A cash home buyer can close faster, avoid interest costs, and gain stronger bargaining power, but ties up large amounts of money in one asset. Taking a home loan in Malaysia in 2026 offers liquidity, access to incentives, and investment flexibility, but comes with long term repayments and interest risk.

Cash home buyers enjoy a strong advantage in Malaysia’s property market. Paying for a property outright without relying on a bank loan can simplify the buying process, save interest payments, and make you more attractive to sellers. However, taking on a housing loan has its own benefits, including financial flexibility and potential government incentives.

Whether you are considering a first property purchase or an investment, understanding the pros and cons of buying a house with cash versus taking on a loan is essential in making an informed decision. In this guide, we explore everything a cash home buyer needs to know in Malaysia in 2026, including costs and benefits, government schemes, and practical tips.

Why Malaysians Are Re-Evaluating How They Finance a Home in 2026?

Homebuyers in Malaysia are becoming more strategic about how they fund their property purchase. With rising living costs, fluctuating interest rates, and the growing preference for financial flexibility, many buyers are rethinking whether to buy as a cash home buyer or take on a housing loan.

This shift has made it essential to understand the long-term impact of both options, not just on affordability, but on lifestyle, liquidity, and future investment plans.

More importantly, buyers now prioritise financial resilience, ensuring their chosen method supports both present needs and future goals.

Factors to Consider Before Buying a House With Cash

Buying a property with cash may appear straightforward, but there are important financial considerations for any cash home buyer in Malaysia. Here are some factors to consider before buying a house with cash:

1. Liquidity and Emergency Funds

Paying for a property outright ties a significant amount of money to one asset. Before making a cash purchase, ensure you have sufficient emergency funds for unexpected repairs, medical emergencies, or other investment opportunities. Being house poor is a risk if too much cash is committed to the property.

2. Property Type and Location

Consider whether the property is a strata development or a landed property. Strata properties come with monthly maintenance fees, while landed homes often require more individual upkeep. Prime locations such as Mont Kiara, Bangsar, or Petaling Jaya might appreciate faster, but upfront costs are higher.

3. Future Financial Goals

Being a cash home buyer should not compromise other financial goals, such as retirement savings, children’s education, or further investments. Evaluate whether tying up funds in a property aligns with your long-term plans.

Considering these factors ensures your cash purchase does not negatively impact your financial stability. Thoughtful planning allows you to enjoy the benefits of homeownership while maintaining flexibility for other priorities.

What are the Costs Involved in Cash Purchases?

Even as a cash home buyer, there are costs beyond the purchase price to consider. Understanding these additional expenses helps you plan your finances more accurately and avoid surprises after the purchase.

1. Stamp Duty

Stamp duty remains a key cost. As of 2025, first-time home buyers may benefit from partial or full exemptions for properties up to RM600,000 under updated government incentives. Properties above RM600,000 may qualify for a 50–75% exemption, depending on price tiers.

2. Legal Fees

Legal assistance is required for preparing the Sale and Purchase Agreement (SPA) and the Memorandum of Transfer (MOT). Legal fees usually range between 0.5% and 1% of the property’s value.

3. Insurance

While not mandatory for cash purchases, home insurance is recommended to cover fire, theft, or natural disasters.

4. Maintenance Fees for Strata Properties

Monthly fees vary based on unit size, facilities, and the number of units in the development. Premium facilities such as swimming pools, gyms, and air-conditioned common areas increase fees. Landed homes require periodic maintenance, which can range from RM200 to RM1,500 monthly depending on property size and condition.

5. Renovations and Miscellaneous Costs

From plumbing issues to repainting, renovations are part of homeownership. Budgeting at least 5–10% of the property value for renovations is a prudent approach.

Being aware of these costs ensures that buying a property with cash does not strain your finances. Careful planning allows cash home buyers to enjoy homeownership without unexpected financial stress.

