Not all extra payments save the same. This guide explains advance loan payment vs reduce loan principal and why paying straight into principal usually cuts more interest. Learn simple 2026 strategies like flexi loans, EPF use, and refinancing to repay your home loan faster.

For most Malaysians, buying a home means taking on a multi-year housing loan, often 30 to 35 years. While this is considered normal, many homeowners today are choosing to shorten their mortgage tenure by making extra payments. Understanding advance loan payment vs reduce loan principal is essential in knowing which method helps you save the most interest, build equity faster, and enjoy financial freedom earlier.

If you’re looking to repay your home loan faster while staying financially secure, this guide explains refinancing, EPF withdrawals, MRTA vs MLTA, and strategies for early settlement.

Understanding Home Loan Repayment in Malaysia

Home loans in Malaysia generally follow a reducing balance interest structure, meaning interest is calculated daily based on the outstanding principal. If you reduce the principal faster, you reduce the interest charged for the rest of the loan tenure.

This is why strategies like advance loan payment vs reduce loan principal matter; they determine how early payments are applied and how much you eventually save.

Because every bank structures its loan packages differently, extra payments may not always go directly toward reducing the principal. This makes it important to understand your loan terms clearly, so you can make informed decisions that genuinely accelerate repayment and reduce total interest.

Advance Loan Payment vs Reduce Loan Principal: What’s the Difference?

Many Malaysian homeowners try to repay their housing loan faster, but not everyone understands that the method of extra repayment matters. Two common approaches used by banks are advance loan payment and reduce loan principal, and each works very differently.

These two strategies sound similar but are very different in banking terms. Let’s have a look at these.

Advance Loan Payment

Paying in advance means you are settling your upcoming instalments ahead of time. The bank records it as future payments, so your next due dates move forward, but your outstanding principal does not reduce immediately. Because interest is still calculated based on the original principal, the actual savings on interest are minimal.

Example:

If your instalment of RM2,000 is due on 1st April but you pay RM4,000 in March, the RM2,000 extra is treated as paying your May instalment.

Reduce Loan Principal

Reducing the principal means your extra payment goes directly toward lowering the outstanding loan amount. Since Malaysian home loans calculate interest daily based on the remaining principal, this method immediately reduces the interest charged. It is a far more effective way for borrowers exploring how to repay home loan faster.

Which Is Better?

For most Malaysian borrowers who want to maximise savings, choosing to reduce loan principal is usually the more effective option. This method cuts down the outstanding balance immediately, which means less interest is charged over the remaining tenure.

Many banks promote semi-flexi and full-flexi loan packages because these allow you to deposit extra funds directly into the loan account. The moment the principal drops, your daily interest is recalculated on the lower amount, making it one of the smartest approaches for anyone looking into how to repay home loan faster.

- Semi-flexi loan (The bank must process withdrawals manually, sometimes with a small fee)

You can deposit extra money into the account, and it will reduce interest, but if you want to withdraw the extra amount later, you usually need to submit a request and wait for bank processing. - Full-flexi loan (Fully linked to a current account, withdrawals are instant and usually free)

Your home loan is paired with a current account where you can deposit or withdraw money anytime. Every ringgit you keep inside instantly lowers your interest calculation.

Because interest in Malaysia is commonly calculated daily, being able to push extra funds directly into the loan principal gives consistently stronger financial results.

Choosing between the methods depends on your financial goals, flexibility needs, and how your bank handles the repayment structure.

The 2026 Malaysian Home Loan Landscape & Interest Rates

The Malaysian mortgage scene has evolved, with increased competition among banks and borrowers seeking greater flexibility. Gaining clarity on the current interest-rate range and product trends is crucial for deciding between advance loan payment vs reduce loan principal strategies.

As of December 2025:

- SBR/BR

- range: 2.75% – 6.40% (SBR fixed at 2.75%, BLR up to 6.40%)

- Final effective mortgage rates: 3.9% – 4.6%

Most new buyers choose 30- to 35-year tenures. Semi-flexi loans continue to be the most common option.

These features make it more appealing for homeowners to leverage various repayment strategies to cut interest and shorten their loan tenure.

