Explore Malaysia’s mortgage options in 2026, from basic term loans to semi-flexi and full-flexi packages. Understand how repayment flexibility, withdrawal rules, fees, and OPR movements affect long-term interest costs, so you can choose a home loan that truly fits your financial goals.

Buying a home is one of the biggest financial decisions most Malaysians will make, and choosing the wrong home loan could cost tens of thousands of Ringgit over time. Understanding the semi flexi loan meaning, and how it differs from basic term and full flexi mortgages is crucial for first-time buyers and experienced homeowners alike.

In Malaysia, most home loans fall into three main categories: basic term loans, semi-flexi loans, and full flexi loans. While their names may sound similar, each differs in how interest is calculated, how repayments are processed, and how deposits or withdrawals are handled.

With rising property prices, stricter repayment expectations, and more cautious spending habits in 2026, selecting the right home loan is more important than ever.

Understanding Malaysian Mortgage Choices

Most housing loans in Malaysia are variable-rate packages based on the bank’s Base Rate. This means repayment amounts may change over time depending on Bank Negara Malaysia’s Overnight Policy Rate (OPR).

While advertised interest rates are important, they should not be the only factor when choosing a mortgage. Understanding the semi flexi loan meaning, withdrawal rules, fees, and repayment flexibility often has a greater long-term financial impact.

In 2026, Malaysian buyers are increasingly leaning toward:

- Loans that allow extra repayments

- Mortgages that reduce interest as savings increase

- Options to withdraw funds for emergencies

- Lower long-term interest cost

This trend explains why semi-flexi and full-flexi products are more popular today than a decade ago.

What Is a Basic Term Loan?

A basic term loan is the simplest and oldest type of mortgage in Malaysia. It is a traditional repayment structure where the borrower pays a fixed instalment every month throughout the tenure.

How It Works

- The monthly instalment is fixed

- No automatic interest reduction, even if you pay extra

- Extra payments will usually be treated as advance instalments

- Withdrawals are normally not allowed

Pros

- Predictable monthly repayment

- Good for tight budgets

- Often offers lower interest rates

- Stable repayment planning

Cons

- No payment flexibility

- Extra payments do not reduce the loan principal

- Early settlement penalty usually applies (around 3% if settled early within the lock-in period)

Basic term loans are increasingly rare in Malaysia in 2026, but still exist among traditional banking products, especially for buyers who want repayment certainty without changing instalments.

Semi Flexi Loan Meaning: How Does It Work?

A semi-flexi loan is a mortgage that allows borrowers to pay more than the scheduled instalment amount and reduce interest charges based on the reduced principal. This is different from a basic term loan, where extra payments do not reduce interest.

Key Features of Semi Flexi Loan Meaning

- You can make additional payments at any time

- Interest is recalculated based on the lower outstanding balance

- You may be able to withdraw your extra funds, subject to conditions

- Some banks require formal withdrawal requests

- Some banks charge processing fees when withdrawing

Because the semi flexi loan meaning includes the ability to reduce your mortgage interest as savings increase, this structure has become extremely popular among homebuyers who expect increasing income over time.

Pros

- Savings reduce interest immediately

- May result in thousands of Ringgit saved over the loan life

- Commonly offered by Malaysian banks

- Allows withdrawal (subject to fees or procedures)

Cons

- Withdrawal rules vary by bank

- Some impose administrative fees

- May have slightly higher interest rates than basic term loans

- Approval is sometimes required for withdrawals

In Malaysia, most buyers choose semi-flexi mortgages as they strike the right balance between repayment freedom and cost savings.

Full Flexi Home Loan Explained

Full flexi loans operate similarly to semi-flexi but with greater freedom.

How They Work

- Extra funds automatically offset principal

- Interest recalculated daily or monthly

- The borrower can withdraw excess funds anytime

- A linked current account is provided

- Cheque book and/or debit card access are usually included

Fees

Full-flexi mortgages in Malaysia normally charge monthly maintenance fees, usually between RM5 and RM10.

