean easier access to home financing, especially for first-time buyers or those upgrading to bigger homes.

Ultimately, OPR levels in 2026 will play a central role in determining how easy or difficult it is to get your housing loan approved. Staying informed about rate changes and understanding their implications can help you position yourself more effectively in the bank’s eyes.

Get a quick estimate of your borrowing power using our home loan eligibility calculator.OPR’s Impact on Housing Affordability in 2026

The Overnight Policy Rate (OPR) plays a decisive role in shaping housing affordability for Malaysians in 2026. As the OPR sets the benchmark for home loan interest rates, changes in this rate can either reduce or raise monthly housing costs for both new buyers and existing homeowners.

Lower OPR Supports Affordability

- When the OPR is low, banks offer affordable Malaysia housing loan interest rates, reducing monthly instalment payments for borrowers.

- In 2025, the OPR was decreased to 2.75%, which supported homeownership by lowering debt-service costs and allowing buyers to qualify for higher loan amounts.

- Government measures, such as stamp duty exemptions and loan guarantee schemes, combined with a lower OPR, further improve affordability by decreasing upfront and long-term costs.

High Prices Remain a Challenge

- Despite lower borrowing costs from a reduced OPR, the majority of newly launched homes remain above RM300,000, outside the “affordable” range for many Malaysians.

- Income limitations and high property prices mean that, even with supportive OPR policies, not all households can benefit fully from improved loan terms.

While OPR movements in 2026 will help ease the financial burden on home buyers by making loans more affordable, true housing affordability depends on a combination of interest rates, property prices, and income growth. Buyers will need to consider all these factors when evaluating whether the time is right to purchase a home.

Should You Buy a Home When OPR Is High?

Buying a home when the OPR is high is generally less favourable because you’ll face higher loan interest rates and increased monthly repayments. However, there are situations where purchasing during a high OPR period can still make sense, depending on your financial stability, market timing, and property choices.

Pros and Cons of Buying During High OPR

Here’s a table outlining three pros and three cons of buying a home when the OPR is high in Malaysia:

| Pros | Cons |

| Developers may offer discounts or incentives to attract buyers. | Higher OPR leads to higher home loan interest rates and monthly repayments. |

| Less competition for property, allowing more negotiation power. | Tighter lending requirements could make loan approval harder. |

| Opportunity to secure properties that are less in demand. | Lower loan eligibility and affordability due to increased total costs. |

Considerations for Buyers

- Assess whether you can comfortably afford higher monthly instalments while still maintaining good financial health.

- Consider locking in a fixed-rate home loan if you expect OPR to drop in the future, securing your repayments until rates fall.

- Monitor government policies that may temporarily cushion affordability, such as stamp duty waivers or first-home incentives.

While buying a home when OPR is high can be more expensive, carefully evaluating your long-term financial readiness and property choices and watching for market opportunities can make the decision more strategic. If you’re planning to wait, watch for signals of an upcoming OPR cut, which will lower borrowing costs and improve affordability.

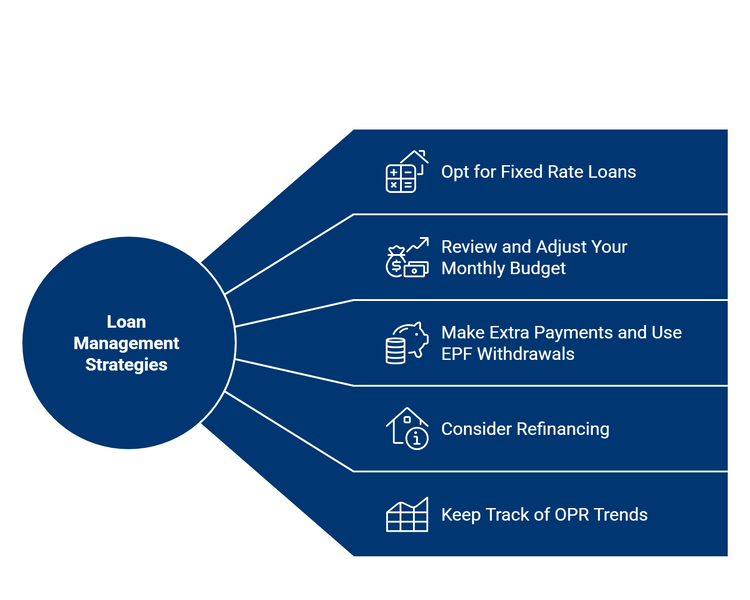

Tips to Manage Housing Loans During OPR Fluctuations

Managing a housing loan can feel challenging when the OPR keeps changing. Here are practical tips to manage housing loans during periods of OPR fluctuations in Malaysia, based on advice from official sources and major banks:

Opt for Fixed Rate Loans

- Fixed-rate loans provide stability, protecting you from sudden increases in monthly repayments when OPR rises.

- Although the initial rate may be higher, it ensures predictable long-term costs and shields you from volatility.

Review and Adjust Your Monthly Budget

- Revisit your financial plan and reduce non-essential expenses to accommodate possible increases in home loan payments.

- Use a home loan affordability calculator to project instalment changes under different OPR scenarios and stay prepared.

Make Extra Payments and Use EPF Withdrawals

- Paying more towards your loan principal when possible will reduce total interest, shorten your loan period, and minimise the impact of rising OPR.

- Consider eligible withdrawals from EPF Account 2 to manage outstanding balances and reduce monthly financial stress.

Consider Refinancing

- If your existing loan rate becomes too high following OPR hikes, shop around for refinancing options with a lower spread or more favourable terms.

- Compare multiple banks, as most use the Standardised Base Rate (SBR), but many offer different spreads that directly affect your repayments.

Keep Track of OPR Trends

- Monitor Bank Negara Malaysia’s OPR announcements and market forecasts to anticipate changes and plan your refinancing, loan applications, or repayment strategies accordingly.

These steps will help borrowers maintain control over their finances and minimise the long-term impact of OPR fluctuations on their housing loans.

Should You Make a Home-Buying Decision Based on OPR Movements?

OPR changes can influence interest rates, repayments, and overall borrowing costs, but they shouldn’t be the only factor guiding your home-buying decision. It’s more practical to consider your long-term financial stability, the property’s value, your savings, and how comfortable you are with potential changes to your repayment terms. If the home fits your budget and long-term plans, you can still proceed even during shifting OPR conditions.

Whether you’re buying or selling, our property guides make every step clearer.

Keep up with Malaysia’s latest property launches and discover opportunities worth considering.