CCRIS and CTOS are key credit reports used by Malaysian banks for home loan approvals. CCRIS shows your recent 12-month repayment history, while CTOS provides a broader credit profile and a 300-850 score. Managing both improves your approval chances in 2026.

Buying your first home in Malaysia can feel overwhelming, especially for a first-time home buyer dealing with credit checks, loan approvals, and ever-changing government schemes.

This guide simplifies the process for first-time buyers, explaining CCRIS and CTOS, the home loan approval process Malaysia, and the latest updates from Budget 2026 to help you make informed decisions and improve your chances of loan approval.

What Is CCRIS?

The Central Credit Reference Information System (CCRIS) is a centralised credit reporting system managed by Bank Negara Malaysia. It collects and consolidates credit-related information from participating financial institutions across Malaysia.

The CCRIS report provides a comprehensive snapshot of an individual’s credit history, including loan records, payment behaviour, and any legal actions related to credit. This report plays a crucial role in financial institutions’ loan approval decisions by showing a borrower’s creditworthiness.

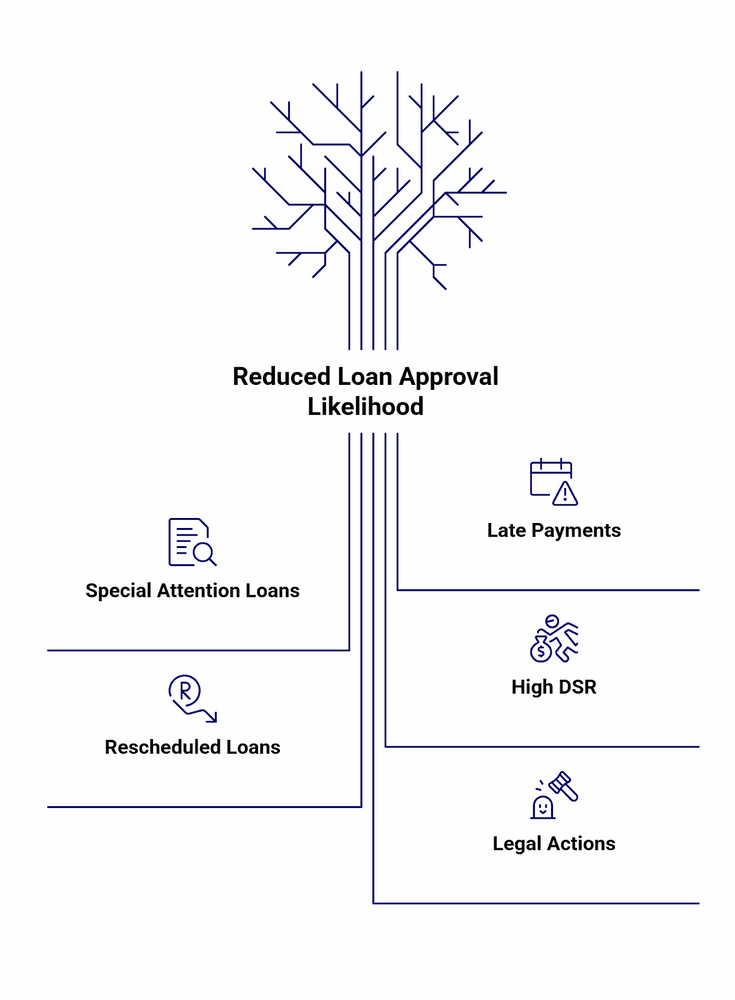

5 CCRIS Red Flags That Affect Loan Approval

Loan approval can be negatively impacted by several red flags within the CCRIS report that indicate financial risks to lenders. Key red flags include:

- Late Payments: Records of overdue payments or of consistently paying loans late are marked in the CCRIS report, which can impact creditworthiness.

- Loans Under Special Attention: Accounts flagged for close monitoring due to payment difficulties or restructuring.

