Malaysia housing loan interest rates in 2026 are driven by the OPR and banks’ Base Rates, directly affecting your monthly repayments. Knowing how loan types and rate changes work helps you compare banks and choose a more affordable mortgage.

Malaysia housing loan interest rates in 2026 continue to play a significant role in how homebuyers plan their finances, compare banks, and choose the right loan package. With changes in the Overnight Policy Rate (OPR), shifting Base Rates (BR), and evolving bank policies, borrowers need a clear understanding of what shapes loan affordability.

This article breaks down the key factors influencing interest rates, the types of loans available, which banks offer competitive packages, and what you can do to qualify for better rates. Whether you’re applying for your first mortgage or exploring refinancing, this guide helps you make steady and informed choices for the year ahead.

What Drives Changes in Malaysia’s Housing Loan Interest Rate in 2026?

Housing loan interest rates in Malaysia in 2026 are influenced primarily by macroeconomic policies and banking practices aimed at maintaining economic stability and supporting affordable homeownership.

Bank Negara Malaysia’s (BNM) Overnight Policy Rate (OPR)

Bank Negara Malaysia’s Overnight Policy Rate (OPR) is a key determinant in mortgage loan interest rate malaysia, as it influences the cost of borrowing across the banking system. The OPR was lowered to 2.75% in July 2025 and is expected to remain stable through early to mid-2026, depending on economic growth and inflation trends.

This rate affects bank lending costs, and any change can directly affect housing loan interest rates, with potential easing if economic growth slows or inflation remains manageable.

Base Rate (BR) and Base Lending Rate (BLR) Changes

Banks base their housing loan interest rates on reference rates such as the Base Rate (BR) and Base Lending Rate (BLR), which track BNM’s OPR but also incorporate bank-specific factors, such as operational costs and credit risk.

Fluctuations in BR and BLR reflect changes in OPR and market conditions, leading to corresponding adjustments in mortgage loan pricing. These adjustments ensure banks cover their costs while responding to monetary policy signals, impacting how affordable housing loans are for borrowers.

The OPR set by Bank Negara Malaysia drives the overall lending environment, while the BR and BLR adopted by banks translate that policy into actual loan interest rates for homebuyers in 2026. Monitoring these rates helps borrowers understand potential shifts in their monthly repayments and overall housing affordability.

Check your monthly instalments instantly with our mortgage payment calculator.What are the Types of Housing Loans in Malaysia?

Malaysia offers different housing loan structures that cater to various borrower needs and financial management styles. Understanding the types of loans available helps homebuyers choose a plan suited to their situation and repayment preferences.

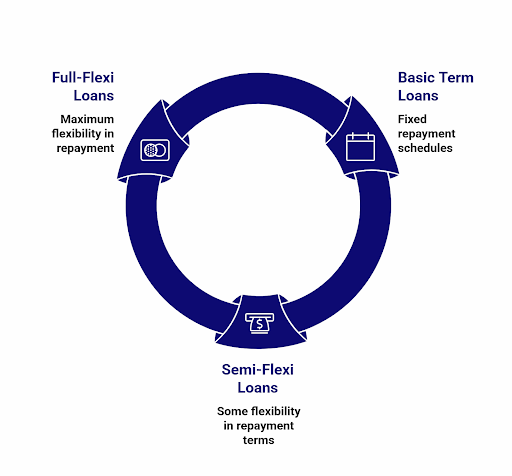

Basic Term Loans

- Fixed repayment schedule with a set monthly payment over the loan tenure.

- Interest rate calculated on the outstanding loan amount until the loan is fully paid.

- Less flexibility in repayment beyond the set schedule; prepayment may be subject to fees.

Basic term loans are straightforward and suitable for borrowers who want predictable monthly instalments and stable budgeting. They allow precise long-term planning but offer limited flexibility for early repayment or fluctuating cash flows.

