A CTOS score is a three-digit credit rating (300-850) used by Malaysian banks to assess your loan risk. In 2026, a higher score improves your chances of home loan approval and better interest rates, while a lower score can lead to stricter terms or rejection.

A CTOS score is a three-digit credit rating, typically ranging from 300 to 850, used by Malaysian banks to assess how risky it is to lend you money. In 2026, lenders rely on it heavily for home loan approvals, interest rate decisions, and loan amounts. A higher score signals strong repayment behaviour and improves your chances of securing better mortgage terms, while a lower score may lead to stricter conditions or rejection.

Buying a home feels exciting until your loan application hits a roadblock because of a low CTOS score. Many Malaysians don’t realise how much their credit standing affects bank approval until it’s too late.

If you’ve been wondering what is CTOS and how to improve CTOS score before applying for a home loan, this guide is for you. We’ll break down easy, practical steps to help you strengthen your credit profile so you can boost approval chances and secure better financing terms.

What Is CTOS Score and Why Do Banks Check It?

Banks check CTOS scores in 2026 because they want a quick, objective way to judge how risky it is to lend you money. A strong score signals “low risk” and can mean smoother approvals and better interest rates, while a weak score can trigger rejections or stricter terms.

A CTOS score is a three‑digit number, usually ranging from 300 to 850, that sums up your creditworthiness based on your past and current borrowing behaviour. It is generated by CTOS, a private credit reporting agency in Malaysia, using data such as your repayment history, outstanding debts, credit history length, credit mix, and newly opened credit lines.

Banks still rely heavily on CTOS scores to quickly assess how likely you are to repay a home loan on time and in full. A higher CTOS score generally improves your chances of loan approval and can support better pricing. In comparison, a lower score may lead to smaller approved amounts, higher rates, or outright rejection, especially when paired with weak income or high existing commitments.

Check your monthly repayments with our easy mortgage calculator.How CTOS Data Affects Your Home Loan Approval

When applying for a home loan in Malaysia, banks rely heavily on your CTOS score to evaluate your financial trustworthiness. This score reflects your creditworthiness based on your repayment history, outstanding debts, and legal records, giving lenders a clear picture of your risk level.

A strong CTOS score signals reliability, increasing your chances of loan approval and favourable interest rates. In contrast, a low score can lead to delays, higher rates, or outright rejection due to perceived risk.

Minimum CTOS Score Usually Needed for Mortgage Applications

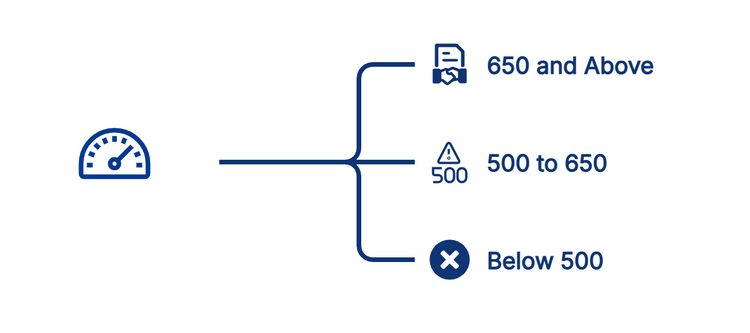

A CTOS score plays a significant role in how banks assess your home loan strength. While each bank has its own internal guidelines, most follow similar risk tiers when reviewing mortgage applications.

- 650 and above: Usually seen as a healthy score with better approval chances and more competitive interest rates.

- 500 to 650 range: Possible to get approved, but banks may offer higher interest rates, lower loan amounts, or stricter terms.

- Below 500: Considered high risk; most applications are rejected unless strong financial proof is provided.

- Borrowers with stable income and low debt often get more flexibility even if their score sits slightly below ideal levels.

- Lifting your score past 650 can create a noticeable difference in loan outcomes and overall borrowing cost.

A stronger CTOS score not only boosts approval chances but also helps you secure a home loan with better repayment terms.

How to Check Your CTOS Report in Malaysia

Checking your CTOS report helps you proactively manage your credit standing before applying for a home loan. In 2026, the process is quick, digital, and can be done via multiple platforms.