- High Debt Service Ratio (DSR): When monthly debt obligations exceed a certain percentage (often 60%) of monthly income, it lowers loan approval chances.

- Rescheduled or Restructured Loans: A History of loan repayment rescheduling or restructuring signals potential repayment issues.

- Legal Actions or Bankruptcy: Any legal proceedings or bankruptcy information will reduce the likelihood of loan approval.

These factors indicate potential repayment risks, and addressing them is essential to maintain good credit standing and improve loan approval outcomes in 2026.

How to Check Your CCRIS Report in 2026

Checking your CCRIS report is straightforward and can be done through multiple channels, with an increasing push towards digital access:

- eCCRIS Online Portal: The most convenient method is through Bank Negara Malaysia’s eCCRIS online platform, which provides free, secure access to your credit report anytime after online registration.

- Registration Requirements: Individuals must register by verifying their identity in person at Bank Negara’s office or an AKPK branch, linking their MyKad and mobile number, and receiving a six-digit PIN for secure login.

- Walk-in Access: People can still visit Bank Negara Malaysia or use the on-site credit kiosks to obtain immediate report access by submitting identification documents.

Once accessed, the report will show detailed loan records, payment history, and any special notes on loans or credit applications, helping users fully understand their credit status.

Estimate your monthly payments in seconds with the mortgage calculator.What Is CTOS?

CTOS, or CTOS Data Systems Sdn. Bhd. is a private credit reporting agency in Malaysia operating under the Credit Reporting Agencies Act 2010. Unlike CCRIS, which Bank Negara Malaysia manages, CTOS functions independently and compiles credit information from a variety of sources beyond just financial institutions.

The agency provides a credit score ranging from 300 to 850 that reflects an individual’s creditworthiness and helps lenders assess the risk of lending to that person.

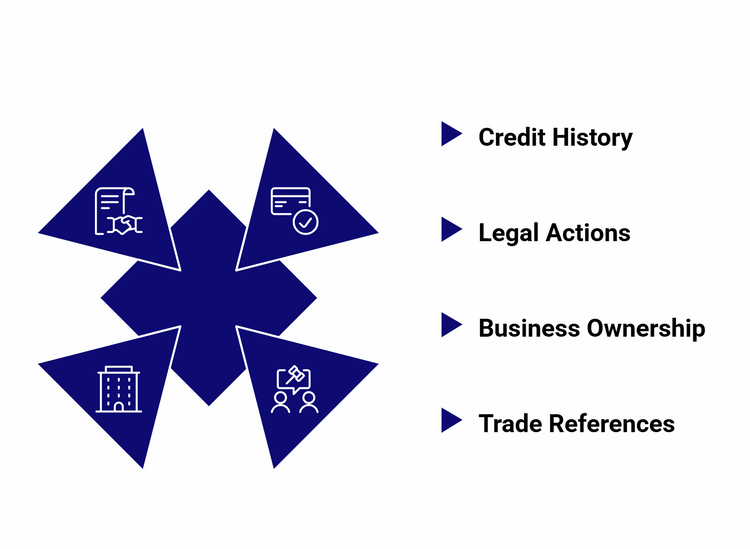

What CTOS Tracks and Why Banks Rely on It?

CTOS gathers information from public sources, including legal notices, the Companies Commission of Malaysia (SSM), the Insolvency Department, and other government registries. This data includes:

- Credit repayment history sourced from CCRIS

- Legal actions like bankruptcies and court summons

- Business ownership details and company filings

- Trade references and non-bank credit defaults

Banks and financial institutions use CTOS reports, including credit scores, because they provide a broad, consolidated view of an individual’s or company’s economic behaviour and legal status, supplementing the raw credit data from CCRIS.

