| Periods | Gain | Periods | Gain |

| 1990 to 2000 | 46 % | 2000 to 2010 | 109% |

| 1991 to 2001 | 26% | 2001 to 2011 | 112% |

| 1992 to 2002 | 7% | 2002 to 2012 | 145% |

| 1993 to 2003 | -26% | 2003 to 2013 | 120% |

| 1994 to 2004 | 4% | 2004 to 2014 | 94% |

| 1995 to 2005 | -13% | 2005 to 2015 | 82% |

| 1996 to 2006 | -2% | 2006 to 2016 | 41% |

| 1997 to 2007 | 144% | 2007 to 2017 | 34% |

| 1998 to 2008 | 50% | 2008 to 2018 | 90% |

| 1999 to 2009 | 37% | 2009 to 2019 | 22% |

| AVERAGE | 56% | ||

If you have extra money, is it better to pay extra on your mortgage or invest in the stock market? This is a common question with many theoretical answers. This article attempts to answer that question for Malaysian home buyers based on historical evidence.

✉️Subscribe to us on Telegram for the latest property insights and updates.

Five years ago, my friend’s son, like many young Malaysians, bought a house with an 80% house loan repayable over 20 years. Following a promotion and some extra income, he contemplated whether to use the money to shorten his loan period (by paying extra every month, thereby reducing the total amount paid to the bank) or to invest it in the stock market

The sources of his dilemma were these two iProperty.com articles with different suggestions:

- Properties vs stocks: Which is a better investment in Malaysia?. This article says your ROIs are similar in properties and stock markets over a 20-year period.

- Should you pay off your home loan early? Here’s how & when you should do it

This got me thinking. We have the data: we know how house prices have changed and how the KLCI has performed over 20-year periods. We also know the history of housing loan interest rates. Based on this historical evidence, and from a cash flow gain perspective, which would be the better choice?

The short answer is you are better off investing any extra monies in the stock market than paying off your housing loans. The gain from a reduced total amount paid to the bank is more than offset by the lower gain from investing, as shown below:

I have also analysed four house types – terrace house, semi-d, detached and high-rise in Kuala Lumpur, Selangor, Johor and Penang, and my conclusion is independent of the house type and location, meaning the purchase price and potential capital gain from the house are not factors to consider.

We should not be surprised by the results. Historically, long-term returns of stock markets far exceed long-term housing loan interest rates. I can reconcile these findings with the two iProperty.com articles as follows:

- The article on housing gain vs stock market returns does not consider cash flow situations, only capital gains from changes in house prices. With cash flow considered, stock markets provide better returns.

- The article on early loan settlement is actually in line with my findings. It shows that if the returns from other investments are higher than the loan interest rates, you should not pay off the loan early. This is consistent with my findings that the long-term returns from the KLCI are higher than the long-term housing loan interest rate.

When returns from stock markets exceed the housing loan interest rate, you are better off not making that extra housing loan payment. It does not matter if it’s a large lump sum payment or several annual payments, or when you make the extra payment.

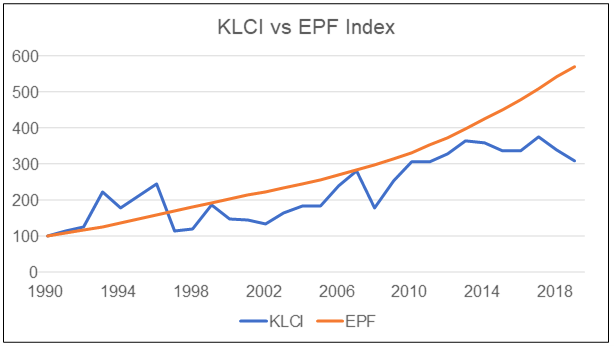

If you have zero knowledge of stock markets, the EPF has a Top-up Savings Contribution scheme where you can make additional voluntary contributions to your loved ones’ accounts. If you had invested 100 each in both the EPF and the KLCI in 1990, what you achieved over the next 20 years is illustrated in the chart below:

Also, if you had an opportunity to withdraw a lump sum to pay off some of your housing loans, you are better off leaving your money in the EPF to let the savings compound.