Ways to Check Your CTOS Report (2026)

- Register online at the CTOS website for a MyCTOS account

- Use the MyCTOS mobile app, available on iOS and Android

- Purchase via Touch ‘n Go (TnG) eWallet mini-program

- Visit a CTOS branch for an in-person request

| Method | Platform | Delivery | Identity Verification |

| Online Registration | CTOS website | Email/PDF | MyKad, phone, email |

| MyCTOS App | iOS/Android App | In-app/email/PDF | App login, MyKad |

| Touch ‘n Go eWallet | TnG App | In-app/email | TnG ID, MyKad |

| CTOS Branch | Physical Centre | Printed/email | In-person, MyKad |

How to Buy a CTOS Report Through Touch ‘n Go (TnG) eWallet

Buying your CTOS report through Touch ’n Go eWallet is one of the quickest ways to access your credit score and check your loan readiness. The process is fully digital, fast, and convenient, perfect for homebuyers who want an instant overview of their credit standing.

1. Check Your App Version and Wallet Balance

Ensure your TnG eWallet app is up to date and that you have enough balance to pay for the report (usually around RM27.90 for a CTOS Score Report).

2. Log In to Your TnG eWallet Account

Open the app and sign in using your registered mobile number and password.

3. Go to the Financial Services or Search for CTOS

Navigate to “Financial Services” or simply use the search bar to find the CTOS icon. It’s typically listed under Mini Programs or Credit Report services.

4. Select “CTOS Score Report”

Tap on the option to view the price and the details included, such as your CTOS score, CCRIS, and credit alerts.

Confused between CCRIS and CTOS? Get an apparent breakdown in this quick, helpful guide.

5. Confirm Your Purchase and Verify Your Identity

Accept the TnG terms and pay using your wallet balance.

You may be asked to complete identity verification using:

- MyKad number

- IC image upload

- SMS/email OTP

6. Download Your CTOS Report Instantly

Once payment and verification are completed, your report will be generated immediately.

You can:

- View or download the PDF inside the TnG eWallet app

- Access the copy sent to your registered email

7. Check for Free or Discounted CTOS Report Campaigns

TnG eWallet occasionally offers free or discounted CTOS Basic or Score Reports during promo campaigns.

Watch for:

- Push notifications

- Banner ads in the app

- TnG’s promo page

Getting your CTOS report through TnG eWallet is a fast and reliable way to review your credit score before applying for a home loan. With instant access, easy downloads, and occasional discounts, it’s one of the most convenient options for keeping your credit information up to date.

Checking CTOS via MyCTOS App

The MyCTOS app lets you access your full credit report directly from your phone. It’s designed for users who want instant updates on their CTOS score and credit activity.

- Download the MyCTOS app from the Apple App Store or Google Play Store.

- Register or log in with your details, verify your identity (MyKad/IC, phone, email).

- View and download your full CTOS credit report instantly inside the app or have it emailed to you.

- Receive credit alerts and recommendations to boost your score.

Using the MyCTOS app gives you immediate access to your credit report along with real-time alerts, making it easier to track changes and stay prepared before applying for a home loan.

Use our home loan eligibility calculator to find out how much you can qualify for.How Much Does a CTOS Report Cost in 2026?

CTOS reports come in different options depending on the level of detail you need. Whether you’re checking your basic credit profile or monitoring your score before a home loan, these are the typical prices you can expect in 2026.

| Report Type | 2026 Cost (MYR) | Notes |

| MyCTOS Basic Report | Free (2x/year) | Basic credit info only |

| MyCTOS Score Report | RM27.90 / RM27.00 | Full score, CCRIS, alerts |

| SecureID Monitoring | RM9.90/month, RM99/year | Enhanced fraud protection |

Note: Some eWallets may offer free reports during promos; check the TnG campaign page for current offers.

Knowing the cost of each CTOS report helps you choose the right one based on your loan preparation needs.

What Lowers Your CTOS Score (Common 2026 Red Flags)?