CTOS vs CCRIS: What First-Time Buyers Should Understand

For first-time homebuyers, understanding CTOS and CCRIS is essential because both reports influence loan approval. Each provides different credit details to help buyers manage their profiles more effectively.

| Feature | CCRIS | CTOS |

| Managed by | Bank Negara Malaysia (BNM) | CTOS Data Systems Sdn. Bhd. (Private company) |

| Data sources | Banks and financial institutions only | Banks, public agencies, legal firms, SSM, the insolvency department, etc. |

| Type of data | Raw credit data, including the recent 12 months | Consolidated credit score and detailed financial/legal info |

| Credit score provided | No | Yes (range: 300 to 850) |

| Data retention | Up to 12 months of recent credit history | Permanent records create a historical archive |

| Usage | Primary tool for monitoring loan repayments | Used alongside CCRIS for broader credit risk assessment |

CCRIS shows recent bank repayment records, while CTOS provides a broader credit view with additional data and a score. Checking both helps first-time buyers understand their credit standing and improve their chances of loan approval.

Estimate your monthly instalments in seconds with our mortgage payment calculator for quick results.How does CTOS affect the Home Loan Approval Process in Malaysia?

Understanding how CTOS affects the home loan approval process Malaysia helps first-time buyers figure out what banks look at beyond basic repayment records. CTOS scores, past credit behaviour, and public records all play a role in how lenders assess risk before approving a mortgage.

1. CTOS Provides a Comprehensive Credit Risk Profile

CTOS is a crucial tool used by banks in Malaysia to assess home loan applications. It does this by providing a detailed credit report and a credit score that reflects an individual’s financial behaviour, including repayment history, outstanding debts, legal issues, and bankruptcies. This gives lenders a broader understanding of a borrower’s creditworthiness beyond the recent 12-month payment data found in CCRIS.

2. Banks Use CTOS Scores and Reports to Evaluate Loan Applicants

Banks consider the CTOS credit score, which ranges from 300 to 850, as an indicator of loan risk. Scores above 650 generally improve approval chances and loan terms, while scores below 500 often lead to rejections. Banks also review CTOS for negative records such as legal cases, defaults, or bankruptcy, which can severely impact home loan approval.

3. CTOS Reports Complement CCRIS Information

While CCRIS tracks payment history with financial institutions, CTOS adds insights from legal and business records, offering a fuller credit profile. Banks rely on both reports to safeguard lending by identifying risks not visible in CCRIS alone.

Understanding and managing your CTOS report is essential for a smooth home loan application and a successful homeownership journey.

Planning to apply for a home loan? Learn the four essential documents you must have ready.

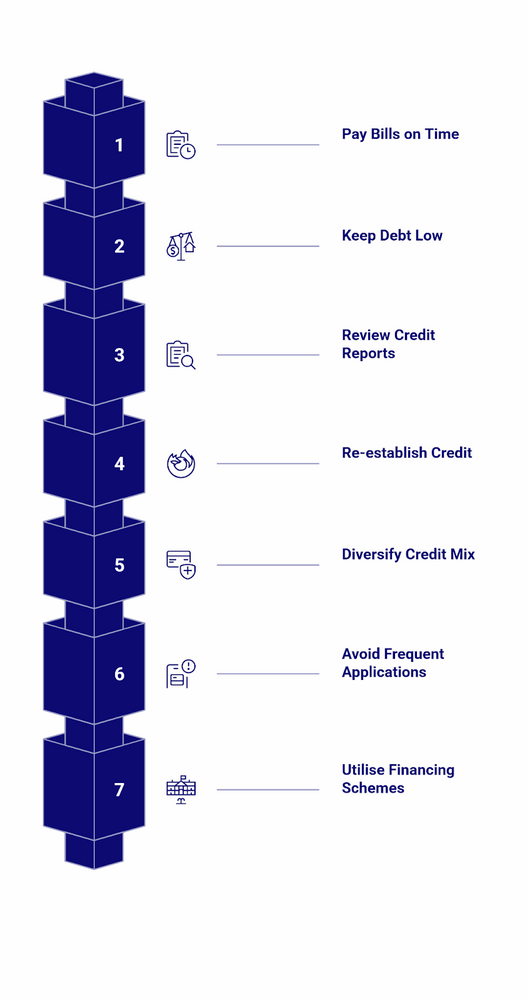

7 Steps to Improve Your Credit Health Before Applying

Understanding CTOS and CCRIS helps first-time buyers understand how banks evaluate loan applications and manage their credit more effectively.