Start your search for the best homes in Malaysia and browse property listingsAdvantages of Being a Cash Home Buyer

Being a cash home buyer has clear advantages in the Malaysian property market:

1. Strong Negotiation Position:

Sellers often prioritise buyers who can pay cash due to the certainty of transaction completion. Mortgage rejections at the last minute are common for loan applicants, but a cash home buyer avoids this risk entirely.

2. Savings on Interest Payments:

Avoiding monthly loan repayments means significant savings on interest. For example, purchasing an RM600,000 property outright can save hundreds of thousands in interest compared to a 30-year housing loan at a 4.0% interest rate.

3. Faster Closing Process:

Cash purchases can conclude in a matter of weeks, while bank loans may take a month or longer for approval, underwriting, and disbursement. Signing the Sales and Purchase Agreement (SPA) and Memorandum of Transfer (MOT) with cash is straightforward, reducing administrative delays.

4. Simpler Documentation:

Banks require extensive paperwork, including proof of income, credit reports (CCRIS/CTOS), and insurance documentation. Cash home buyers bypass this, making the process less cumbersome.

Drawbacks of Paying Cash for a Property

Despite its advantages, buying a home with cash has some limitations that buyers should consider.

1. Reduced Liquidity

Large sums tied to a property restrict your ability to invest elsewhere or cover unforeseen expenses.

2. Missed Government Incentives

Government schemes, such as the updated 2025 Stamp Duty Exemption and Home Ownership Campaign (HOC) incentives, often apply only when a housing loan is involved. A cash home buyer may miss out on these benefits.

3. Perception Issues

Large cash purchases may attract scrutiny from tax authorities such as LHDN. Ensure funds are legally sourced to avoid complications.

Things to Consider When Taking on a Housing Loan

Opting for a housing loan can be a practical choice for buyers who want to retain cash for other investments or take advantage of government incentives. However, it is important to understand the key factors that influence loan approval and repayment.

1. Debt-to-Service Ratio (DSR)

Banks assess your DSR to determine how much of your income goes towards debt repayment. A DSR below 70% is generally considered healthy, improving your chances of loan approval while ensuring you have sufficient funds for daily expenses and unexpected costs.

2. Credit Reports (CCRIS & CTOS)

Maintaining a strong credit history is crucial. CCRIS tracks your recent bank borrowings, while CTOS provides a broader view of your financial behaviour. A low credit score may affect your loan eligibility or lead to higher interest rates.

3. Mortgage Insurance

Most banks require Mortgage Reducing Term Assurance (MRTA) or Mortgage Level Term Assurance (MLTA), which covers your outstanding loan if you pass away or become permanently disabled. MRTA reduces coverage as you repay the loan, while MLTA provides a fixed coverage amount. This ensures your family does not have to settle the housing loan unexpectedly.

4. Interest Rates

With Bank Negara Malaysia’s OPR at 3.00% in 2025, interest rates directly impact your monthly instalments. Fixed-rate loans offer stability, while floating-rate loans may fluctuate with OPR changes, affecting repayment amounts over time.

While taking on a housing loan allows flexibility and access to government incentives, careful planning is essential. By considering your DSR, credit score, mortgage insurance, and potential interest rate changes, you can make an informed decision and manage your property purchase with confidence.

Compare and choose the right plan for your budget with the home loan calculatorWhat are the Benefits of Financing a Property with a Loan?

Financing a property with a housing loan offers several advantages that go beyond simply spreading out your payments. For many Malaysians, taking on a loan can provide flexibility, access to government incentives, and opportunities for investment growth, making it an attractive alternative to paying for a home in cash.

1. Financial Flexibility

Using a housing loan allows you to spread the cost of a property over time, preserving your cash for other purposes such as investments, renovations, or emergency expenses. This ensures you are not tying up all your savings in a single purchase.

