Are you a first time home buyer? Forget applying for a home loan if you haven’t sorted out these mortgage pitfalls.

Your credit score is typically what banks use to subjectively evaluate the credibility of your financing application, including credit card applications and home loans. However, many banks in Malaysia use their own internal method of evaluating your credit score. This means your chances of getting a loan approved vary depending on which bank you choose to apply for credit. Your credit score can also be used by the bank to determine the interest rate for your loan.

What factors determine your credit score?

In general, credit rating agencies such as RAM Credit information (RAMCI) tabulates a credit score based on an individual’s:

- payment history

- credit mix and loan amounts owed

- length of credit history

- new credit applications in the past 12 months

- legal track record.

The information above, as well as the credit score, will allow financial institutions to determine a borrower’s 3C’s: Character, Capital and Capacity.

CHARACTER: Reflected based on your attitude towards your loan. If you take pride in paying your bills promptly, you will get an A for reliability on your debt repayment. They also take into consideration your personal details such as the length of stay in your current address and the duration of your current employment.

CAPITAL: This shows the number of valuable assets you hold which can be used as collateral, such as property, investment or savings in the event you fail to repay your loan.

CAPACITY: Depicts the income you earn and this reflects your ability to pay off your debt. Thus, you need to make sure that you have sufficient cash flow running.

How can you hurt your credit score?

#1 Being a bad paymaster

Only 55% of Malaysians pay their bills on time, which is 25% below the world average. -Organisation for Economic Co-operation and Development (OECD), 2016-

Being chronically late on your bill payments can have detrimental effects on your credit score. Banks are extremely concerned about your repayment history especially if you have developed a habit of late payments. When another bank sees that you are never on time with your payments, they have the automatic impression that you are going to be late with their payments as well.

The number of negative items on your credit report is important. The more incidents of credit transgressions, the more your score will suffer. And your recent negative financial record will affect your scores more severely compared to a credit record that is several years old. So make an effort to note all your payment due dates on a calendar and work towards meeting those deadlines.

While being early or prompt on your payments for a month won’t improve your credit score immediately, keeping this habit will eventually improve your credit score in the long run.

#2 Defaulting on a loan

On August 15, 2018, it was reported in the Parliament that roughly 64,632 Malaysians aged between 18 to 44 years old have been declared bankrupt over the last 5 years! Their inability to settle car, house and personal loans or for being guarantors for other loan defaulters are the main reasons for this worrying trend, statistics from the Insolvency Department revealed.

Avoid defaulting on your debts if you are struggling to pay your minimum. Contact your lender to organise altering your repayment schedule. if you have more than one credit card, you should identify the total amount of debt and interest rate charged on each card and work towards paying off the card with the highest interest rate first. After you have paid off that card, you can move on to the card with the next highest interest charge and so on so forth. This method applies if you have multiple debt types. Work on your highest first then move downwards from there.

Another way to clear your card balance quickly and with a lower interest rate is through a balance transfer, which is offered by banks. This facility allows a credit card holder to shift debt from an existing credit card with a high annual interest rate to one with a lower interest rate or even a 0% rate over a fixed period.

#3 Sharing poor financial relationships

Sharing financial relationships with others can have a toxic effect. For example, you might share your apartment’s monthly utility payment with your housemate or roommate. Or you may have taken up a loan on behalf of your spouse, relative or friend, or even agreed to be a loan guarantor for them. If they default or delay on the payment, it will reflect badly on your credit score. As a guarantor, the debt will become your responsibility if they don’t pay up, and that will add up to your debt burden, affecting your credit score.

So, be careful when you share bills with others or when you take up loan on behalf of someone else. If possible, keep your finances separate from others including family and this will allow you to control your own credit score.

#4 Having no credit history

If you are proud of the fact that you don’t own a credit card or have never taken up a loan, the shocking truth is, having no credit rating is as bad as having a poor one.

Although you may manage your money well, a lack of credit history could actually be viewed as a negative attribute by the credit rating agencies. The score looks to see if you have a lengthy history of managing your credit obligations. The older your credit report, the more points you will earn. You want the history! You may want to get yourself a credit card, but make sure you don’t splurge on it.