Step 1. Pay Your Bills on Time Every Month

Consistently making timely payments on all your debts, including credit cards, personal loans, and utilities, is the most critical factor in improving your credit health. Even making minimum payments on credit cards if you cannot afford the full balance helps maintain a positive record. Late payments appear on your CTOS report and negatively affect your credit score.

Step 2. Keep Your Debt Levels Low

Maintain low outstanding balances by regularly paying down debts. Aim to keep credit utilisation, the ratio of credit card balances to credit limits, below 30%. Avoid borrowing more than necessary and reduce overall debt steadily to demonstrate financial discipline to lenders.

Step 3. Regularly Review and Correct Your Credit Reports

Obtain copies of your CTOS and CCRIS reports frequently to check for inaccuracies or outdated information. Dispute and correct any errors immediately to ensure your credit report accurately reflects your financial status, preventing undue damage to your credit reputation.

Step 4. Re-establish Credit History if You Have Past Issues

If you have a poor credit history, work on rebuilding it responsibly by avoiding drastic actions such as closing many credit accounts or opening multiple new ones at once. Seek advice from credit counsellors or financial advisors to develop a tailored credit improvement plan.

Step 5. Diversify Your Credit Mix Responsibly

Having a mix of credit types, such as credit cards, personal loans, and instalment loans, can boost your CTOS score by showing lenders you can handle various financial obligations. However, avoid applying for multiple new credit facilities simultaneously.

Step 6. Avoid Frequent Loan Applications

Multiple recent loan or credit inquiries can lower your score and signal financial distress to lenders. Apply selectively and space out credit requests to maintain a stable credit profile.

Step 7. Utilise Government or Islamic Financing Schemes

These schemes often have more flexible credit requirements and can be an option for those improving their credit scores while still needing financing.

- LPPSA (Lembaga Pembiayaan Perumahan Sektor Awam): A government-backed loan scheme for Malaysian public sector employees, providing up to 100% financing with low fixed interest rates and longer repayment tenures, including the Skim Pembiayaan Perumahan Muda (SPPM) for young public servants aged 30 and below with extended tenures of up to 40 years.

- SJKP (Skim Jaminan Kredit Perumahan): A housing credit guarantee scheme designed to help individuals without fixed income, such as gig workers and small traders, to secure home loans with government guarantees. It offers financing up to RM500,000 to cover the purchase price and related fees, with flexible eligibility criteria.

- Maybank Islamic HouzKEY: An Islamic home financing product offering up to 100% financing for eligible properties, designed to provide Shariah-compliant home financing solutions.

Improving your credit health before applying for a home loan requires disciplined financial behaviour, including timely payments, debt reduction, regular credit report monitoring, and responsible credit management. These steps collectively enhance your CTOS score and credit profile, increasing your chances of loan approval and access to better lending terms in 2026.

Check your eligibility in minutes with our home loan eligibility calculator.Home Loan Approval Process for First-Time Buyers in 2026

For first time home buyers in Malaysia, the home loan approval process Malaysia in 2026 focuses on three main areas: your credit profile (CCRIS/CTOS), your ability to repay (income and debt-to-service ratio), and the property’s value and eligibility.

Banks generally follow a standard flow: pre-approval, formal application, credit checks, valuation, and legal documentation, which may take about three to six months from application to key handover.

Understanding the required down payment, upfront costs, and how joint applications work will help you prepare a stronger and more confident home loan application.

Required down payment and upfront costs

Understanding the upfront costs helps first-time buyers plan their finances better and avoid unexpected expenses when securing a home loan.