Pros

- Complete repayment flexibility

- No approval is generally needed for withdrawals

- No penalties for depositing or withdrawing extra funds

- Maximum long-term interest savings

Cons

- Higher interest rates than other loan types (in many cases)

- Monthly maintenance fees

- Fewer banks offer this type of loan as of 2026

Full Flexi loans offer maximum repayment flexibility and easy access to funds, making them ideal for borrowers who value liquidity and control. However, higher interest rates and maintenance fees should be weighed before choosing this option.

Flexi Loan Vs Semi Flexi Loan: Key Differences

Understanding flexi loan vs semi flexi loan is critical for Malaysians when comparing their options. Although both are more flexible than basic term loans, they are not identical.

Here is the clearest comparison:

- In a semi-flexi loan, withdrawals may:

- Require approval

- Incur a service fee

- Take processing time

- In a full-flexi loan:

- Withdrawals are usually free

- No formal approval needed

- Funds are accessible instantly via a linked current account

Both allow additional deposits to reduce interest, but full-flexi gives more autonomy and faster access to funds.

This is why the question of flexi loan vs semi flexi loan often comes down to how frequently a borrower expects to withdraw extra funds.

Make informed property decisions with expert property guidesComparison Table: Basic Term, Semi Flexi & Full Flexi Loan

Understanding the differences between Basic Term, Semi-Flexi, and Full-Flexi loans is essential for choosing the right mortgage. This table highlights key features, flexibility, and fees to help you pick the loan that best fits your financial strategy.

| Loan Type | Flexibility | Withdrawal Rules | Extra Payments Reduce Interest | Fees | Best Suited For |

| Basic Term Loan | Very low | Usually disallowed | No | None | Borrowers who want fixed instalments |

| Semi-Flexi Loan | Medium | Allowed but may require notice or fees | Yes | Possible admin charges | Buyers wanting savings but not needing instant withdrawals |

| Full-Flexi Loan | High | Free and instant via linked account | Yes | RM5–RM10 per month | Buyers who want maximum control and liquidity |

By comparing features side by side, borrowers can make an informed choice that balances repayment flexibility, interest savings, and access to funds according to their lifestyle and financial goals.

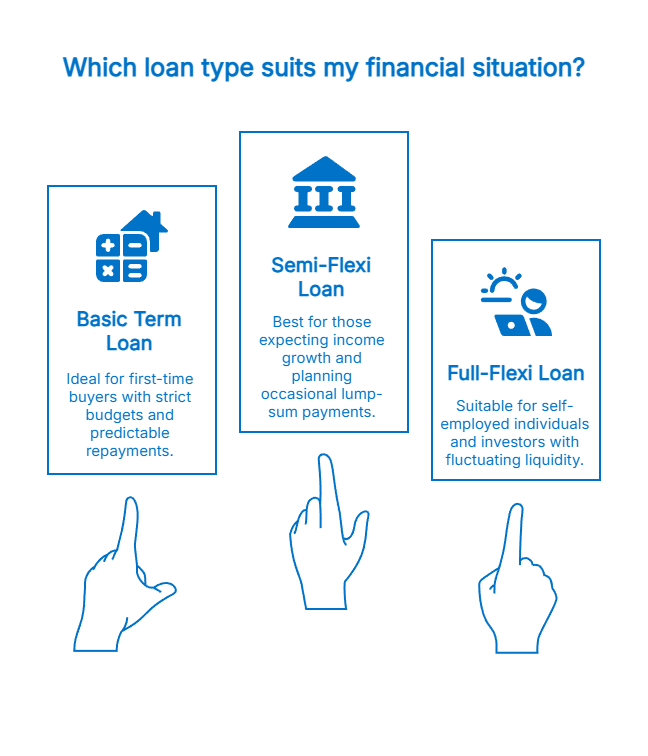

Which Loan Suits Which Type of Buyer?

Choosing between flexi loan vs semi flexi loan, and basic term mortgages depends on personal financial behaviour.

