Do you know that your loan rejection will be recorded in the system for up to 12 months and affect your chances of reapplying for a loan during this period? Read on to find out how to avoid loan rejection in Malaysia.

Affordability goes hand-in-hand with financing, unless you’re paying for your property’s purchase with cash.

Get the macro perspective on housing loans, how to check home loan eligibility, and how you can use loan eligibility calculators such as LoanCare to avoid or minimise loan rejections in Malaysia.

What Happens If My Loan Application Is Rejected?

To ensure responsible and transparent financing protection for both consumers and financial institutions, banks perform a credit check on the borrower’s CCRIS report, income supporting documents, debt service ratio (DSR), and also, net disposable income (NDI) when reviewing a loan application.

For DSR, the overall acceptable average DSR is around 60%. Some banks are more lenient, going as high as 80% DSR, while some are very conservative, going as low as 40% DSR.

As for NDI, it’s a measure by banks to ensure that home loan borrowers are able to live a standard lifestyle after all the loans commitment.

So, if your profile doesn’t meet the bank’s lending criteria, your loan application will be declined and here’s what happens afterwards.

READ: 9 Reasons why banks reject your home loan

CCRIS will record loan rejection in Malaysia?

Have you ever been told that CCRIS will record your loan rejection in Malaysia? That’s actually a major misconception.

The fact is that the information about your rejected loan applications will not be included in CCRIS reports, according to Bank Negara Malaysia’s (BNM) CCRIS FAQs.

This is to ensure that any bank or financial institution you’re applying for a loan with will not be prejudiced by the decision of another bank when reviewing your loan application.

Furthermore, BNM do not place borrowers on a blacklist on CCRIS when their loan application is rejected, nor they will express any opinion about the information in the credit report.

The CCRIS report only shows the financing and repayment history of a borrower with financial institutions over the last 12 months. It doesn’t provide an assessment of a borrower’s credit standing.

Explore the latest property launches in Malaysia today!Loan rejection will be recorded by the bank, internally

However, if your application is rejected by a bank, this rejection record will remain in the bank’s internal system for 6 to 12 months, depending on the bank’s policy.

You might ask: “Can I apply for a loan again after being denied?” The answer is that you’re most likely not going to be able to obtain a loan from the same bank during this period.

Improve Your Chances of Getting A Home Loan with LoanCare

As pointed out, a loan rejection can set you back potentially up to 12 months before you can apply for another loan. Well, you could keep applying but that doesn’t bode well for your record.

So, you should only apply for a loan if you are certain about your ability to repay and the chances of getting a loan approved.

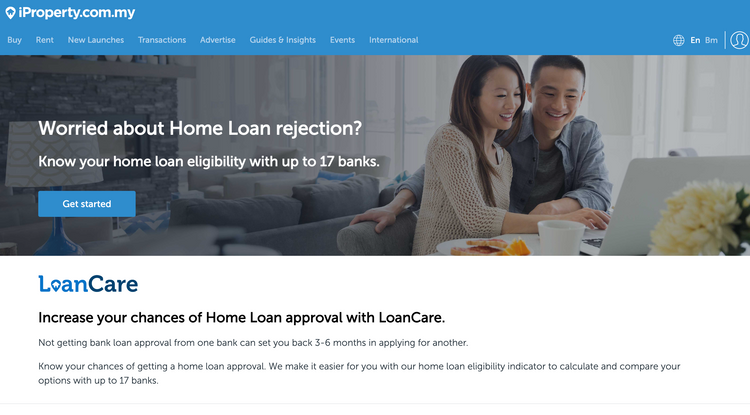

With this in mind, iProperty Malaysia has come up with a home loan eligibility calculator – LoanCare, where you’ll be able to compare loan options from 17 banks in Malaysia FOR FREE.

This is a free and easy-to-use home loan eligibility calculator which requires no registration and documents, except for minimal personal info about your financial situation.

That way, you can avoid loan rejections and the repercussions that could follow.

Searching for pre-owned properties? Explore our extensive listings here!Check Your Home Loan Eligibility with LoanCare in 5 Easy Steps

Step 1 – Visit LoanCare on iProperty.com.my

Ready? Click on ‘Get started’.