Many Malaysians in 2026 are placing financial priority on:

- Becoming debt-free before retirement

- Reducing interest costs

- Increasing net worth faster

- Leveraging EPF Account 2 withdrawals

These shifting financial habits make understanding advance loan payment vs reduce loan principal more relevant than ever.

Browse a diverse selection of homes for sale in MalaysiaShould You Try to Pay Off Your Mortgage Early?

For many Malaysians, becoming debt-free sooner sounds financially smart, and in many cases, it is. Before making extra repayments, it’s important to look at your personal situation, financial flexibility, and long-term goals.

Benefits of Paying Off Early

Paying off your home loan ahead of schedule offers several advantages that directly impact your finances and long-term goals. Here are the key benefits to consider:

- Lower total interest paid

Extra payments reduce your outstanding balance sooner, so you pay less interest over the life of the loan. - Shorter loan tenure

You may be able to shave years off your mortgage, helping you achieve financial freedom earlier. - Less financial stress later

Removing a monthly repayment can make retirement or future planning much easier and more flexible. - Stronger personal balance sheet

Paying down principal increases your net worth and overall financial position, which may help when applying for future financing.

Overall, early repayment strengthens your financial health while giving you more flexibility and peace of mind.

Potential Risks or Drawbacks

While paying off your home loan early can save interest and reduce debt, it is important to consider the potential downsides. Being aware of these risks helps you plan repayments without compromising financial stability. Here are some key considerations:

- Lower liquidity

Redirecting too much cash to the mortgage can leave you with less emergency savings if something unexpected occurs. - Opportunity cost

Your extra cash might earn better returns elsewhere, such as Amanah Saham Bumiputera (ASB), EPF dividends, or other investments. - Higher-interest debts may need priority first

If you have credit card balances, personal loans, or other debts with higher interest rates, those should generally be settled before focusing on early mortgage repayment. - Possible early settlement fees

Some Malaysian loans still carry lock-in periods or penalty clauses if you settle too early, especially within the first 3–5 years. - Budget pressure

Extra payments must be comfortable and sustainable; stretching your finances too far is risky.

Paying off your loan early can deliver strong financial benefits, but only if it fits your budget and keeps you secure in other areas of life. Take time to evaluate your cash reserves, lifestyle needs, and alternative investment returns to decide if this strategy truly benefits you.

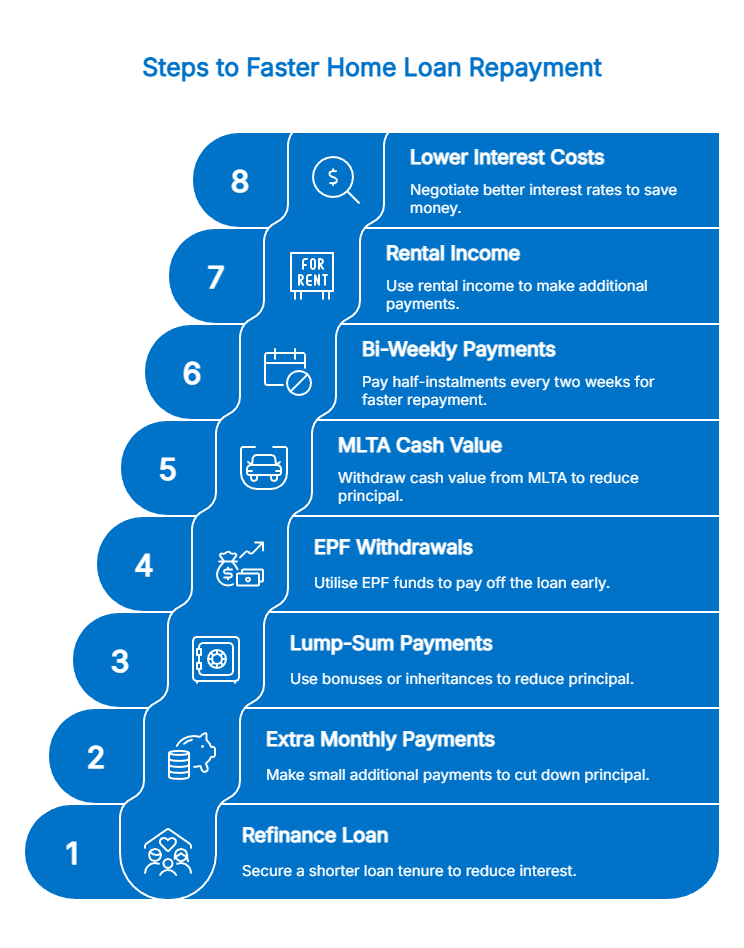

Eight Proven Ways on How to Repay Home Loan Faster in Malaysia

Paying off your mortgage early is possible with a smart repayment strategy that works within Malaysian banking rules. These eight methods can help reduce interest costs and shorten your loan tenure significantly.