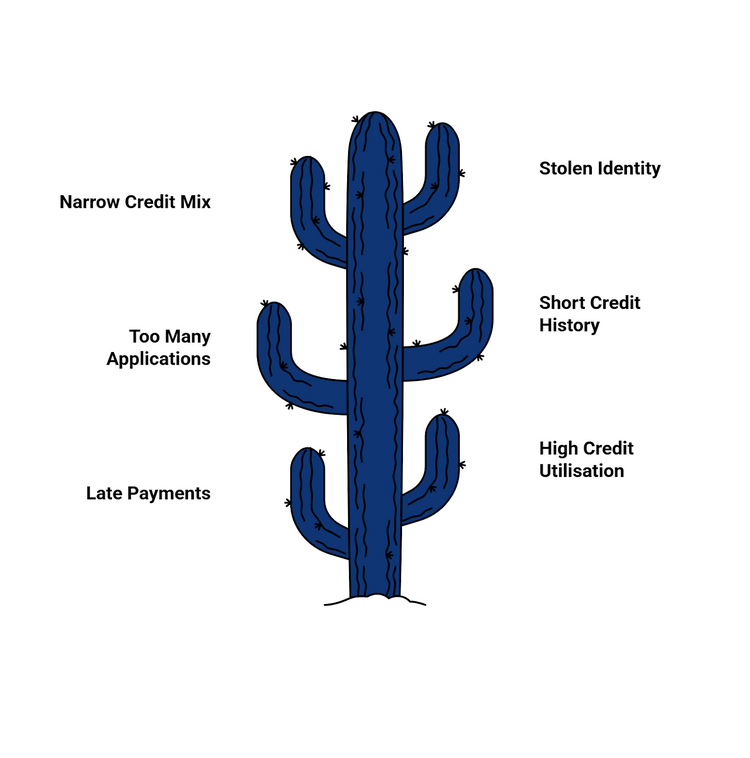

Certain financial behaviours and warning signs will quickly drag down your CTOS score in Malaysia, especially ahead of a home loan application. Knowing these pitfalls helps you fix your credit profile before applying.

Key CTOS Score Red Flags

- Late or Missed Payments

Missing bill, loan, or credit card payments is the biggest reason for a lower score. Even a few late payments, legal actions, or accounts sent to collections can cause a sharp drop.

- High Credit Utilisation

Using 30 to 40% or more of your available credit limits (e.g., maxing out credit cards) signals financial stress. High balances relative to your income are seen as risky by lenders.

- Too Many Credit Applications

Frequently applying for new credit cards or loans within a short period triggers multiple hard inquiries, which can reduce your score and signal desperation to lenders.

- Short or Limited Credit History

Having very few credit accounts, or accounts that are less than two years old, means lenders can’t see enough positive payment behaviour from you.

- Narrow Credit Mix

If you only use one type of credit (like just credit cards, or only a personal loan), your score may be weaker than someone who responsibly manages multiple types (e.g., credit cards plus an auto loan).

- Stolen Identity or Fraudulent Accounts

Any unrecognised loans, credit cards, or purchases showing up on your CTOS report indicate identity theft and should be disputed immediately.

Consistently avoiding these pitfalls is essential to maintaining a healthy CTOS score in 2026, especially when planning a major home purchase.

Use our mortgage loan payments calculator to see your monthly instalments.How to Improve CTOS Score Before Applying for a Home Loan?

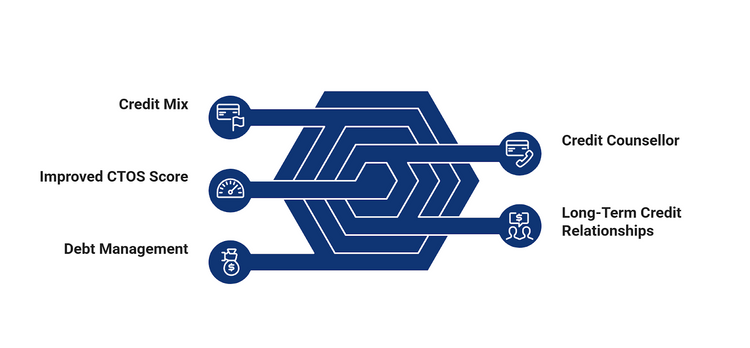

Improving your CTOS score before applying for a home loan involves building consistently good credit habits and tackling potential red flags well ahead of your application. Lenders look for reliable payment behaviour, low outstanding debts, and responsible credit usage.

- Pay All Bills On Time

Set automated reminders or direct debits for utilities, credit cards, and loans. Even one late payment can lower your score, so promptness is key.

- Lower Your Credit Utilisation Ratio

Aim to use less than 30% of your credit limit across cards and lines. Pay down existing balances to signal healthy borrowing and repayment patterns.

- Avoid Unnecessary New Credit Applications

Limit the number of new loans or credit cards you apply for, especially in the six months before your mortgage application, as too many hard checks lower your score.

- Check and Dispute Any Errors

Review your CTOS report for outdated or incorrect entries, and dispute anything inaccurate with CTOS to boost your score.

- Clear Off Small Debts and Settlements

Pay off old, forgotten, or small debts, including overdue telco or utility bills, and get confirmation in writing that your account is settled.

- Maintain a Healthy Mix of Credit Types

Having both credit cards and loans managed responsibly can be favourable, but do not take on debt you don’t need just for “mix” points.

- Build and Maintain Long-Term Credit Relationships

Keeping older accounts open shows a longstanding positive history, while frequently opening and closing accounts can lower your score.

- Seek a Credit Counsellor If Needed

If managing multiple debts overwhelms you, consult with a financial counsellor before your home loan application is in progress.