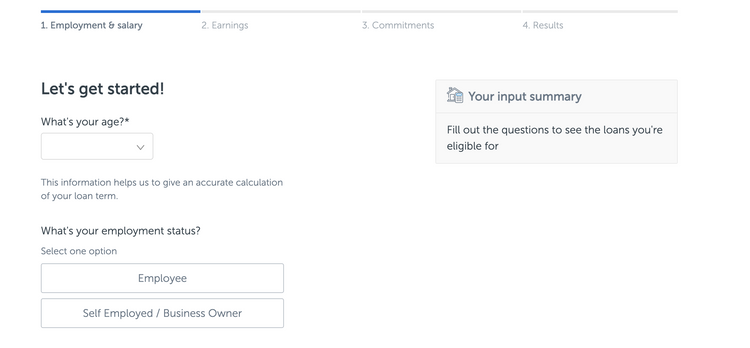

Step 2 – Provide Your Info

Fill in the fields in the respective Employment & Salary, Earnings, and Commitment sections.

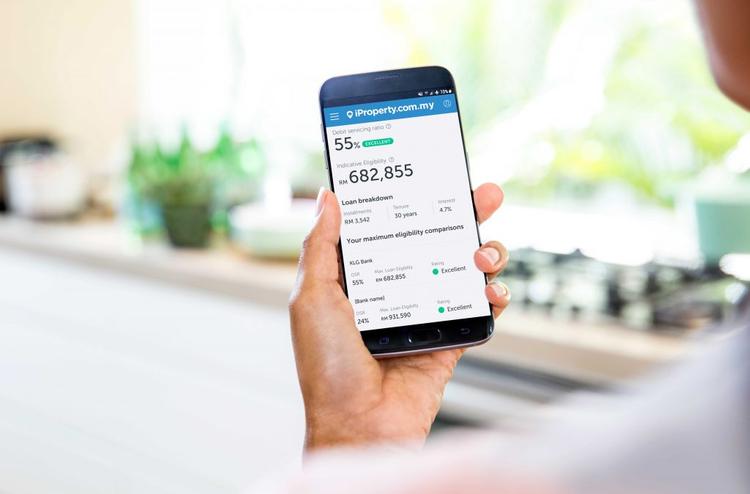

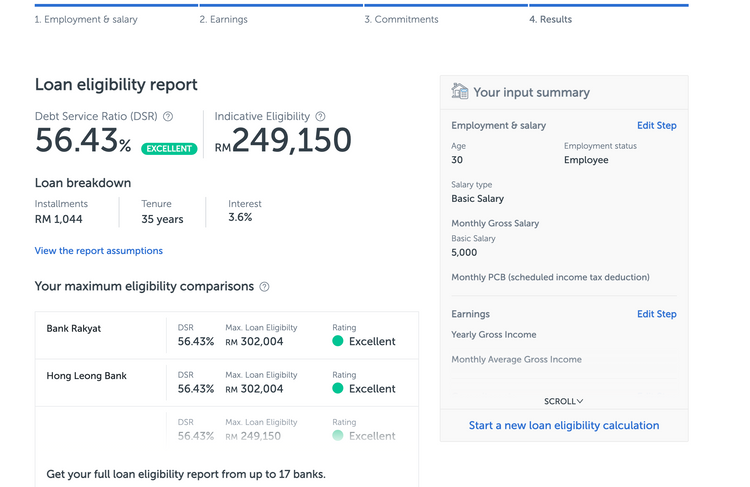

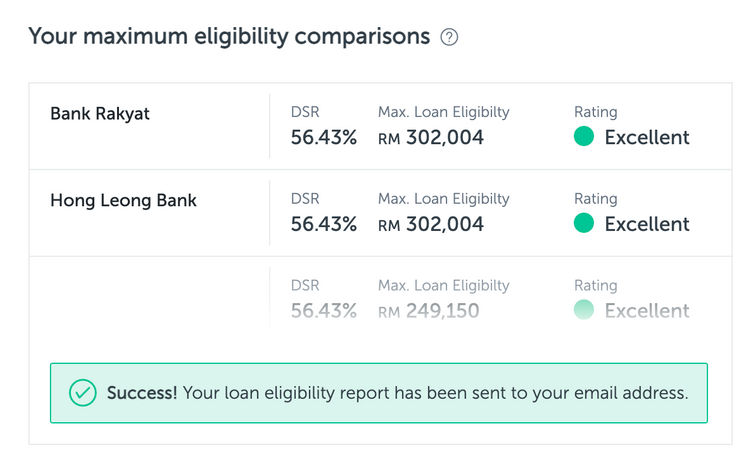

Step 3 – Review Indicative Loan Eligibility

For example, if you’re 30 years old with a monthly income of RM5,000, and have a monthly home loan repayment of RM1,500 and monthly car loan repayment of RM1,000, then the indicative borrowing amount is RM249,150.

You can edit the figures entered by clicking on ‘Edit Step’ that’s on the right column.

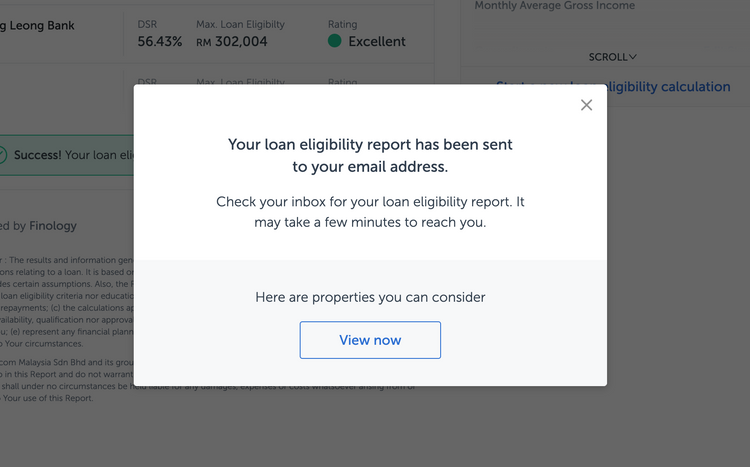

Step 4 – Enter Your Email Address To Receive the Full Loan Eligibility Report

Step 5 – Check Your Email For The Full Loan Eligibility Report

Review your home loan options from up to 17 banks and financial institutions listed below.

To assist you further, you may also refer to the links below of home loans offered by the 17 financial institutions and banks in Malaysia. They’re in no particular order.

Top housing loans in Malaysia

- Home loan packages by Maybank

- Property financing plans by CIMB

- Home and property loans by OCBC

- 5 Home Plan by Public Bank

- Home financing by RHB

- Housing loan by Hong Leong

- Loans and financing by Affin Bank

- Home Financing-i by Bank Rakyat

- Mortgages by HSBC

- Property Financing-i by MBSB

- Home financing packages by UOB

- Home and property financing by AmBank

- Home financing by Bank Islam

- Residential property financing with Bank Simpanan Nasional (BSN)

- Property loan solutions by Standard Chartered

- Housing loan by Citibank

- Property mortgages by AIA