Below are the most effective strategies Malaysians use to shorten their mortgage and reduce total interest.

1. Refinancing to a Shorter Tenure

Switching to a shorter loan tenure reduces total interest and forces faster principal repayment. Consider new lock-in periods, fees, and whether your loan is semi-flexi or full-flexi before refinancing.

2. Making Extra Monthly Repayments

Paying more than your required instalment regularly reduces principal faster, lowering daily interest and shortening your loan tenure. Small, consistent top-ups can make a big difference over time.

3. Making Lump-Sum Payments

Using savings, bonuses, or investment returns to pay extra directly toward the principal cuts interest costs and shortens your mortgage term. Always instruct the bank to apply it to the principal.

4. Using EPF Account 2 Withdrawals

Eligible Malaysians can use EPF Account 2 to reduce or settle their home loan. Applying EPF early in the loan term maximises interest savings while keeping within EPF’s withdrawal rules.

5. MLTA vs MRTA: Mortgage Insurance Options

Mortgage Reducing Term Assurance (MRTA) provides reducing coverage with no cash value, mainly for protection. Mortgage Level Term Assurance (MLTA) accumulates cash value that can be withdrawn to reduce principal, helping to repay the loan faster. MLTA therefore offers both protection and a potential avenue for accelerated repayment, unlike MRTA.

6. Bi-Weekly Payment Method

Paying half your monthly instalment every two weeks increases the number of payments each year, reducing principal faster and lowering interest without needing a larger monthly budget.

7. Using Rental Income to Accelerate Repayment

Directing rental profits to extra payments or periodic principal reductions speeds up repayment, builds equity, and improves long-term financial growth. Keep a separate emergency fund for security.

8. Lowering Total Interest Costs

Refinancing to a lower rate, negotiating better spreads, or switching to a full-flexi loan reduces interest costs. Lower interest rates make all extra payments more effective in cutting your loan tenure.

Finishing your mortgage sooner is not just about paying more, but paying smarter with the right repayment approach. Implementing even one or two of these strategies consistently can make a major long-term difference to your financial freedom.

Learn, plan, and invest wisely in Malaysian property with property guidesAdvance Loan Payment vs Reduce Loan Principal: Which One Saves More?

When you want to repay your home loan faster, both methods can help, but they work differently and produce different results.

Let’s compare both approaches side by side.

| Criteria | Advance Loan Payment | Reduce Loan Principal |

| Effect on Loan Tenure | Minimal | Significant |

| Interest Savings | Low | High |

| Immediate Effect | Only changes the due date | Reduces balance instantly |

| Best Used When | You want short-term flexibility | You want long-term savings |

| Long-Term Financial Impac | Slight | Very large |

Most financial advisers in Malaysia recommend reducing principal whenever possible, as it has a far greater impact on lowering interest and shortening loan tenure. Choosing the right approach also depends on how your bank applies extra payments and whether your loan package supports principal reduction efficiently.

Ultimately, the best choice depends on your banking package and personal financial goals, balancing flexibility with long-term savings.

Lock-In Periods, Administrative Charges & Refinancing Costs

Before deciding on advance loan payment vs reduce loan principal, it’s crucial to understand the bank’s rules and fees, as these can impact how effectively you repay your mortgage.

Lock-In Periods

Loans often have a lock-in period, typically 3–5 years, during which early repayment may incur penalties (usually 2%–3% of the outstanding loan). Zero-moving-cost loans generally have longer lock-ins.

Administrative Charges

When making extra payments or repaying your home loan faster, it’s important to account for any additional charges imposed by the bank. These may include:

- Valuation fees

- Legal fees

- Stamp duties

- Documentation or processing costs

Being aware of these expenses ensures your extra payments go toward reducing the principal rather than covering hidden fees, maximising your interest savings.