Basic Term Loan Best For:

- First-time buyers with strict monthly budgets

- Borrowers who want predictable repayments

- Buyers unlikely to make extra deposits

Semi-Flexi Loan Best For:

- Workers expecting a higher income in future

- Buyers planning irregular or occasional lump-sum payments

- Those who may withdraw funds occasionally

- Borrowers wanting lower total interest without extra account fees

Full-Flexi Loan Best For:

- Self-employed individuals

- Business owners or freelancers

- Investors with fluctuating liquidity

- Borrowers planning to deposit and withdraw frequently

The main difference between the three loans lies in flexibility and access. Basic term loans offer fixed repayments with no extra access, semi flexi loans provide occasional structured access with interest savings, and full flexi loans allow instant access and maximum control over funds.

Islamic Home Loans: How Are They Different?

Islamic home financing continues its strong momentum into 2026, projected to comprise around 50% of total bank financing in Malaysia amid rising demand for Sharia-compliant options.

Unlike conventional loans, Islamic financing:

- Does not charge interest

- Uses Sharia-compliant buy-and-lease (or partnership) structures

- May be based on concepts like Murabahah or Musyarakah Mutanaqisah

- Fixes profit margins upfront

- Can be structured to operate similarly to semi-flexi or full-flexi in repayment behaviour

Islamic loans are available to all customers, Muslim and non-Muslim alike.

How OPR Affects Home Loans in 2025?

Bank Negara Malaysia (BNM) adjusts the Overnight Policy Rate to align with inflation, liquidity and economic conditions.

As of December 2025, OPR remains stable at 2.75% (cut from 3% in July 2025, unchanged through November MPC meetings).

How Rising OPR Affects Borrowers

- Instalments increase for variable-rate loans

- Interest cost rises over the tenure

How Lower OPR Helps Borrowers

- Instalments fall

- Tenure may shorten (if the monthly instalment remains unchanged)

This impact is particularly noticeable in flexi loan vs semi flexi loan products, since:

- Semi- and full-flexi borrowers can offset higher interest by depositing more funds

- Basic term borrowers cannot reduce interest permanently, even if they pay ahead

Changes in the OPR directly affect your loan instalments and total interest cost. Semi and full flexi loans offer the advantage of offsetting higher rates through extra deposits, while Basic Term loans remain fixed regardless of rate changes.

Compare and choose your next rental home in MalaysiaCommon Mistakes Malaysians Make With Semi Flexi Loans

Even though many borrowers understand the semi flexi loan meaning, they often fail to maximise its advantages. Avoiding these common mistakes ensures you get the full benefit of interest savings and flexibility.

1. Relying Only on Minimum Monthly Instalments

Many homeowners treat semi flexi loans like basic term loans, paying only the scheduled instalment every month. This defeats the purpose of the semi flexi structure, which is designed to help you reduce interest through extra deposits. Without additional payments, interest savings remain minimal.

2. Withdrawing Too Frequently

Some borrowers treat the semi flexi loan as a convenient savings account. Frequent withdrawals reduce principal gains and may incur fees or require bank approval. This behaviour cancels out long-term interest savings and prevents the loan from performing as intended.

3. Not Understanding Bank Fees or Conditions

Semi flexi withdrawals are not always free. Many banks charge RM10–RM50 per transaction, require forms, or process withdrawals in one to two days. Borrowers who are unaware of these conditions end up frustrated or paying unnecessary fees.

4. Failing to Adjust Repayments When OPR Changes

When interest rates rise due to OPR adjustments, borrowers should increase repayments to maintain cost savings. Ignoring these changes may increase total interest significantly. This is one of the biggest differences when analysing flexi loan vs semi flexi loan, because full flexi borrowers respond faster with instant withdrawals and deposits.

5. Depositing All Savings Without Keeping an Emergency Buffer

Some borrowers become overly aggressive and deposit every spare Ringgit into their loan, leaving no emergency fund. If an urgent expense arises, they are forced to withdraw and pay fees, negating their earlier savings.

6. Choosing a Semi Flexi Loan Without Assessing Their Financial Behaviour

Semi flexi loans suit borrowers who can commit to overpayments. Those without this habit might be better off with a basic term loan or, if they need instant access, a full flexi loan.

Avoiding these common mistakes ensures you fully benefit from the flexibility and interest savings that a Semi Flexi loan offers. Thoughtful planning, disciplined repayments, and careful withdrawals make the loan an effective tool for reducing your mortgage cost.

