Confused about why your home loan instalments keep changing? This 2026 guide explains Malaysia’s Standardised Base Rate, how it differs from BR and BLR, and how each affects your real borrowing cost. Learn how SBR links to OPR, what spreads mean, and how to compare loans confidently.

Buying a home or refinancing a mortgage often feels overwhelming, especially when interest rates keep changing. Many Malaysians struggle to understand why monthly instalments increase, how banks calculate lending rates, and what the switch from older systems like BR Malaysia means for existing borrowers. The biggest question many ask is simple: How do I know if I am getting the best loan rate today?

The standard base rate in Malaysia plays a major role in determining the real cost of a housing loan in 2026. Recent adjustments to the Overnight Policy Rate have influenced lending rates across major banks, and these changes directly affect home loan affordability. Understanding how SBR affects interest, repayments, and refinancing can help buyers make smarter decisions and avoid costly mistakes.

What Is The Standard Base Rate (SBR)?

The standard base rate in Malaysia is the reference rate used by banks to price new floating-rate home loans and financing products. It is directly linked to the Overnight Policy Rate set by Bank Negara Malaysia. When the OPR changes, the SBR moves by the same amount.

The purpose of SBR is to create a fair, transparent way for borrowers to compare loan rates across different banks. Before SBR was introduced, each bank used its own method to calculate the Base Rate. That system often confused borrowers because rates varied between banks.

Under the SBR framework, all banks start from the same benchmark. The difference in the final interest rate comes from the bank’s spread. The spread depends on borrower profile, risk level, loan package features, and operating costs.

This means the SBR itself is not the final rate borrowers pay. It only forms the base. The actual interest charged is known as the Effective Lending Rate. Understanding this difference helps borrowers compare loans more accurately.

In simple terms:

- SBR reflects national economic policy.

- The spread reflects the bank’s pricing decision.

- The final home loan rate reflects both.

This system makes home loan pricing easier to understand and more consistent for Malaysians planning to buy or refinance property.

Difference Between SBR, BR, And BLR

Understanding the difference between SBR, BR and BLR helps borrowers see how home loan interest is calculated today, and why instalments may change over time. Each rate system was introduced at different stages of Malaysia’s lending history.

Knowing how they evolved makes it easier to understand how banks price home loans in 2026.

Base Lending Rate (BLR)

BLR was the reference rate used before 2015. It was based on borrowing costs between banks and was generally similar across the industry. Home loans were priced using the formula BLR minus or plus a percentage.

Although simple to understand, the BLR structure became less reflective of real funding costs.

Base Rate (BR)

BR replaced BLR in January 2015. Under this system, every bank sets its own reference rate based on internal funding costs and the Statutory Reserve Requirement. This meant loan rates differed from one bank to another. Borrowers found it difficult to compare home loan packages because BR was not standardised.

Many existing loans are still priced under BR, especially those taken between 2015 and July 2022.

Standardised Base Rate (SBR)

The standard base rate Malaysia framework came into effect on 1st August 2022. SBR is now the standard benchmark reference rate used by all banks for new floating-rate home loans. It is directly linked to the Overnight Policy Rate set by Bank Negara Malaysia. When OPR increases or decreases, the SBR moves by the same amount.

The final home loan rate is calculated using SBR plus a spread, reflecting borrower risk and the bank’s pricing strategy.

Comparison Between SBR, BR And BLR:

| Rate Type | When It Was Used | Who Sets It | How Interest Is Calculated | Common Today |

| BLR | Before 2015 | Central bank influenced | BLR ± margin | Only for older legacy loans |

| BR Malaysia | 2015 to 31st July, 2022 (and existing loans today) | Individual banks | BR + spread | Still applies for many existing loans |

| SBR | From 1st August, 2022 | Standardised across all banks, linked to OPR | SBR + spread (Effective Lending Rate) | Used for all new floating-rate home loans |

Why Malaysia Moved To SBR?

The transition from BLR to BR and now to SBR was intended to improve transparency and make loan comparison fairer. Under SBR, borrowers can easily see how a change in OPR affects their repayments. They can also compare loan packages based on spread, instead of being confused by different base rates.