Refinancing Costs

Refinancing can be a useful strategy to reduce interest or shorten your loan tenure, but it comes with costs that must be considered. These may include:

- Legal processing fees

- Valuation fees

- Administrative charges

Evaluating the total cost against potential savings ensures refinancing genuinely helps you repay your mortgage faster and more efficiently.

Understanding all these conditions ensures your extra payments go toward principal reduction effectively, helping you save interest and shorten your mortgage without unexpected charges.

Paying Off Mortgage vs Investing Your Cash

A major debate in Malaysia is whether homeowners should pay off their home loan early or invest their cash elsewhere to get a better long-term value. The right decision depends on your financial goals, risk tolerance, and the returns you can realistically expect. Let’s have a look at what homeowners can do.

Better to Reduce Loan Principal When:

- Loan rate > investment returns

- You prefer debt-free living

- You want guaranteed savings

Better to Invest When:

- You can earn returns higher than loan interest

- You already have sufficient emergency funds

- You have financial discipline

Some Malaysians follow a hybrid:

- Pay down some principal

- Invest parallel savings

This balances predictable debt reduction with wealth building.

In the end, comparing paying off your mortgage versus investing is not one-size-fits-all. The best choice is the one that strengthens your financial position without disrupting your lifestyle, long-term plans, or peace of mind.

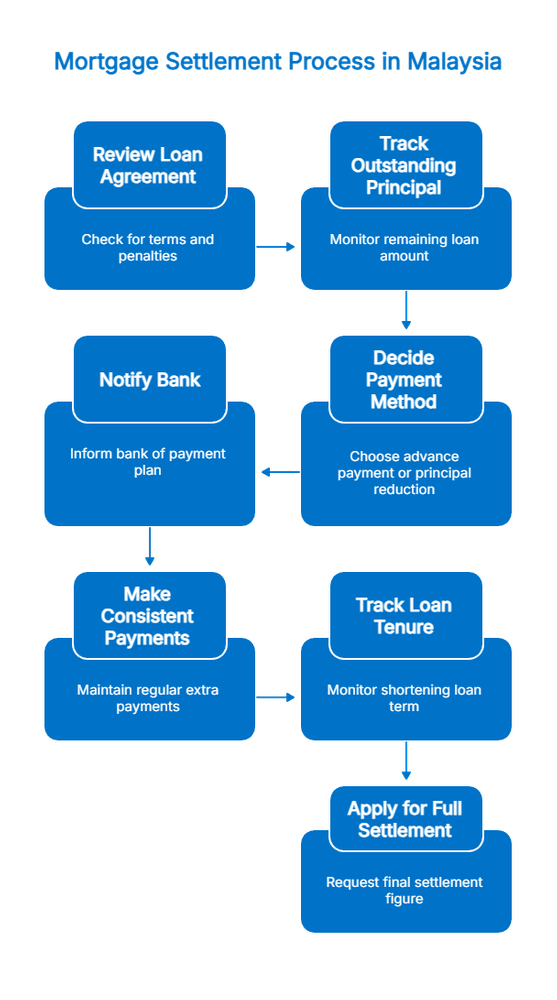

Step-by-Step Process to Settle a Home Loan in Malaysia

Paying off a home loan ahead of schedule is possible for most borrowers, but doing it efficiently requires a proper plan. Here’s a simple step-by-step process that works within the Malaysian banking system:

Step 1: Review Your Loan Agreement

Check for lock-in periods, early settlement penalties, interest type (BLR/BR or fixed), and whether your loan package allows extra repayments without charge.

Step 2: Track Your Current Outstanding Principal

Log in to your bank’s online portal or request a statement to understand how much principal remains and how your monthly instalment is allocated between principal and interest.

Step 3: Decide Between Advance Payment or Direct Principal Reduction

If your bank allows advance loan payment vs reduce loan principal, confirm which method gives you maximum interest savings.

Step 4: Notify the Bank in Writing (If Needed)

Some banks require written instructions if you want extra payments applied directly to the principal.

Step 5: Make Additional Payments Consistently

Whether monthly, quarterly, or yearly, consistency compounds savings when interest is charged daily or monthly.

Step 6: Track New Loan Tenure and Interest Savings

Use the bank’s loan portal or a mortgage calculator to see how your repayment pattern is shortening the loan term.