Things to Consider When Choosing the Right Loan

Selecting the right home loan depends on your income, spending habits, and how you plan to manage repayments. When comparing mortgage choices, consider:

1. Expected Future Income

If your salary is stable with little expected change, a basic term loan may be the most suitable option. However, if your income is likely to grow over time, a semi flexi loan becomes more valuable. Extra repayments can reduce interest and potentially shorten the overall loan tenure, saving you thousands over the years.

2. Need for Emergency Access

If you anticipate needing access to funds for emergencies, a full flexi loan is usually the better choice. It allows instant withdrawals without approvals, providing flexibility and peace of mind when unexpected expenses arise.

3. Loan Optimisation Habits

Borrowers who actively deposit spare cash into their mortgage accounts can maximise interest savings. Semi and full flexi loans are ideal for those who plan to make regular overpayments to reduce the loan principal faster.

4. Administrative Costs

Consider the fees associated with each loan type. Full flexi loans often charge ongoing monthly maintenance fees, while Semi Flexi loans may impose withdrawal fees. Understanding these costs helps you choose a loan that aligns with your financial habits.

By assessing your future income, access needs, repayment habits, and fees, you can choose the loan that best fits your lifestyle and financial goals. The right choice ensures both flexibility and long-term savings.

Strategies to Maximise Your Semi Flexi Loan

Understanding the semi flexi loan meaning is only the first step. To fully benefit from this flexible mortgage structure, borrowers must adopt smart repayment strategies that reduce interest, shorten the loan tenure, and preserve financial freedom. Here are the most effective ways Malaysian homeowners can maximise a semi flexi loan.

1. Make Consistent Extra Repayments

The heart of a semi flexi loan lies in its ability to reduce principal instantly whenever extra deposits are made. Even committing RM200–RM500 monthly can significantly lower the long-term interest you pay. Consistency is more impactful than occasional large deposits because it reduces the principal earlier and more frequently.

2. Deposit Lump-Sum Payments Strategically

When you receive bonuses, commissions, or tax refunds, allocating part of them to your loan dramatically accelerates principal reduction. A single RM10,000 lump sum can shorten your tenure by several months or more, depending on your outstanding balance.

3. Increase Deposits During High OPR Periods

When interest rates rise, semi flexi borrowers can fight higher costs by depositing more. This helps maintain manageable monthly interest and offsets rising instalments, an advantage not available to basic term loan holders.

4. Limit Withdrawals to True Emergencies

Semi Flexi loans offer flexibility, but frequent withdrawals weaken their biggest advantage. Keeping extra deposits untouched ensures the interest reduction remains effective. Use the withdrawal feature only for emergencies or unavoidable expenses.

5. Use Budgeting Systems to Stay Disciplined

Set a fixed percentage of your income aside as an extra repayment. Automate transfers so deposits consistently reduce your principal without requiring monthly reminders.

6. Monitor Your Loan Regularly

Online tools and bank apps help track your principal, interest savings, and repayment progress. Awareness encourages better decisions and motivates you to stay committed to your repayment strategy.

By consistently making extra repayments, strategically depositing lump sums, and monitoring your account, you can significantly reduce interest and shorten your loan tenure. Semi Flexi loans reward disciplined borrowers with both flexibility and long-term savings.

Which Loan Should You Choose?

Choosing the right loan helps you balance monthly payments, interest savings, and access to extra funds. In Malaysia 2026, buyers typically choose:

- Basic term loans for fixed budgeting

- Semi flexi loans for balanced freedom and interest savings

- Full flexi loans for maximum liquidity

If your goal is:

| Goal | Recommended |

| Reduce interest without constant account control | Semi-Flexi |

| Make frequent withdrawals and deposits | Full-Flexi |

| Fixed monthly payment | Basic Term |

When comparing flexi loan vs semi flexi loan, the difference ultimately depends on how often you need unrestricted access to your prepayments.

If you seldom withdraw, semi-flexi is usually sufficient.

If you withdraw frequently, full-flexi makes more sense despite the small monthly fee.Discover a variety of landed and high-rise homes to suit your lifestyle and budget. Explore properties for sale on iProperty.