- Minimum down payment (LTV rules)

For most first-time buyers, the standard minimum down payment is about 10% of the purchase price, with banks offering up to 90% margin of financing for an owner-occupied first residential property.

Some special schemes (e.g., selected “first home” or government/Islamic packages) may offer higher funding of 100-110%, effectively reducing or covering the down payment for eligible buyers.

- Legal fees, valuation fees and stamp duty

Beyond the down payment, you must budget for legal fees (Sale and Purchase Agreement and loan agreement), stamp duty on the transfer (MOT/SPA) and loan, and property valuation fees.

These upfront costs typically amount to 3-5% of the property’s price. However, first-time buyers enjoy stamp duty exemptions or discounts on properties up to a specified price threshold (for example, exemptions for properties up to RM500,000 extended to first-time buyers under recent budgets).

- Insurance/takaful and other incidentals

Banks usually require mortgage protection, such as MRTA/MLTA (or Islamic equivalents), which can be paid upfront or financed into the loan, plus minor charges such as disbursements, government search fees, and loan processing charges.

Planning for these items helps avoid cash flow surprises at signing. By factoring in the down payment, legal fees, stamp duty and other mandatory charges, buyers can prepare a realistic budget and reduce last-minute financial stress during the purchase process.

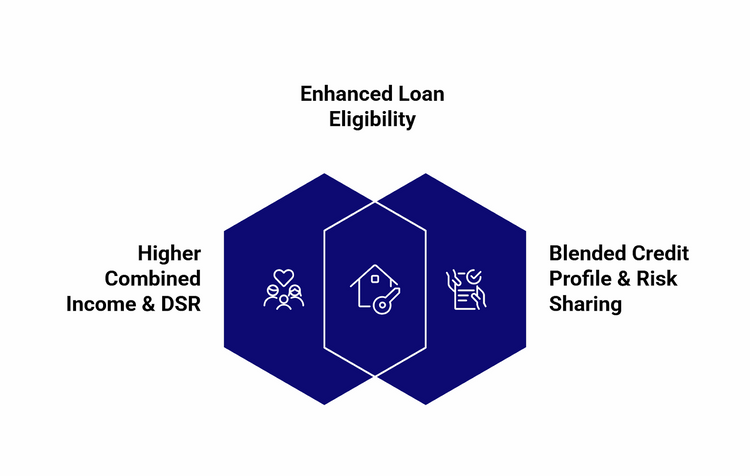

How do joint applications help first-time buyers?

Joint applications offer first-time buyers a practical way to strengthen their loan eligibility. By combining income and credit profiles, banks get a clearer picture of overall financial stability, which can improve approval chances.

- Higher combined income and stronger DSR

A joint application (e.g., with a spouse or immediate family) allows banks to assess combined gross income, which can significantly improve the debt service ratio (DSR) and increase the maximum eligible loan amount. This is useful when one borrower’s income alone is not enough to qualify for the desired property price or tenure.

- Blended credit profile and risk sharing

In a joint home loan, banks review both applicants’ CCRIS/CTOS reports and overall credit health, which means a co-borrower with stronger credit can sometimes help offset a weaker profile.

However, serious red flags (e.g., delinquency or legal action) for either party can still lead to rejection. Joint ownership also spreads long-term repayment responsibility, but both parties are fully liable if repayments are missed.

- Long-term planning and eligibility for future loans

Using a joint application for the first property can help secure better financing now. Still, it may affect future borrowing capacity for both borrowers, since the full instalment usually counts towards each person’s DSR.

First-time buyers should balance the immediate benefit of higher approval odds with their long-term plans, such as upgrading or buying an investment property later.

A joint home loan can boost affordability and approval strength, but it also links both parties to the same long-term repayment and future borrowing limits. First-time buyers should weigh the immediate benefits against long-term financial goals before deciding.

Browse properties for sale all over Malaysia.Latest 2026 Government Schemes for First-Time Home Buyers in Malaysia

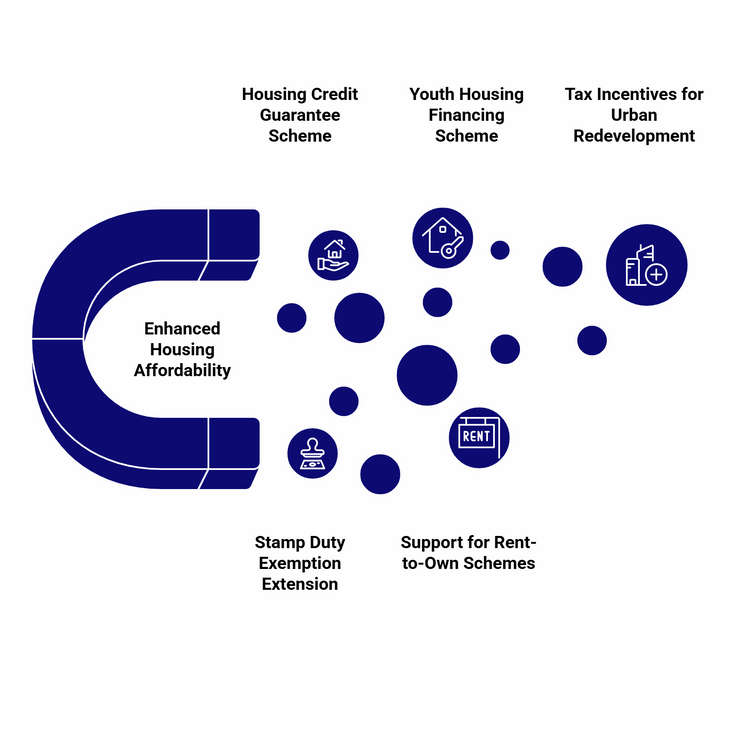

The Malaysian government has introduced and enhanced several schemes in 2026 to make homeownership more accessible and affordable for first-time buyers:

- Housing Credit Guarantee Scheme (SJKP): Allocation doubled to RM20 billion to assist up to 80,000 first-time buyers, especially gig workers and self-employed individuals, by providing government-backed guarantees for housing loans even without fixed income documentation. This scheme aims to expand homeownership among non-traditional earners.

- Stamp Duty Exemption Extension: Full stamp duty exemption on both the instrument of transfer and loan agreements for residential properties priced up to RM500,000 has been extended until December 31, 2027. This significantly reduces upfront costs for first-time buyers, easing financial burdens.

- Youth Housing Financing Scheme (LPPSA): Extended through 2026 with an increased financing limit of up to RM1 million, targeting roughly 48,000 young civil servants, enabling them to purchase or upgrade homes with government support.

- Support for Rent-to-Own and Build-Then-Sell Schemes: The government encourages financial institutions to develop flexible homeownership options through rent-to-own and build-then-sell programs, which offer alternative paths to homeownership for middle-income groups.

- Tax Incentives for Urban Redevelopment: A special 10% tax deduction (capped at RM10 million) is offered for renovations or the conversion of commercial buildings into residential units, supporting urban housing supply.

These initiatives collectively aim to lower financial barriers, widen access to financing, and stabilise housing affordability for first-time buyers in Malaysia throughout 2026 and beyond.

Is Your First Home Loan Application Ready for 2026?

Buying your first home in Malaysia becomes much easier when you understand how CCRIS, CTOS, income stability, DSR, and government schemes shape your approval chances.

By checking your credit reports early, planning your down payment, estimating upfront costs, and considering options like joint applications, you create a stronger and more confident path to homeownership.

With clear preparation and the correct information, navigating the 2026 home loan approval process becomes far less overwhelming and far more achievable.

Explore our easy property guides for every stage of your journey, from buying your first home to selling with confidence.

Get the latest updates on new launches across Malaysia and find fresh opportunities that match your goals.