These conclusions are surprising and counter-intuitive. There are limitations to the conclusion and of course, they assume the future will be the same as the past. This is where I leave you with a quote from Howard Marks, founder of Oakfield Capital which, in 2019, was acquired by Brookfield Asset Management, the biggest public real estate investment company in the world. He said, “History doesn’t repeat itself, but it does rhyme.”

Let’s jump into the detailed explanation, which is broken down into 7 sections, to showcase how we arrive to the conclusion of why you shouldn’t pay off your mortgage early:

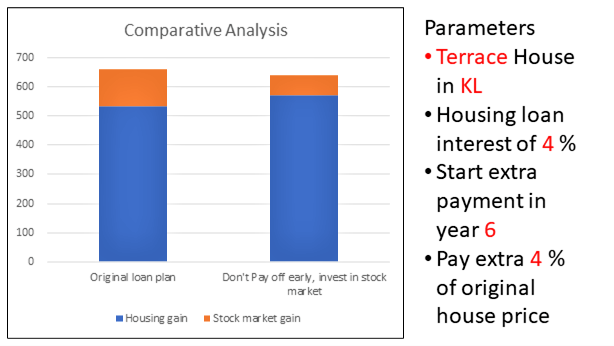

1. Comparative analysis: Invest or settle your housing loan?

Let’s look at what you can do with that extra money:

- Scenario A: Invest, or

- Scenario B: Pay off your mortgage.

And then we will compare the cash flow gain between them.

A cash flow gain is defined as the difference between monies received (or receivable) and those paid. If the gain from B is higher than A, it is better to pay the bank. Apart from the four property types in the four regions mentioned above, I also analyse the impact of both Scenarios with the following variables:

- When you first start having the extra money. I cover three periods – year 6, year 8 and year 10 after the purchase of the house in year 1.

- The house loan interest rate: look at four interest rates situations – 3%, 4%, 5% and 6%. These should cover the range of Malaysian house loan interest rates.

- The extra money: I assume that a buyer would have bought the appropriate type of house based on his ability to repay the loan. As such, I look at the extra money as a percentage of the house value. For my analysis, I look at three percentages – 4%, 5%, and 6%.

Cash flow gain under Scenario A (Invest)

The cash flow gain under Scenario A comes from two sources:

- The house: This is the difference between the house price at the end of the loan period (i.e., year 20) and the monies paid to the bank as well as the down payment for the house. Refer to section 2.

- Investing in the stock market: This covers both the capital gain from the increase in the stock market index and the dividends received. Refer to section 3.

The gain from investing in the stock market will of course vary with when you first have the extra money and how much extra money you have.

Cash flow gain under Scenario B (Pay off your mortgage)

The cash flow gain under Scenario B comes from two sources as well:

- The house as per Section 4. This is likely to be more than under Scenario A as you have paid less to the bank.

- Investing in the stock market. You may argue that if you are using the extra money to repay the bank, where would you have the money to invest in the stock market?

The reality is that if you make the extra payment to the bank, you will shorten the loan period. So instead of repaying the bank for 20 years, you may only have to repay the bank for 15 years. After this, you will have the money that would have gone to the bank repayments for other investments. I have assumed that these are invested in the stock market.

The stock market investment here will be for a shorter period.

2. Gain from the house purchase

I compute that gain from buying and owning the house for 20 years based on the following assumptions:

- A 20-year housing loan

- Purchase financed 20% by down payment from savings and 80% from the bank loan

- I ignore sales commissions, legal fees and stamp duties in my analysis

The gain from buying and owning the house for 20 years is represented by Equation 1. The gain in cash-flow terms is the difference between the price of the house at the end of the original loan period of 20 years and what you incurred (the sum of what you paid to the bank plus the down payment).

Equation 1: Gain = [ House price in year 20 ] – [ Total payment to the bank ] – [ 20 % down payment ], where:

- The house price in year 20 = House purchase price X average gain over 20 years.

- The total amount paid to the bank depends on the interest rate and the loan amount, which in turn is dependent on the purchase price of the house.

- The 20% down payment is dependent on the purchase price

Obviously, house prices and gains will vary between house types and locations. Since I am looking at a 20-year period, I base my analysis on data from 1990 to 2019.