Step 7: Apply for Full Settlement When Ready

Once you can clear the full balance, request a final settlement figure from the bank (valid for a few days). After payment, the bank will issue a redemption statement and release the property title.

A structured approach helps Malaysian homebuyers shorten their loan tenure smoothly, saving thousands in interest while maintaining financial control.

Look through rental options across MalaysiaWhat Happens After Full Settlement?

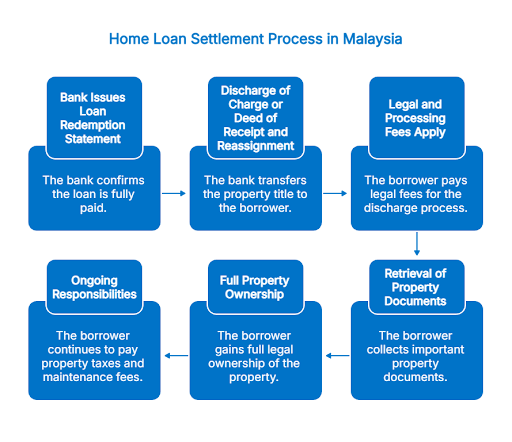

Once you have fully paid off your home loan in Malaysia, whether through advance loan payment vs reduce loan principal strategies, a lump sum payment, refinancing, or regular instalments, the loan officially comes to an end. But there are a few important administrative steps that follow.

Here’s what typically happens after full settlement:

1. The Bank Issues a Loan Redemption Statement

Your bank will formally confirm that the entire outstanding loan amount, including principal and interest, has been cleared. This statement is essential for the next steps with legal documentation.

2. Discharge of Charge or Deed of Receipt and Reassignment

Because the bank is technically the legal charge holder of the property until your loan is settled, the property title must now be transferred fully into your name.

This process depends on the type of title:

Individual or Strata Title (Registered Property):

The bank will prepare a Discharge of Charge, which needs to be lodged with the Land Office to remove the bank’s name from the property title.

Master Title (Unregistered Property):

If the strata or individual title still hasn’t been issued, the bank will execute a Deed of Receipt and Reassignment (DRR), returning the bank’s legal interest in the property back to you or your lawyer.

3. Legal and Processing Fees Apply

Completing the discharge process is not automatic. It requires a lawyer, and the borrower usually bears the cost. Legal fees may vary, but typically include:

- Solicitor’s fees for discharge preparation

- Land office fees

- Registration charges

Being prepared for these costs ensures a smooth settlement and avoids delays in obtaining your property’s clear title.

4. Retrieval of Property Documents

Once the discharge process is complete, you or your appointed lawyer can collect:

- Original copy of the Sale & Purchase Agreement (SPA)

- Original copy of the loan agreement

- Property title (if applicable)

These documents should be safely stored, as they prove full ownership.

5. You Now Fully Own the Property

After discharge, the property is officially and legally free from bank encumbrances. You are now the full legal owner and can:

- Sell the property freely

- Transfer or refinance it

- Use it as collateral if needed

This final step marks the completion of your home loan journey and gives you full control over your property.

6. Future Property Tax or Maintenance Responsibilities Continue

While your loan is over, ongoing costs remain, such as:

- Quit rent

- Assessment tax

- Service charge or maintenance fee (for strata properties)

These are now solely your responsibility without the bank’s involvement.

With your home loan fully settled, the final step is ensuring all legal discharge documents are completed so full ownership officially transfers to you. Once done, the property is entirely yours, giving you full freedom to sell, refinance, or simply enjoy a loan-free home.

The Smartest Way Forward

If your goal is how to repay home loan faster, then understanding the impact of advance loan payment vs reduce loan principal is crucial.

The smartest way forward is to choose a repayment strategy that matches your financial stability, long-term goals, and lifestyle priorities. Some homeowners prefer reducing interest by paying more each month, while others benefit from lowering tenure for faster freedom from debt. Regardless of approach, staying consistent and reviewing your loan performance annually ensures you remain on track.

With careful planning, discipline, and informed decision-making, your mortgage becomes a strategic step towards long-term financial security.

Calculate your estimated monthly instalments and explore scenarios that fit your financial comfort. Use the Mortgage Calculator on iProperty.