For borrowers, the most important number is the final interest rate, known as the Effective Lending Rate. This is the actual rate paid throughout the loan period. Understanding the ELR helps buyers select the loan that fits their financial situation.

How SBR, BR And ELR Affect Your Home Loan Interest?

Many homebuyers look only at the base rate when applying for a mortgage. However, the base rate alone does not show the full cost of borrowing. What matters most is how the rate is calculated and how it affects monthly instalments.

The Standardised Base Rate is the starting point for new floating home loans. It reflects the Overnight Policy Rate set by Bank Negara Malaysia. When the central bank adjusts interest rates to control inflation or economic growth, the SBR moves accordingly. This means instalments may increase or decrease depending on market conditions.

For older loans priced under BR Malaysia, the calculation works similarly. The difference is that BR varies between banks because it is based on each bank’s internal funding cost. Borrowers under BR may see rate changes that are not directly tied to national policy movements.

Effective Lending Rate: The Real Rate Paid

The Effective Lending Rate is the actual rate borrowers pay throughout the loan period. It reflects the total cost, including the bank’s spread. The spread depends on several factors, including credit score, loan size, property type, and the borrower’s risk profile.

The formula is:

SBR or BR + spread = Effective Lending Rate (ELR)

For example:

- SBR is 2.75 percent.

- The bank spread is 1.30 percent.

- The final interest rate becomes 4.05 percent.

This final rate is what determines the monthly instalment, not the SBR alone. Two banks with the same SBR can still offer different ELRs because the spread is not standardised.

Understanding this difference helps buyers choose the most suitable loan and avoid unnecessary costs over long loan periods. It also shows why comparing only base rates is not enough when selecting a home loan package.

Latest SBR, BR And BLR Lending Rates in Malaysia (2026 Update)

Understanding the latest lending rates is important when planning to buy a home or refinance an existing loan. Rates have shifted in response to recent Overnight Policy Rate decisions by Bank Negara Malaysia. These changes affect affordability and monthly instalments for many borrowers.

Below is an updated snapshot of reference rates published by major banks in Malaysia. This table reflects the most recent publicly available figures as of late 2025.

| Bank | Standardised Base Rate (SBR) | Base Rate (BR) | BLR or BFR | Notes |

| Maybank | 2.75% | 2.75% | 6.40% | Indicative effective rate for RM350,000 loan over 30 years is around 3.90% per year |

| Hong Leong Bank | 2.75% | 3.63% | 6.64% | Latest rate published 14th July, 2025 |

| CIMB Bank | 2.75% | 3.75% | 6.60% | Effective rate varies based on loan package and risk |

| MBSB Bank | 2.75% | 3.65% | 6.50% | Indicative financing rate around 4.20% per year |

| UOB Bank Malaysia | 2.75% | 3.61% | 6.57% | ELR depends on spread and borrower profile |

| Alliance Bank | 2.75% | 3.57% | 6.42% | Updated as of 15th July, 2025 |

The majority of banks are currently aligned at 2.75 percent for SBR, since the Standardised Base Rate is directly linked to the Overnight Policy Rate. Although the base rate may appear similar across banks, the actual rate paid can vary due to differences in spreads. This is why the Effective Lending Rate remains the most important figure to review when choosing a home loan package.

For borrowers with existing loans under BR or BLR, the final repayment amount may still change. These loans continue to follow their original pricing structure unless refinanced or restructured.

How Changes in OPR Affect Monthly Instalments?

Changes in the Overnight Policy Rate directly affect home loan repayments in Malaysia. Since the Standardised Base Rate is linked to the OPR, any adjustment by Bank Negara Malaysia will affect the interest borrowers pay.

When the OPR increases, the SBR rises. This leads to higher monthly instalments. Borrowers under BR Malaysia may experience similar effects, though the movement can vary by bank. On the other hand, when the OPR is reduced, the SBR will fall, and monthly instalments may become lower.

Even a slight change in interest can create a noticeable difference over long loan tenures. For example, an increase of only 0.25 per cent can add thousands of ringgit to the total repayment amount over 30 years.

Example Loan Scenario

Assume:

- Loan amount: RM500,000

- Tenure: 35 years

- Effective lending rate: 4.05 percent

| Situation | Interest Rate | Approx Monthly Instalment |

| Current rate | 4.05% | RM2,277 |

| If SBR increases by 0.25% | 4.30% | RM2,344 |

| If SBR increases by 0.50% | 4.55% | RM2,412 |

A 0.50 percent change results in an increase of about RM135 per month. Over one year, that is more than RM1,600. Over the full loan period, it can exceed RM45,000.

This is why many homebuyers monitor OPR announcements closely. Understanding how interest movements affect instalments can help you decide when to refinance, when to lock in a rate, or when to delay a purchase.

Staying informed helps borrowers plan better, manage risk, and avoid financial surprises.

Should You Choose a Floating or Fixed-Rate Loan in 2026?

Many borrowers face a common question when applying for a home loan. Should you choose a floating rate or a fixed rate? The right choice depends on your financial stability, risk tolerance, and expectations about future interest movements.

Floating-Rate Home Loans

Floating-rate loans move according to the SBR or BR Malaysia, depending on when the loan was taken. When the Overnight Policy Rate changes, the monthly instalment will increase or decrease. Floating loans are popular during stable economic periods or when interest rates are expected to fall.

Advantages of floating rates

- Lower rates when the economy is stable or improving

- Savings when OPR decreases

- Flexible refinancing opportunities

Disadvantages

- Monthly payments can rise unexpectedly

- Harder to plan long-term budgeting

Fixed-Rate Home Loans

Fixed-rate loans offer stability. The interest rate stays the same throughout the agreed period, usually between three and five years. Instalments do not change even if market rates move.

Advantages of fixed rates

- Predictable monthly instalments

- Easier financial planning

- Protection against sudden rate increases

Disadvantages

- Usually, higher starting rates compared to floating loans

- No benefit if OPR drops significantly

Which Option Works Best in 2026?

Interest rates in Malaysia have been adjusting gradually with economic conditions. Borrowers who want stability may prefer fixed rates, especially if they expect rates to rise. Those comfortable with some risk and wanting potential savings may choose floating rates.

The right choice depends on personal priorities. A balanced approach is to compare Effective Lending Rates for both options and check lock-in periods, early settlement fees, and refinancing flexibility.

Calculate your monthly payments in minutes with the Mortgage Loan Calculator.What Homebuyers Should Look For When Comparing Home Loans in 2026

Choosing a home loan is not only about finding the lowest base rate. The real cost of borrowing depends on many factors that affect long-term affordability.

Understanding these points can help you choose the best loan structure for your financial goals.

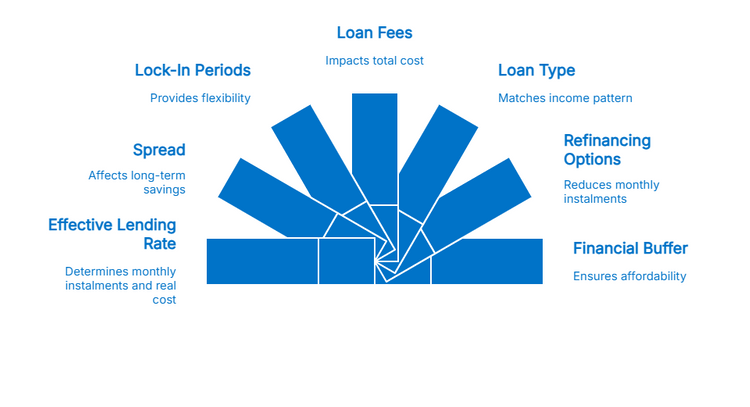

1. Compare the Effective Lending Rate

Do not compare banks based on SBR or BR alone. The Effective Lending Rate shows the real cost of the loan, including the spread. This is the rate that determines your monthly instalment.

2. Check the Spread

Banks apply different spreads based on loan risk, repayment ability, and internal pricing strategies. A lower spread usually leads to lower instalments. A small difference can save thousands of ringgit over time.

3. Review Lock-In Periods

Some loans include lock-in periods. During this period, you must pay a penalty if you refinance or settle early. Shorter lock-in periods give more flexibility.

4. Look at Loan Fees and Conditions

Processing fees, legal fees, valuation fees, and insurance packages, such as MRTA or MLTA, affect the total cost. Always check the product disclosure sheet before signing.

5. Understand Flexi vs Non-Flexi Loans

Flexi loans allow extra payments and lower interest rates. Non-flexi loans are more structured with less flexibility. Choose based on your income pattern.

6. Check Refinancing Options

Refinancing may be helpful if rates fall or if your loan is still priced under BR Malaysia or BLR. Refinancing can reduce monthly instalments, but always consider fees and penalties.

7. Evaluate Your Financial Buffer

Choose a loan where you can still manage instalments even if rates increase slightly. A comfortable buffer reduces financial stress.

A careful comparison helps you choose a loan that fits your lifestyle and long-term goals. When rates move frequently, it pays to review options rather than accepting the first offer.

What Happens to Existing Loans Under BR or BLR?

Many homeowners in Malaysia still have loans priced under the BR Malaysia or the older BLR system. These loans do not automatically change to the Standardised Base Rate. They continue to comply with the terms of the original loan agreement.

If your loan was taken before 1st August 2022, it may still be priced using BR or BLR. The instalment amount can still change, but the movement depends on the bank’s internal cost factors and interest strategy. It may not always follow the Overnight Policy Rate directly.

- Can You Switch to SBR?

The only way to move from BR or BLR to SBR is through refinancing. Refinancing means ending the current loan and starting a new one under the latest structure. This can offer better transparency and potentially lower repayments, depending on the spread and the loan package.

- When Refinancing Might Make Sense

- If the Effective Lending Rate on your current loan is higher than the market average

- If your lock-in period has ended and penalties no longer apply

- When OPR is stable or moving downward

- If you want more flexible features, like redraw or extra repayment

- When You Should Be Careful

- If refinancing fees are higher than the savings you gain

- If you are close to the end of your loan tenure

- If your financial situation has changed and your risk score is lower

- What Borrowers Should Do Now

Contact your bank and request your current Effective Lending Rate. Compare it with current SBR-based offers from other banks. Use this information to evaluate whether refinancing is worth it.

A clear understanding of how BR and BLR operate today can help you plan smarter and avoid unnecessary repayment costs.

Is Now a Good Time to Buy Property in Malaysia?

Many homebuyers are watching interest rates closely before making a decision. Property affordability is influenced strongly by the lending environment. When rates stabilise or decrease, borrowing becomes cheaper and monthly commitments are easier to manage.

In recent months, the Overnight Policy Rate has remained steady. As a result, the standard base rate in Malaysia has also remained unchanged at 2.75 percent across major banks. Stable interest conditions support better planning for both first-time buyers and investors.

Demand in the property market has also shown consistent activity. Many buyers are exploring refinancing opportunities and looking for value in both primary and secondary market homes. Flexible financing packages and competitive spreads have created more choices for borrowers.

However, property decisions should not be based only on interest rates. Financial stability is more important. Always ask yourself:

- Can I comfortably manage repayments if rates rise slightly

- Do I have adequate savings for emergencies

- Am I choosing a property that fits long-term needs

A good time to buy is when you are financially ready, the numbers are clear, and the property meets your lifestyle and investment goals. With transparent pricing under SBR and more tools to compare packages, buyers today have better information than before.

Ready To Make A Confident Home Loan Decision in 2026?

Understanding how the standard base rate Malaysia affects borrowing can help you plan ahead and avoid financial stress. Many buyers worry about rising instalments and feel unsure about comparing loan packages or choosing the right bank. Clear information makes those decisions easier.

When you understand SBR, spreads, and the Effective Lending Rate, you can choose with confidence. You can also decide if refinancing makes sense, especially if your current loan is still under BR Malaysia or BLR.

If you are planning to apply for a home loan soon, review your options early.

Compare effective rates and check how small changes in interest affect monthly repayments. Even a small difference can save a meaningful amount over time.

For more property insights, market updates, and home financing guidance, explore iProperty Guides.

Researching properties? Visit iProperty Malaysia to view new project launches now.