2. Access to Government Incentives

First-time homebuyers who take on a housing loan may qualify for various government incentives. These include stamp duty exemptions, the Malaysia My First Home Scheme (Skim Rumah Pertamaku), and discounts under Home Ownership Campaign (HOC) programmes. Such incentives can significantly reduce the upfront cost of purchasing a property.

3. Potential for Investment Growth

Loans enable investors to leverage their funds to acquire multiple properties. By generating rental income from these investments while keeping some cash in hand, investors can diversify their portfolio and take advantage of other opportunities, such as property renovations or new developments.

4. Building a Credit History

Taking on a housing loan and making consistent repayments helps build a strong credit record with banks and credit reporting agencies like CCRIS and CTOS. A good credit history can improve your eligibility for future loans, lower interest rates, and increase financial trustworthiness for other major purchases.

While paying cash for a property might seem straightforward, financing a property with a loan provides significant advantages. From maintaining financial flexibility and accessing government incentives to fostering investment opportunities and building a strong credit history, a housing loan can be a strategic tool for both homeowners and property investors in Malaysia.

Challenges of Taking a Housing Loan

While housing loans offer several advantages, they also come with potential challenges that every prospective homebuyer should be aware of. Understanding these drawbacks can help you plan your finances better and avoid unexpected difficulties over the long term.

1. Long-Term Commitment

Housing loans in Malaysia typically span 20–30 years. Committing to such a long tenure means that monthly repayments can take up a significant portion of your disposable income. For some, this may limit spending on daily expenses, leisure, or other investments, requiring careful budgeting to maintain financial stability.

2. Rising Interest Costs

Many home loans are linked to Bank Negara Malaysia’s Overnight Policy Rate (OPR). Floating-rate loans are particularly susceptible to fluctuations, meaning even a 0.25% increase in interest rates can substantially raise your monthly repayments over a 30-year period. Borrowers should plan for potential rate hikes to avoid repayment stress.

3. Possibility of Loan Rejection

Banks evaluate applicants based on their Debt-to-Service Ratio (DSR), CCRIS, and CTOS credit reports. A high DSR or poor credit history can result in loan rejection, delaying your homeownership plans. It is essential to prepare and maintain a strong financial profile before applying for a loan.

Although taking on a housing loan allows buyers to spread payments and retain cash for other purposes, it requires careful consideration. The long-term commitment, susceptibility to rising interest rates, and potential for loan rejection are key factors to keep in mind. By understanding these challenges and planning accordingly, homebuyers can manage their loans effectively and make informed property decisions in Malaysia.

Cash Purchase vs Home Loan: A Side-by-Side Comparison for Malaysians

Before choosing whether to purchase as a cash home buyer or through financing, it helps to see how both options compare in terms of cost, flexibility, risks, and long-term benefits.

Comparison Table:

| Category | Buying with Cash | Buying with a Loan |

| Upfront Cost | Full property price + fees | 10% deposit + fees |

| Monthly Payment | None | 20–35 years of instalments |

| Interest | None | High over loan tenure |

| Liquidity | Cash tied up | Cash preserved for other use |

| Process Speed | Fast | Dependent on bank approval |

| Negotiation Power | Strong | Moderate |

| Best For | Buyers with ample cash | Buyers wanting flexibility |

Both approaches have advantages, and the right choice depends on your financial stability, risk tolerance, and long-term goals. Assessing liquidity, affordability, and future plans will guide a confident decision.

Updated Government Schemes and Incentives (2025–2026)

The Malaysian Government continues to refine its housing policies in 2025 and 2026 to support first-time homebuyers and improve overall market accessibility. These updated incentives can significantly reduce upfront costs and broaden financing options for eligible buyers.

1. Stamp Duty Exemption

Under Budget 2026, first-time homebuyers purchasing residential properties priced up to RM500,000 continue to enjoy a full stamp duty exemption on the transfer instrument and loan agreement. The exemption is extended to 31 December 2027.