Consistently following these habits over time can significantly increase your chances of loan approval at better interest rates in Malaysia.

How Long Does It Usually Take to Improve Your Credit Score?

Improving your CTOS score is a gradual process. Most positive changes begin to be reflected in your report within one to three months, but significant improvement can take 6 to 12 months of consistent, responsible habits. Bill payments, debt reduction, and account updates are typically reported monthly so that you can see incremental increases after each update cycle.

- Minor corrections or disputes (e.g., removing inaccurate information) may result in changes within 3 to 14 days.

- Paying off overdue balances or establishing a good payment history is reflected in the next monthly update.

- If rebuilding from a very low score, expect the process to take at least 6 months, and steady financial discipline for at least a year is recommended for the best chance of securing a home loan.

Checking your progress every three to six months helps ensure your efforts are reflected in your CTOS score well before you apply for a home loan.

Final Check Before Submitting Your Home Loan Application

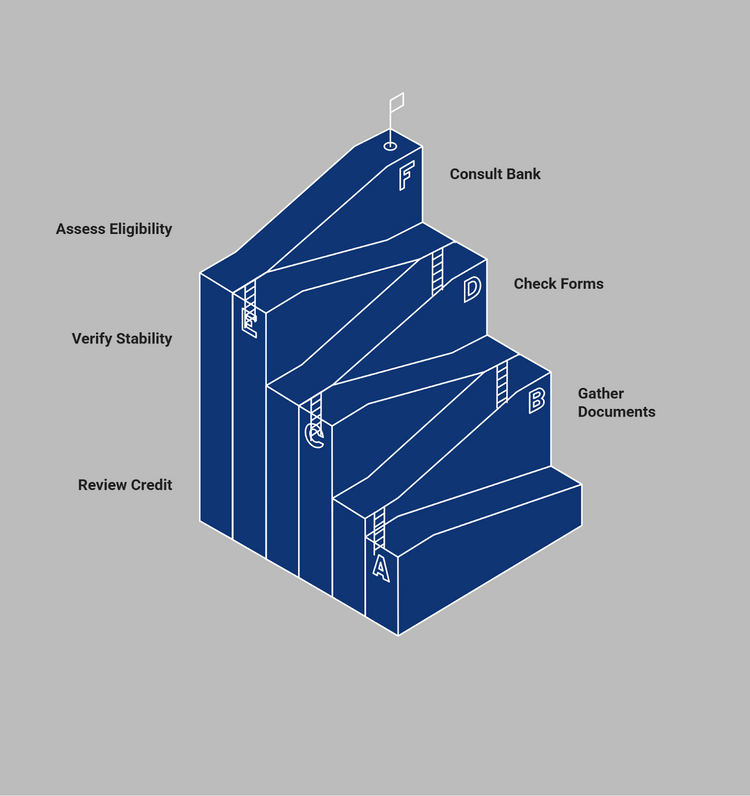

Before submitting your home loan application, complete these final checks to strengthen your approval odds and avoid unnecessary delays:

- Review Your Credit Standing

- Confirm your CTOS score is above the bank’s minimum requirement, ideally 650 or higher.

- Make sure your credit report is free of inaccuracies, recent disputes are resolved, and overdue debts are cleared.

- Gather Required Documents

- Prepare copies of your MyKad/IC (front and back).

- Collect three to six months’ payslips, recent EPF statements, and the last three months’ bank statements.

- Have your latest income tax receipts and stamped property booking or sales forms ready.

- Verify Financial Stability

- Double-check that your monthly debt repayments (including the new home loan) will not overextend your budget.

- Confirm steady income deposits and employment status.

- Check Application Forms

- Ensure all forms are complete, accurate, and signed.

- Attach supporting documents in the order required by the bank.

- Assess Your Loan Eligibility

- Use home loan calculators to confirm the amount you can borrow and the monthly repayment commitment.

- Consult Bank or Agent

- If unsure, request a final review by your banker or mortgage advisor to confirm everything is in order.

Completing these checks greatly improves your chances of timely home loan approval and helps secure the most favourable terms for your new property.

From condos to landed homes, explore what fits you best.What Should You Keep in Mind Before Submitting Your Home Loan Application?

Strengthening your CTOS score and tidying up your financial profile can make a noticeable difference when you’re ready to apply for a home loan. A clean report, organised documents, and steady repayment habits help you present yourself confidently to any lender. With the proper preparation, you place yourself in a stronger position to secure approval and enjoy smoother financing for your new home.

From your first purchase to your next sale, our property guides walk you through every part of the process. Dive in whenever you’re ready.

Follow Malaysia’s newest property launches and uncover fresh opportunities that match your goals.