Let Home Loan Eligibility Calculator Assist In Your Homebuying Journey

While it’s common for property buyers to apply for multiple loans to have a higher chance of securing a loan, this practice can backfire and cause applications to be rejected. Having too many applications could be seen as a red flag of your intent.

If you believe you have good finances and have done everything you need to improve or prove your creditworthiness, you can approach 2 or 3 banks to apply for a home loan.

Alternatively, check with LoanCare first, to save yourself some time and minimise the risk of your loan applications being rejected. As illustrated above, it takes just 5 quick steps, with minimal financial info required. No documents required too!

Give it a quick try, and know your options before applying for your next home loan! Try LoanCare now.

Here’s 6 Other Measures That Can Be Taken To Improve Home Loan Approvals

- Have a good credit record by keeping all payments up to date on existing credit facilities / liabilities. Without these repayment records of credit cards or other financial commitments, the bank isn’t able to assess whether you’re a good paymaster or not.

- The ability to prove financial capability to make monthly payments, and/or reduce your loan commitments and debts.

- Fully and accurately disclose all information about your financial position when applying for a home loan. Be sure to also submit all the right documents that the bank requires.

- Home buyers may also want to consider available government housing schemes and incentives.

- Understand and accept the reasons for loan rejection

- Stay updated on BNM’s borrowing regulations

READ MORE: