Understand what CCRIS is, how it affects loan approvals in 2026, and how it differs from CTOS. Learn how to check your eCCRIS report, fix common issues, and build a strong 12-month repayment record to improve your home loan eligibility and interest rates in Malaysia.

When you apply for a home loan, personal financing, credit card, or any central credit facility in Malaysia, there’s something behind the scenes that matters just as much as your income: CCRIS. Short for the Central Credit Reference Information System, CCRIS is effectively the backbone of credit evaluation used by banks and financial institutions.

For many potential borrowers, not understanding CCRIS means risk; being unaware of negative records, missing repayment entries, or how loan applications are tracked can significantly reduce your chances of approval or even lead to higher interest rates.

In this guide, we’ll explain what CCRIS is, step-by-step how to check your CCRIS score, the real-life implications for loans, how it stacks up against CTOS, how bankruptcies affect credit risk, and practical tips to improve your credit health. By the end, you’ll understand why CCRIS is not just a formality but a critical tool in your financial planning.

What Is CCRIS?

CCRIS (Central Credit Reference Information System) is the official credit database maintained by Bank Negara Malaysia (BNM).

It collects and stores 12 months of credit information from participating licensed financial institutions, banks, development finance institutions, and other credit-only lenders.

Key features of CCRIS:

- Data Source: Only from financial institutions (banks, credit providers).

- Coverage: Outstanding credit, type of facility, instalment amount, payment history for the past 12 months, loan applications, and special attention (i.e., performance-watch) accounts.

- No Numeric Score: Unlike private bureaus, CCRIS does not give you a “credit score.” Instead, it provides factual credit records (payment history, current debt, applications), not an opinionated rating.

- Update Frequency: CCRIS data is updated monthly, typically around the 10th, based on records submitted by financial institutions.

Why it exists: CCRIS helps banks and credit institutions assess lending risk by using a standardised, centralised repository. According to the ASEAN credit registry framework, CCRIS is a key risk-mitigation mechanism regulated by BNM.

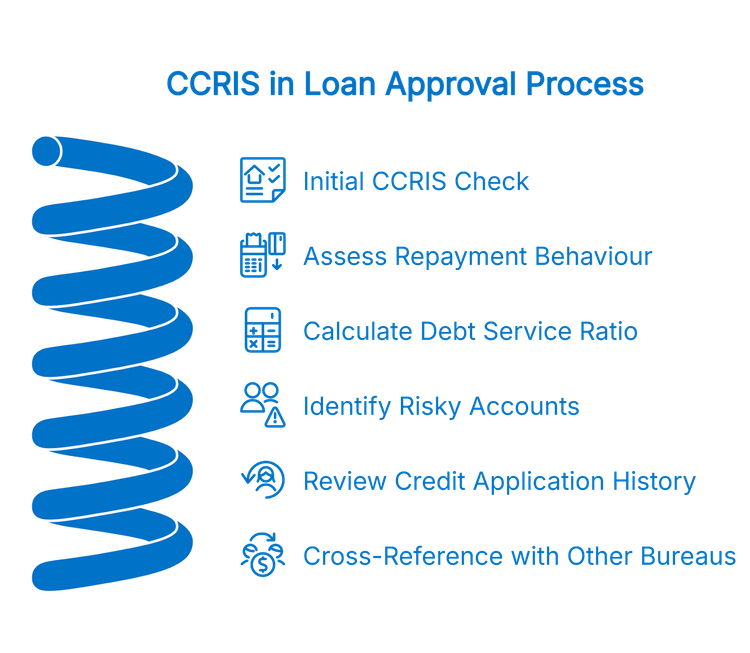

How Lenders Use CCRIS: Real-World Implications

For credit providers, CCRIS is one of the first checks during loan approval.

Here’s how it factors in:

1. Assessing Repayment Behaviour

- Lenders look at each facility’s 12-month repayment pattern (on-time vs late).

- Patterns of “0” in monthly repayment grids (on-time payment) are ideal.

2. Calculating Debt Service Ratio (DSR)

- Outstanding instalments are added to a borrower’s monthly obligations.

- High outstanding debt or many facilities can push DSR too high.

3. Identifying Risky Accounts

- CCRIS flags Special Attention Accounts (SAA), accounts in distress, being restructured, or under collection.

- These are red flags. Even a single SAA entry can drastically reduce creditworthiness.

4. Credit Application History

- All loan applications in the past 12 months are recorded, whether approved or rejected.

- Many recent applications may suggest financial instability or desperation.

5. Cross-Referencing with Other Bureaus

- Banks typically don’t rely solely on CCRIS. They may also check CTOS or Experian for litigation, public records, or business data.

CCRIS is not merely a report; it’s the first impression you give to lenders. Keeping your recent repayment behaviour strong can be the difference between a smooth approval and a rejected application.

How to Check CCRIS Score?

Knowing how to check your CCRIS is critical, especially if you’re planning a loan application soon.

Here’s a step-by-step guide:

Step 1: Register for eCCRIS

- Go to the eCCRIS portal (BNM’s official CCRIS site).

- Fill in personal info: name, MyKad number, date of birth, mobile number, and email.

- You’ll authenticate your identity via an OTP or a small RM1 “micro-transfer” (automatically refunded) to confirm account ownership.

- After verification, you will set up your user ID, password, and security questions.

Step 2: Log In & View Report

- Use your credentials (User ID, password, and OTP) to log in to eCCRIS.

- You’ll be able to download or view your full CCRIS report, including credit facilities, payment history, applications, and SAAs.

Step 3: Alternative Access Methods

- CCRIS Kiosk: Located at BNM branches or AKPK offices. Bring your MyKad, and you can get a printed report immediately.

- Request by Mail: Submit a CCRIS credit report request form (including MyKad copy, proof of address) to BNM Tele-Link.

- In-Person at BNM: Bring ID; you can request a report with the staff’s help.

Step 4: Read and Interpret Your CCRIS Report

- The repayment history is shown month-by-month with codes:

- 0 = paid on time

- 1 = 1 month late

- 2 = 2 months late

- 3 = 3+ months late or severely overdue

- 0 = paid on time

- Check all active credit facilities and their outstanding balances.

- Look for any Special Attention Accounts, and note whether they are being resolved.

Step 5: Dispute Incorrect Entries (if any)

- If you spot inaccurate data (wrong balance, missing account, wrong status), you can file a data verification request via eCCRIS.

- The financial institution or BNM is required to investigate and correct within a set timeframe (often up to 14 days).

By checking your CCRIS early and correcting any discrepancies, you protect your credibility with lenders and avoid unwelcome surprises during loan approvals.

Know your affordability before shortlisting, and check the instalments.Difference Between CCRIS vs CTOS: A Detailed Comparison

Here’s a side-by-side comparison of CCRIS and CTOS, highlighting their significant differences, advantages, and how lenders use them:

| Feature | CCRIS (Bank Negara) | CTOS (Private Credit Bureau) |

| Managed by | Bank Negara Malaysia | CTOS Data Systems Sdn Bhd (private) |

| Data Sources | Financial institutions/banks only | Legal records, insolvency (MDI), SSM, trade references, CCRIS data, court actions |

| Type of Report | Historical & factual credit activity (12 months) | Comprehensive credit report with additional litigation and business data |

| Credit “Score” | No numeric score | Yes, the CTOS Score is typically from 300 to 850 |

| Data Retention Period | 12 months (rolling) | Long-term/”permanent” in terms of public records + CCRIS data |

| Usage | Primary for banks to assess credit risk | Used by banks + legal firms + businesses for deeper risk profiling |

| Cost to Access | Free via eCCRIS (after initial registration) | Fee-based for full credit reports/score (e.g., MyCTOS Score Report RM 27) |

| Ability to Dispute | Yes, via eCCRIS, financial institutions must review and correct data | Yes, via the CTOS platform, depending on the data source |

By keeping both CCRIS and CTOS clean and up to date, you improve your chances of faster approvals and better financing terms.

Bankruptcy & Credit Risk in Malaysia: 2026 Snapshot

To understand why CCRIS matters, it’s helpful to look at the broader context of insolvency and debt risk in Malaysia.

- According to the Malaysian Department of Insolvency (MDI), civil servants accounted for 10-13% of new bankruptcy cases between 2021 and 2024.

- The MDI director-general expressed concern that this growing trend among public sector staff could reflect financial stress in a traditionally stable-income group.

- While the overall national bankruptcy rate has seen varying trends, the rising proportion of civil servant insolvencies underscores how even salaried individuals can be exposed to debt risk when credit behaviour is unmanaged.

Bankruptcy Statistics Table (MDI)

| Year | % of New Bankruptcies by Civil Servants |

| 2021 | 10% |

| 2022 | 11% |

| 2023 | 13% |

| 2024 | 14% (as of data quoted by MDI DG) |

Interpretation:

This data suggests a non-trivial portion of bankruptcies in recent years came from public servants, implying that financial discipline and credit monitoring (such as via CCRIS) are increasingly important, even for stable-income earners.

This rising exposure to credit distress underscores why Malaysians, even those in secure employment, must closely monitor their CCRIS records to protect their long-term financial well-being.

Benefits of a Good CCRIS Status

Having a clean or positive CCRIS credit record brings significant advantages when applying for loans or other credit facilities.

Here’s how:

| Benefit | How It Helps You |

| Higher Loan Approval Chance | Lenders see low risk when your repayment behaviour shows zero or minimal late payments. |

| Better Interest Rates/Terms | Demonstrated discipline may give you access to lower rates or more favourable financing packages. |

| More Negotiation Power | When your CCRIS is clean, you have leverage to negotiate for larger loan amounts or better terms. |

| Faster Processing | Banks prioritise applications from borrowers with good credit history, reducing friction and delays. |

| Access to Premium Credit Products | Good credit profiles may unlock premium credit cards, higher-limit facilities, or investment financing. |

| Credit Monitoring & Discipline | Regularly checking your CCRIS encourages responsible borrowing and early correction of mistakes. |

Example benefit: Suppose you are applying for an RM 500,000 home loan over 30 years. Even a 0.25% lower interest rate (because your credit is strong) can save you thousands of ringgit over the tenure. Lenders may reward low-risk profiles, making CCRIS management very worthwhile.

In 2026, maintaining strong credit discipline is one of the smartest investments you can make.

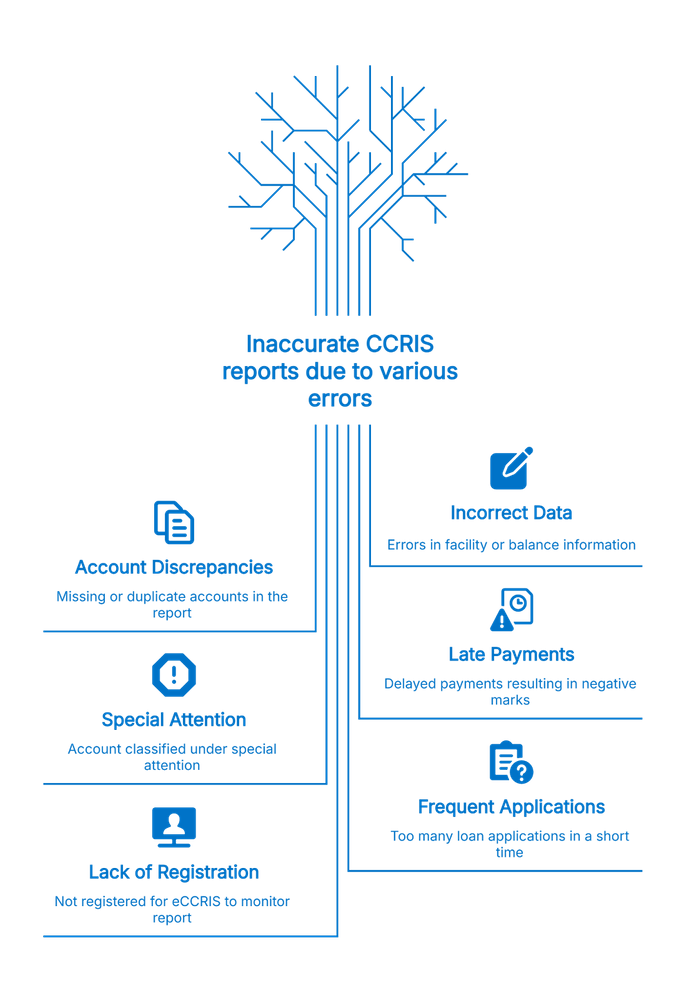

Common CCRIS Problems & How to Fix Them

Even with the best intentions, CCRIS reports may contain problematic entries. Here are typical issues and how to address them:

1. Incorrect Facility or Balance

- Solution: Identify the error, file a data verification request via eCCRIS. The financial institution must correct the data.