2. Housing Credit Guarantee Scheme (SJKP)

The guarantee allocation under SJKP has been expanded, enabling more first-time buyers, including freelancers and gig workers, to obtain financing. The increased guarantee amount aims to support up to 80,000 additional homebuyers under Budget 2026.

3. Home Ownership Campaign

Under HOC extensions, developers and the Government continue to provide incentives (discounts, rebates, exemptions) for first-time buyers, especially for properties under the RM500,000 threshold.

4. Affordable & Government-Backed Housing Projects

As part of the 2026 budget allocations, funding is provided towards affordable housing projects under programmes such as People’s Housing Programme (PPR) and Rumah Mesra Rakyat, aimed at B40 and M40 income groups, though these target lower-cost housing rather than private market properties.

These updated measures offer meaningful financial relief to eligible Malaysians, helping reduce the total cost of homeownership and easing entry into the property market. Understanding these incentives allows buyers to plan more effectively and take advantage of available support when purchasing a home.

See what’s new on the market right now and explore the latest property launchesiProperty Tips for Cash Home Buyers and Loan Applicants

Buying a home is one of the biggest financial decisions most Malaysians will make. Whether you plan to purchase with cash or take on a housing loan, understanding the key considerations can help you avoid costly mistakes and make a choice that suits both your lifestyle and long-term financial goals.

1. Evaluate Your Financial Situation

Before committing to a property, assess your cash reserves and monthly cash flow. Ensure you have sufficient funds for emergencies, unexpected expenses, and ongoing commitments such as maintenance or education costs. Even cash home buyers should avoid tying up all their savings in a single property purchase.

2. Understand the Market

Research current property values in key areas such as Kuala Lumpur, Petaling Jaya, and Johor Bahru. Understanding market trends, average prices, and upcoming developments will help you make an informed decision and avoid overpaying for a property.

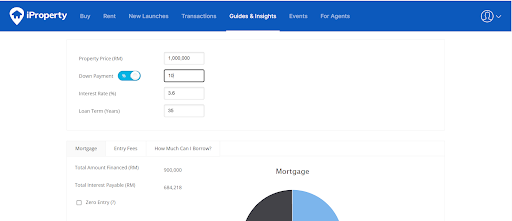

3. Compare Loan Offers

For those considering a housing loan, take time to compare different loan packages from multiple banks. Use online tools such as the iProperty Home Loan Calculator to estimate monthly repayments, interest costs, and total loan expenditure over the tenure.

This allows you to visualise different scenarios and select the most cost-effective loan structure for your situation. Even cash home buyers can use the calculator to understand the potential savings in interest if they were to take a loan instead of paying fully in cash.

4. Plan for Hidden Costs

Buying a property involves more than just the purchase price. Budget for additional costs such as legal fees, stamp duty, maintenance charges, renovation costs, and home insurance. Factoring in these expenses early ensures you are financially prepared for the full cost of homeownership.

5. Consider Investment Potential

Cash home buyers may enjoy the simplicity of outright ownership, but they could miss opportunities to leverage cash for other investments. Loan applicants, on the other hand, can retain some cash for alternative investments such as shares, gold, or even rental properties, potentially increasing long-term financial growth.

Careful planning is key whether you are a cash home buyer or taking on a housing loan. By evaluating your finances, understanding the property market, comparing loan offers, budgeting for hidden costs, and considering investment opportunities, you can make a well-informed decision that aligns with your financial goals and long-term property plans.

Making the Right Choice

Whether you are a cash home buyer or planning to take on a housing loan, the decision depends on personal finances, long-term goals, and market conditions. Paying cash reduces debt and interest payments, simplifies the transaction, and makes you an attractive buyer. Conversely, financing a property allows liquidity, access to government incentives, and the ability to invest in multiple properties.

Ultimately, understanding your financial position, government schemes, and market trends will ensure a confident, informed decision.

For Malaysians ready to make a move, planning carefully and leveraging available tools is key.Planning to buy a home soon? Explore comprehensive guides on property buying in Malaysia.