The following sections describe:

- How I derive the house purchase price

- The average gain in house prices over 20 years

Purchased house price

The purchased price is based on Q1 2005 Malaysian National Property Information Centre (NAPIC) data. This is because 2005 is in the middle of 1990 and 2019. The chart below shows the prices of the four property types in the four regions covered in the analysis.

Average gain in house prices over 20 years

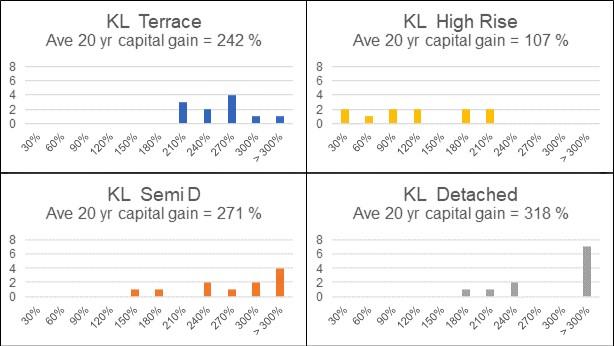

Data for average gain in various categories of properties are available in my previous article, When is the best time to buy a house in Malaysia?, where I analyse price gains over several rolling 20-year periods. I reproduce below the charts for Kuala Lumpur as an example.

The average gains for the different house types are based on their respective rolling 20-year period gains. For example, the average gains over 20 years for Kuala Lumpur are as follows:

- Terrace – 242%

- High-rise – 107%

- Semi-D – 271%

- Detached – 318%

3. Stock market gain

There are two sources of gain from investing in the stock market

- Capital gain – refer KLCI Capital Gain

- Dividends – refer to Dividends

I used the changes in the Kuala Lumpur Composite Index (KLCI) to represent the gain from investing in the stock market.

KLCI capital gain

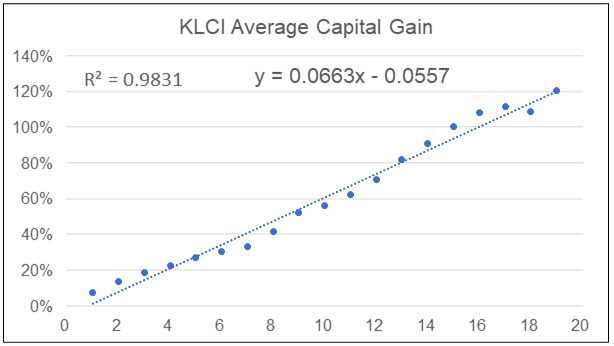

To be consistent with the property gains, I look at the stock market capital gain from a rolling period basis. I derive the rolling capital gains as shown in the following example:

- If you invest for one year, the average gain for a one-year period is the average annual gain from 1990 to 2019.

- If you invest for two years, the average gain for a two-year period is the average gain for all the two years rolling gain from 1990 to 2019.

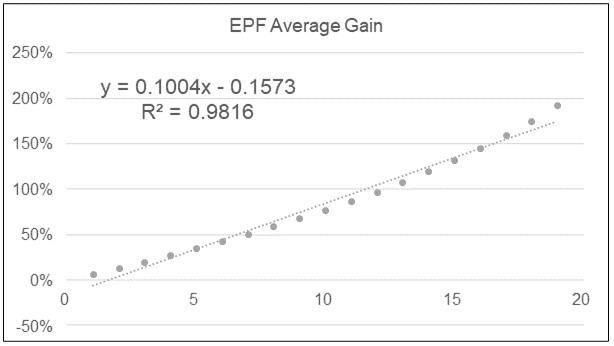

- If you invest for 10 years, the average gain for a 10-year period is the average gain for all the 10 years rolling gain from 1990 to 2019. To elaborate there are twenty 10-year periods as shown below with an average gain of 56%:

I compute the average rolling gains for the various holding period and then plot them as shown in the following chart:

Notice that gain increases with the investment period. To simplify the analysis, I find the best fit line to represent the gain for various periods – this becomes Equation 2.

Equation 2: KLCI gain = [ 0.0663 X Investment period ] – 0.0557

For example, if you invest for 5 years, then the capital gain

= [0.00663 X 5] – 0.0557

= 0.2758 or 27.58 %

CHECK OUT: How to invest in REITs in Malaysia and why is it an alternative to property investment?

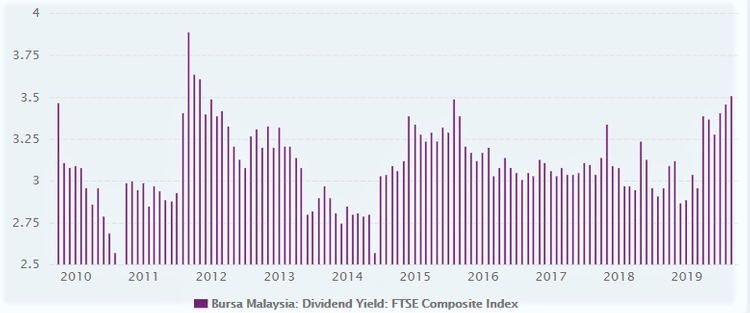

Dividends

Over the past decade, the dividends paid by the companies making up the KLCI generally ranged from 2.75% to 3.25% as can be seen from the chart below. For the purpose of this analysis, I have assumed that it is 2.75 % per annum.

I have assumed that the dividends received would be reinvested back to the stock market. Thus, the total gain from dividends is not just the annual dividends received but also the capital gains from the reinvested dividends.

The above analyses show that some numerical skills are helpful when you invest in the stock market. This is especially if you invest based on fundamentals.

What happens if you don’t have the skills to invest based on fundamentals but want to do so? One way is to rely on third-party advisers to undertake the fundamental analysis for you. There are several financial advisers who provide such analyses and do it well, such as The Motley Fool*. If you subscribe to their services, you can tap into their business analysis and valuation.

Financial Model

The financial model is developed using Equations 1 and 2.

Total Gain = Capital gain from the house + Gain from the stock market

= Equation 1 + Equation 2

For each of the Scenarios, I look at the results based on the following parameters:

- 4 types of houses – terrace house, semi-d, detached, high-rise

- 4 regions – Kuala Lumpur, Selangor, Johor, Penang

- 4 housing loan interest rates – 3%, 4%, 5%, 6%

- 3 points in time to start the additional loan payment – after 6 years, 8 years and 10 years

- 3 additional loan payments as a % of the housing loan – 4%, 5%, 6%

The value of the house depends on type and location. Together with the bank interest rate, this will determine the annual amount to be paid to the bank over the 20-year loan period. The returns from the stock market as well as gain from the property will be affected by:

- when you start to pay the additional amount

- the quantum of the additional payment.

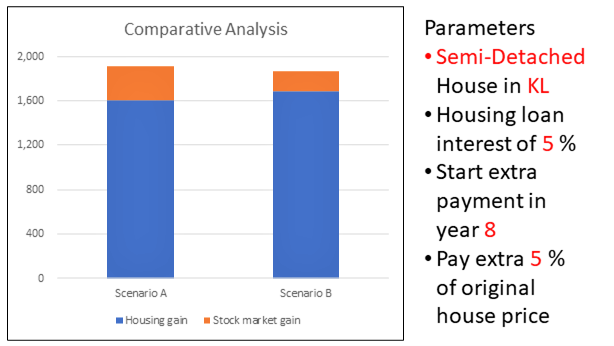

I then compute the gains under both Scenarios for the various parameters. The chart below summarises a sample result.

Reviewing the results

In all possible combinations of parameters, Scenario A (Invest) outperforms Scenario B (pay down your mortgage). Meaning, if you had extra money, it is better to invest in the stock market. It was a counter-intuitive result.

To verify that it was not a computation or modelling error, I decided to check the model mathematically. For those mathematically inclined you can refer to Appendix 1. The mathematical model shows that the results are independent of the following parameters:

- Type of house

- Location

- Housing capital gain achieved

Whether Scenario B would be a better option is very dependent on how large the housing loan interest rate is compared to the stock market gain. In situations where the annualised stock market returns are greater than housing loan interest rates, Scenario B is never better than Scenario A.

It was only when I set the housing loan interest rate at 9% that I could get some situations for Scenario B to be the better option based on the Financial Model. These were for:

- Starting the extra payment in year 6 with the extra amount based on 4% or 5% of the housing loan.

- Starting the extra payment in year 8 with the extra amount based on 4%.

Even with the housing loan interest rate at 8.5%, there are no situations where the Financial Model has Scenario B being better than Scenario A. The analyses show that once the returns from the stock market exceed the housing loan interest rate, it does not matter how the additional payment is made. Reducing the loan repayment period is not a better measure regardless of:

- when you start to pay

- how much more you pay

READ: How to set up utilities in your new home after receiving Vacant Possession (VP)?

5. Malaysian Employee Provident Fund (EPF)

For those with zero knowledge in stock markets, an alternative way to invest is by making an additional contribution to the EPF. The EPF has a Top-Up Savings facility where the Topper may voluntarily make additional contributions to his family members’ (Toppee) EPF accounts.

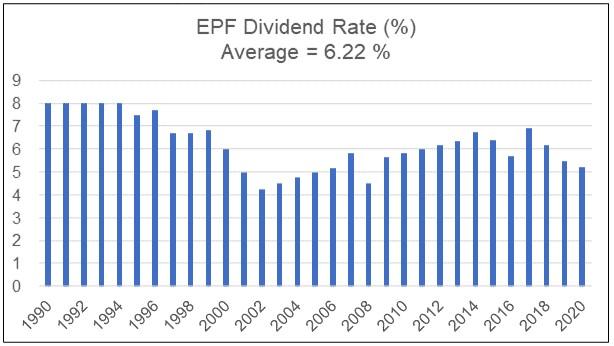

The chart below shows the annual dividend paid by the EPF from 1990 to 2020.

Assuming that a contributor started with 100 in 1990, I derive the amount the person would have using the annual returns in the chart above. I then compare this with those achieved by investing 100 in the KLCI starting in 1990. Over a 20-year period, the EPF contributor achieves more than the KLCI investor as shown in the KLCI vs EPF chart in the introduction. This is because there is no drawdown for the EPF.

Given that returns from the EPF on a long-term basis exceeds those of the KLCI, there is no logic to further analyse. Nevertheless, I run a few simulations with different amounts and different payment timing and find this to be correct. In order to have a consistent approach, I compute the various rolling years’ returns for the EPF as per the KLCI analysis. I then plot the returns and obtain the best fit line as shown below to use in the simulations.

I also examine the EPF scenario from a reverse perspective. If you could withdraw a certain lump sum from the EPF to repay part of your housing loan, should you do so?

Logically you should not do so as you are reducing the potential gain from the EPF when you withdraw. At the same time, the potential savings from the housing loan is smaller as the housing loan interest is lower.

6. Limitations

The above conclusions are of course dependent on the differences between the returns from the stock market (or EPF) and the housing loan interest rates. It is valid as long as the housing loan interest rates are lower than the investment returns. It is also dependent on what you do once you have fully paid off the housing loan. In my analysis, the assumption is you would invest the additional money (from no longer having to pay the housing loan) in the stock market.

Technically it is invested in the same asset class as what you would have invested in if you chose not to make the additional loan repayment. If the investment vehicles are different in both Scenario A and B, not only would the returns be different, but the risk profile would be different. Finally, I would point out that my analysis is mainly a numerical analysis. In reality, you have to consider other qualitative issues such as liquidity, penalties for early redemption, or mortgage insurance benefits.

7. Why you shouldn’t pay off your mortgage early

After examining historical evidence (the actual performance of the KLCI, the actual change in property prices and the history of housing loan interest rates) and the several scenarios of using your extra money (lump-sum vs annual payments, when you start paying, the amount you pay), the conclusion is that in Malaysia, it is better not to pay more of your housing loan. Instead, invest in the stock market or increase your contribution to the EPF. And this conclusion is true no matter what type of house you own or its location, or how you use your extra money to repay your loan.

This article was originally published as Better to invest or pay off mortgage? – the evidence. by i4value.asia and is written by Dato Eu Hong Chew.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.