#5 Having rejected credit applications

Taking a loan to repay a loan might sound like a good short-term solution to your mounting debt woes. However, if your credit score is low, applying for more credits will end up being a futile effort because the bank will reject your applications anyway.

What you will be left with is a big pile of debt and a whole list of loan or credit card rejections on your credit score. When you apply for credit you are giving the lender permission to pull your credit scores. Each time this happens, your credit report will reflect what is called an “inquiry.” When a bank rejects an application, it’ll also appear on the report. Therefore, you should really only apply for credit when you need it, and when you are confident that you are going to get it.

#6 Lack of credit diversity

You will earn good points if you have a nice diverse list of different types of accounts in your credit score. This includes mortgages, auto loans, personal loans and credit cards. If your credit score is dominated by one type of debt only, this could negatively affect the number of credit score points that you earn.

So if you have three credit cards, but no other credit facilities in your name, it is time to relook at your credit report.

#7 Maxing out your credit limit

The debt balances that you carry on your credit cards can affect your scores almost as much as whether or not you make your payments on time.

This category calculates the proportion of balances to credit limits on your revolving credit card accounts – also known as revolving utilisation. The higher your revolving utilisation percentage, the fewer credit score points you will earn.

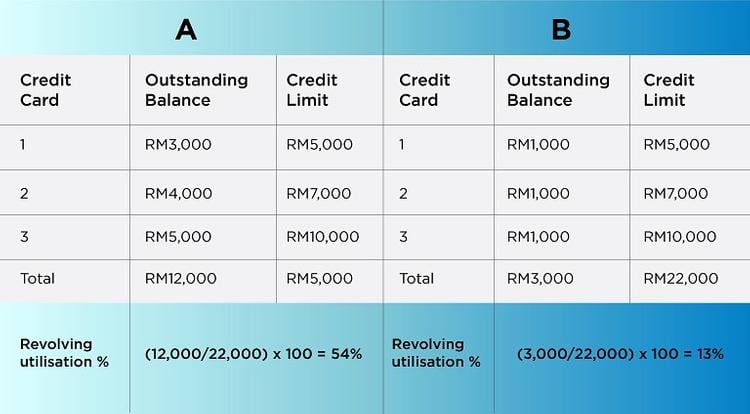

To determine your revolving utilisation, you will need to add up all of your current balances and all of your current credit limits on your open revolving credit accounts. This will give you a total balance and a total credit limit. Divide the total balances by the total credit limit and then multiply that number by 100. This will give you your total revolving utilization percentage.

For example, let’s compare person A’s and person B’s credit record:

Person A with a higher revolving utilisation percentage will have a lower credit score. Keep your credit card debt low with 10% utilisation being the best.

Cancelling credit cards can hurt one’s credit score because this will affect the revolving utilisation percentage. So, it is better to only apply for a card that you need and plan on using.

#8 Having your home foreclosed or car repossessed

Foreclosure is a frightening word for a number of reasons. If you are unable to make your mortgage payments, you will lose your home. Foreclosure will also affect your credit score, which can hurt your chances of qualifying for a new loan in the future.

The same goes if your car has been repossessed because you were delinquent on your auto loan. The mark on your credit report can negatively impact your credit score and can put your repossessed property in jeopardy of being sold or auctioned off. If your car is sold for less than the amount you owe, you will still be responsible for the remaining difference. This debt amount will remain on your credit record until it is paid. Once you pay the debt in full, the repossession status will remain on your credit report for seven years from the date of the original delinquency.

If you are diligent about paying your bills on time and even paid down your credit card balances and other credit scores do’s, you should be on your way to acquiring healthy credit scores. Having a high credit score can set you up for many perks and low-interest loans in the near future. While you can still survive with poor credit score, those extra points will end up saving you money in interest charges over time and can also give you more negotiating power.

Malaysian borrowers can get their credit score for free via iMoney CreditScore, a free credit check tool which provides Malaysians with a three-digit score powered by RAM Credit information (RAMCI).

This article was repurposed from “8 Most Common Reasons Malaysians Get Low Credit Score” on iMoney.com.my | Edited by Reena Kaur Bhatt