Semi-Flexi Loans

- Combines a fixed monthly repayment with the ability to deposit extra funds to reduce principal.

- Excess repayments lower the interest charged, shortening the loan tenure or reducing monthly payments.

- Provides some flexibility without forfeiting the discipline of monthly instalments.

Semi-flexi loans are a middle ground for borrowers who want to save on interest by paying more when possible, while also maintaining regular payment discipline. It helps reduce interest costs and loan duration with moderate flexibility.

Full-Flexi Loans

- Highly flexible structure allowing repayment of any amount at any time without penalties.

- Borrowers can withdraw excess funds deposited as needed, offering liquidity.

- Interest savings depend on frequent principal reductions.

Full-flexi loans suit borrowers with variable incomes or those wanting maximum control over repayments and withdrawals. They offer the most excellent flexibility but require discipline to manage repayments and avoid increasing the outstanding loan balance.

Each loan type in Malaysia balances flexibility, interest savings, and repayment security differently. Choosing the most appropriate type depends on personal financial behaviour and future income expectations.

How Housing Loan Interest Rate Changes Affect Your Monthly Instalments?

Housing Loan Interest rate fluctuations in 2026 will directly affect monthly housing loan repayments, impacting affordability and homeowners’ budgets.

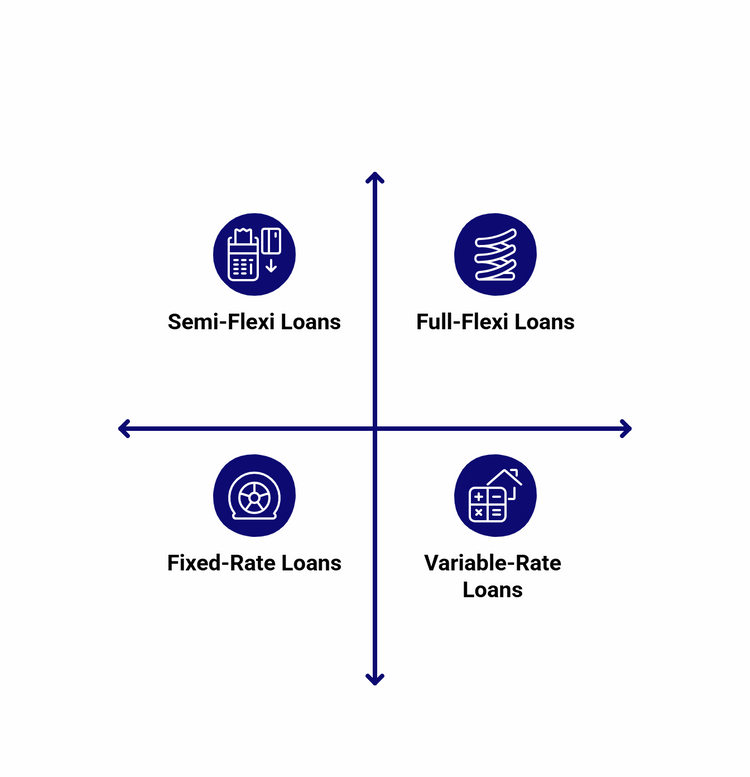

Effect on Fixed-Rate Loans

- Monthly instalments remain constant throughout the loan tenure.

- Interest rate changes typically do not affect ongoing fixed-rate loans but do apply when renewing fixed-rate packages or applying for new loans.

- Offers payment stability and easier budgeting, even amid fluctuations in market interest rates.

Fixed-rate loans protect borrowers from rising interest rates, providing peace of mind with predictable monthly costs. However, borrowers may miss out on benefits if rates fall during the fixed term.

Effect on Variable or Floating Rate Loans

- Monthly instalments fluctuate with changes in the reference rate, such as the Base Rate (BR) or Base Lending Rate (BLR).

- Any upward revision in bank interest rates will increase monthly payments, impacting household cash flow.

- Conversely, rate reductions can lower repayments, easing financial pressure.