2. Missing or Duplicate Accounts

- Solution: Compare your CCRIS report with your bank statements. Highlight discrepancies, request updates.

3. Late Payment Marks (1/2/3)

- Solution: Pay your upcoming instalments on time. After 12 months, if all are “0”, that history becomes stronger.

4. Special Attention Account (SAA) Reporting

- Solution: Engage with your lender, settle arrears, adhere to the repayment plan, and ask for reclassification once in good standing.

5. Frequent Loan Applications

- Solution: Limit the number of credit applications. Wait before applying for new credit; multiple enquiries show up on CCRIS.

6. Not Registered for eCCRIS

- Solution: Register via eCCRIS, verify your identity via OTP or micro-transfer, and monitor your report monthly.

By actively monitoring and correcting these issues early, you keep your credit profile strong and your future borrowing power firmly in your hands.

How to Improve Your CCRIS Over 6-12 Months: A Practical Plan?

If your CCRIS record needs work, here’s a realistic, actionable 6-12 month plan to improve:

Months 1-3

- Register for eCCRIS (if not already).

- Pull your CCRIS report and check for errors.

- Make sure all current credit facilities are tracked and up to date.

- Start making payments strictly on time and eliminate “1” or “2” marks.

Months 4-6

- Pay down credit card outstanding balances. Aim for under 30% utilisation.

- Avoid applying for new credit unless absolutely needed.

- Negotiate with lenders if any facility is strained: consolidation, refinancing, or restructuring.

Months 7-12

- Maintain consistent on-time payments; target a clean 12-month repayment pattern.

- Recheck CCRIS every 3-6 months to monitor changes.

- If you have or had an SAA, actively work with your institution to rehabilitate, and stick to your repayment plan.

- Avoid aggressive debt, aim for a debt-to-income ratio (including instalments) that stays well-manageable.

By the end of the year, you should ideally have built a clean 12-month payment history, which looks very attractive to banks.

Why CCRIS Is More Important Than Ever in 2026?

Before diving into the key shifts, it helps to understand why CCRIS has suddenly become a bigger part of the conversation among Malaysian borrowers and home seekers.

- Data Security & Access Changes: In 2025, BNM temporarily suspended access to CCRIS for credit reporting due to data security concerns. Even though this affected CRAs like CTOS, BNM clarified that individuals can still access their own CCRIS via eCCRIS.

- Rising Bankruptcy Risk: With civil servant insolvency clearly on the rise (10-13% of new bankruptcy cases), CCRIS is a key risk indicator for lenders.

- Loan Scrutiny Intensifying: In a tighter lending climate, banks are even more stringent on credit history. A clean CCRIS can be a game-changer.

- Financial Planning Tool: More borrowers are using CCRIS proactively (not just when applying for credit) to monitor and correct their credit health.

Taken together, these shifts reinforce one message: keeping your CCRIS clean is no longer optional; it is essential to safeguard your financial future and improve your home-loan eligibility.

Your CCRIS Matters

What is CCRIS? It’s your credit story in numbers, not a “core,” but a record of how you’ve borrowed, how you repay, and how disciplined you are. For any Malaysian applying for a loan in 2026, understanding CCRIS is non-negotiable.

How to check your report? Use eCCRIS, visit a kiosk, or apply via BNM. Read your report thoroughly, spot errors, and act on them.

Why improve it? A clean CCRIS helps you get loans faster, negotiate better rates, and access premium financial products.

Simple steps for you:

- Register and check your eCCRIS report today.

- If you’ve got past arrears, build a 12-month clean payment history.

- Use your improved CCRIS when applying for a home loan; it could save you significant money, improve your approval odds, and strengthen your negotiation power.

Check out the latest sales listings from iProperty Malaysia now to browse floor plans, pricing, and developer promos.