Borrowers with variable-rate loans must plan for possible payment increases due to higher interest rates, though they can benefit from rate cuts. Maintaining an emergency fund can help manage these fluctuations.

Effect on Semi-Flexi and Full-Flexi Loans

- Interest savings depend more on principal repayment patterns than on changes in the market interest rate.

- Early or extra repayments reduce outstanding principal and accumulated interest, lowering monthly instalments or loan tenure.

- Withdrawal of excess funds in full-flexi loans can affect principal balance and interest calculations.

For flexible loans, borrower behaviour significantly influences monthly costs alongside interest rates. Financial discipline in making extra payments can mitigate the impact of rate hikes.

Interest rate changes in 2026 require careful monitoring for all loan types to manage monthly instalments effectively. Borrowers should review loan terms and prepare for potential repayment variations to safeguard their financial stability.

Get a quick estimate of what you can afford with our mortgage calculator in just seconds.Banks Offering the Best Mortgage Loan Interest Rate Malaysia

Choosing the right bank can make a big difference in your monthly instalments and overall loan cost. Below is a quick look at some banks offering competitive mortgage loan interest rate malaysia, along with key features to help you compare their packages more easily.

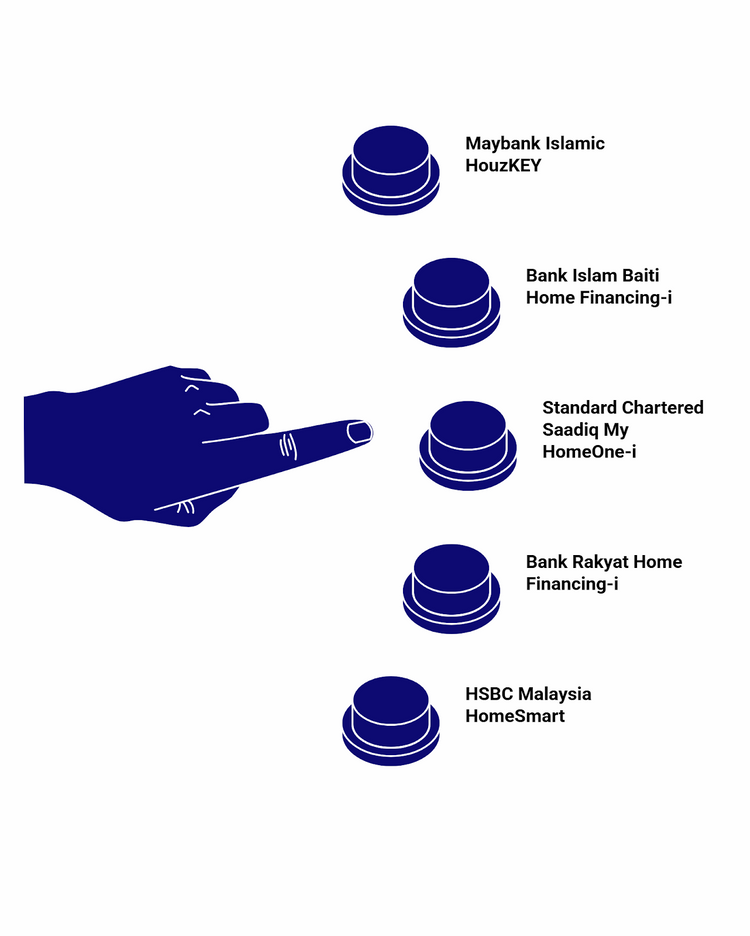

- Maybank Islamic HouzKEY

- Interest rates from as low as 2.88% per annum

- Offers Islamic financing with up to 100% financing on selected properties

- Loan tenure up to 35 years, with a 1-year lock-in period

- Suitable for Malaysian citizens within key regions like Klang Valley, Johor, and Penang

- Bank Islam Baiti Home Financing-i

- Profit rates starting around 3.55% per annum

- Term Islamic financing with a tenure of up to 35 years

- No lock-in period, suitable for flexible loan management

- Standard Chartered Saadiq My HomeOne-i

- Financing rates from approximately 3.9% per annum

- Flexi Islamic financing allows flexible payments and withdrawals

- Loan tenure up to 35 years, no lock-in period

- Bank Rakyat Home Financing-i

- Profit rates as low as SBR + 1.45% (SBR at 2.75%, effective rate around 4.2% and up)

- Financing up to 95%, tenure up to 35 years, no lock-in

- Includes Mortgage Reducing Term Takaful (MRTT) coverage

- HSBC Malaysia HomeSmart

- Effective lending rate around 4.5% per annum (SBR + 1.75%)

- Flexible home loan with zero moving cost promotion

- Minimum financing set depending on region, with up to 30-35 years tenure

These banks provide some of the most competitive mortgage rates in Malaysia for 2026, with variations in loan types, financing limits, and flexibility. Borrowers should assess their eligibility, loan tenure, and repayment preferences to select the best offering aligned with their needs.

The slight differences in interest rates can significantly affect long-term interest payments, so comparing effective rates and terms is critical for cost savings and affordability.

How to Qualify for Better Housing Loan Interest Rates?

Qualifying for better housing loan interest rates in Malaysia in 2026 requires demonstrating strong financial health, responsible credit behaviour, and meeting lender-specific criteria. Understanding what banks look for can increase your chances of securing favourable rates.

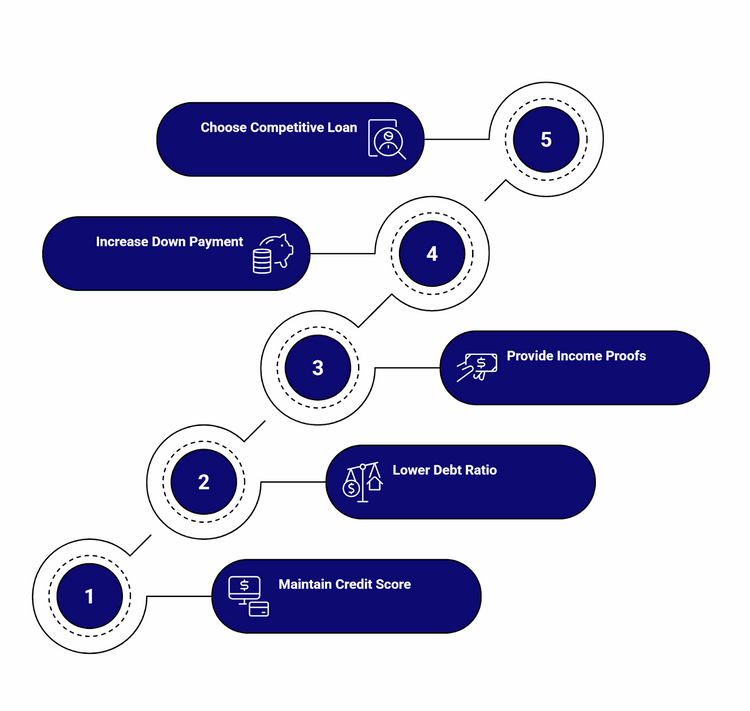

Maintain a Healthy Credit Score

- Clean credit history without defaults or loan repayments.

- Good credit reports from CCRIS and CTOS showing low-risk repayment behaviour.

- Banks give preference to borrowers with consistent and timely debt repayments.

Maintaining a good credit score signals reliability and reduces perceived lending risk, helping you qualify for lower interest rates.

Keep a Low Debt Service Ratio (DSR)

- Most banks prefer a Debt Service Ratio (DSR) below 60%, meaning your total monthly debt obligations should not exceed 60% of your net income.

- Lower DSR means more disposable income to service new loan repayments comfortably.

- High DSR reduces borrowing capacity and may lead to a higher interest rate being offered.

A manageable DSR assures lenders of your repayment capacity, improving eligibility and terms.

Provide Stable and Sufficient Income Proofs

- Evidencing steady employment with verifiable income through payslips, EPF contributions, and tax statements.

- Self-employed borrowers should present robust financial statements or tax returns.

- Higher and stable income generally qualifies for better rates and higher loan limits.

Stable income reduces lender risk and demonstrates the ability to meet loan obligations over the tenure.

Prepare a Larger Down Payment and Lower Loan Amount

- A higher upfront down payment reduces the loan quantum and risk to lenders.

- Smaller loan-to-value (LTV) ratios often attract more competitive rates.

- Demonstrates strong financial discipline and reduces the burden of monthly payments.

Adding more equity to the property signals financial stability and reduces lender risk.

Opt for Banks with Competitive and Transparent Loan Packages

- Research and compare offerings from various banks.

- Select financial institutions with good reputations and customer-friendly loan policies.

- Use facilitators or comparison tools to identify the lowest margin relative to the benchmark rate.

The right bank can offer more advantageous terms even for similar borrower profiles.

Better interest rates can significantly reduce your total loan cost over time. By managing credit risk, optimising finances, and choosing the right lender, you improve your chances of qualification in Malaysia’s competitive housing loan market in 2026.

See how much you can borrow quickly with our home loan eligibility calculator.Should You Refinance Your Housing Loan in 2026?

Refinancing your housing loan in 2026 can be a strategic financial move that helps you save money, improve cash flow, or access extra funds for other needs. Understanding the benefits and considerations will help you decide if refinancing fits your financial goals.

Benefits of Refinancing

- Lower interest rates can reduce your monthly repayments and the total interest you pay over the loan tenure.

- Ability to shorten your loan tenure, leading to quicker debt clearance and interest savings.

- Consolidate other debts into one manageable monthly repayment.

- Access equity from your property’s increased market value for renovations, education, or investment.

- Potentially switch to more flexible loan packages with beneficial terms such as lower fees or easier prepayment options.

Refinancing provides financial flexibility and cost-saving opportunities, especially when interest rates have dropped since you took out your original loan.

When to Consider Refinancing

- If current loan interest rates are significantly lower than your existing rate.

- When your property has appreciated, it increases your equity.

- If you want to reduce monthly repayments due to cash flow issues.

- To consolidate high-interest debts into a cheaper, more manageable loan.

- When you want to switch to a loan product with better features (e.g., flexibility, shorter tenure).

Timing your refinance to coincide with favourable interest rate movements and your evolving financial situation is crucial to maximising benefits.

Key Considerations

- Consider refinancing fees such as legal costs, valuation fees, and possible penalties for early settlement.

- Compare effective interest rates (including all fees) between your current loan and refinance offers.

- Assess the impact on your overall loan tenure and total interest payable.

- Ensure your credit standing and debt service ratio support refinancing approval.

Refinancing is not always beneficial if the savings do not outweigh the costs or if it extends your debt period unnecessarily.

Refinancing in 2026 makes sense for many homeowners aiming to lower costs or improve financial flexibility, especially amid stable or declining interest rates. Careful evaluation of your loan terms, costs, and financial goals is needed to make the right decision.

What Should You Keep in Mind When Making Home Loan Decisions?

Understanding how Malaysia’s housing loan interest rates work helps you compare loan options with greater clarity and confidence. By keeping track of OPR trends, reviewing loan types, checking how rate changes affect repayments, and exploring banks with competitive packages, you strengthen your ability to choose a plan that supports your long-term financial comfort.

As 2026 brings new market conditions and lending updates, staying informed and reviewing your financial readiness can help you secure better rates, whether for a new home purchase or a potential refinance.

Looking for clarity in your property search? Our property guides break it down for you.

Check out the newest launches in Malaysia and see what opportunities are coming up.