Thinking of buying a Malaysia auction property in 2026? This guide breaks down the hidden costs many bidders miss, from unpaid bills and legal fees to renovation, eviction, and financing risks. Learn how the auction process works, when bargains make sense, and how to protect your deposit before you bid.

Buying a Malaysia auction property can be one of the most exciting and cost-effective ways to secure real estate in Malaysia. With thousands of units entering the auction market every month, many homebuyers and investors see auctions as a pathway to lower prices and faster acquisition, especially compared with traditional sub-sale properties. However, the process is not as simple as just placing the highest bid. You are buying the unit strictly as is, and that means everything from outstanding bills to legal complications may fall on your shoulders.

For 2026, the auction landscape in Malaysia has become increasingly digital, competitive, and transparent. Buyers now have access to more data, more online auctions, and clearer administrative rules, yet the risks remain real: late settlements, title complications, unpaid maintenance fees, legal caveats, and stubborn occupants continue to surprise first-time bidders.

This guide provides the most up-to-date understanding of the Malaysia auction property market, what to expect, how to protect yourself, and the hidden expenses you need to budget for before bidding.

Understanding the Malaysia Auction Property Market in 2026

The Malaysia auction property market has grown significantly over the past decade, driven by:

- Higher interest rates in recent years

- Rising cost of living and rising NPLs (non-performing loans)

- Availability of online auction platforms

- Greater transparency in auction listings

- Increased investment interest due to competitive pricing

Major auction platforms and law firms have shifted auctions online, allowing bidders to participate from anywhere in Malaysia. This shift has increased participation, particularly among younger buyers aged 25–40, many of whom are entering the market after being priced out of primary launches.

Meanwhile, demand for Lelong house Malaysia units remains strong, especially among investors seeking below-market property opportunities in urban areas such as Kuala Lumpur, Selangor, Penang, and Johor.

What Is a Property Auction in Malaysia?

A property auction is a sale process conducted when the previous owner defaults on loan repayment. Once the bank forecloses, the property is listed for public auction. Anyone aged 18 and above may bid, provided they can pay the 5–10% deposit before the auction begins.

There are two main categories of auctions. These are:

LACA and Non-LACA Auctions

1. LACA Auction

- The property has no individual or strata title yet

- Transfer is done via assignment

- Typically auctioned by the bank through licensed auctioneers

- Requires 5% deposit

- Settlement period: usually 90 days

2. Non-LACA Auction

- The property has an individual or strata title issued

- An auction conducted by the High Court or the Land Office

- Requires a 10% deposit

- Settlement period: usually 120 days

Many new investors tend to start with LACA units, as reserve prices are usually lower. However, non-LACA auctions often involve fewer administrative risks and delays.

Why Are Properties Auctioned?

Most Malaysia auction property listings arise due to:

- Mortgage loan defaults

- Economic pressures

- Owners unable to service repayments

- Businesses collapsing (commercial property)

- Failure to settle late payments

Understanding the owner’s situation helps buyers estimate the likelihood of outstanding utility bills, unpaid maintenance, or existing tenants.

Discover new and upcoming property launches in MalaysiaHow The Auction Process Works in Malaysia

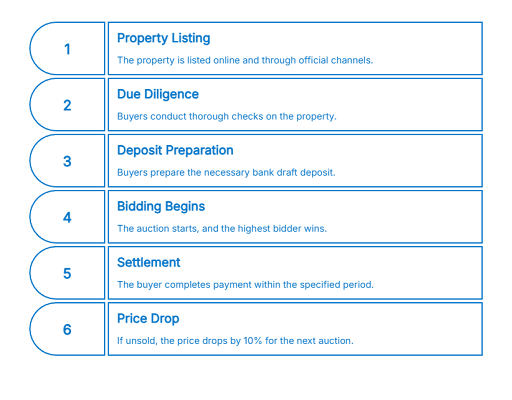

Step 1: Property is Listed for Auction

The auction notice, together with the Proclamation of Sale (POS), is published online and via official channels.

Step 2: Buyer conducts due diligence

This includes:

- Visiting the property in person

- Checking title status

- Verifying unpaid bills

- Reviewing auction terms

Step 3: Bank Draft deposit prepared

Before bidding on a malaysia auction property, you must prepare the required deposit to secure your participation. Ensure the bank draft covers the correct percentage, 5% for LACA or 10% for non-LACA properties, to avoid disqualification.

Step 4: Bidding begins

The auction starts, and the highest bidder at the end wins the property. Bidders should stay within their budget and bid strategically to secure the property.

Step 5: Settlement

The buyer must complete payment within the stated period (90 or 120 days), failing which the deposit may be forfeited.

If a Malaysia auction property is not sold, the price usually drops 10% at the next auction round.

Successful participation in a Malaysia auction property requires careful preparation, research, and financial readiness. By following each step and bidding responsibly, buyers can secure properties with confidence and minimise risks.

Market Trends in 2025

2025 data from Malaysian auction directories and legal firms indicate:

- Residential properties still dominate auction listings

- Condominiums and serviced apartments represent the largest category

- Industrial auctions are rising due to SME business closures

- Digital auctions have made participation easier nationwide

Average auction pricing discounts range between 15-45% below secondary market value, which continues to attract investors looking for opportunities in Lelong house Malaysia listings.

Browse Malaysia’s top property listings and find your dream homeHidden Costs When Buying a Malaysia Auction Property

Many first-time buyers enter auctions expecting bargain prices, only to discover additional costs later. Below are the most common hidden expenses you must budget for.

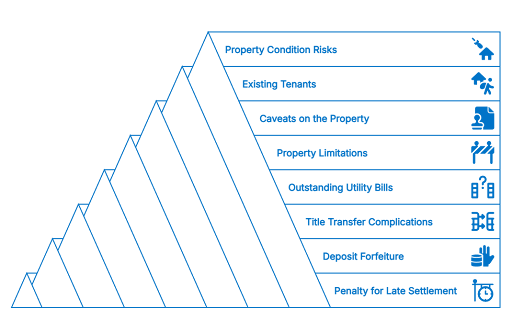

1. Penalty for Late Settlement

For LACA auctions:

- Pay 5% deposit

- Settlement in 90 days

For non-LACA:

- 10% deposit

- Settlement in 120 days

If payment is late, penalties apply, and in some cases, the deposit is forfeited entirely. For this reason, lawyers advise having instant access to cash, overdraft, or ready loan approval before bidding.

Settlement Delays are More Common Now

Financing rejections have increased since banks have tightened risk assessments. For properties with caveats or poor condition, banks may reject loans, forcing the buyer to pay in cash.

2. Deposit Forfeiture

If you fail to do the following, your deposit may be completely lost.

- Failed to secure financing

- Missed the settlement deadline

- Are unable to execute transfer paperwork

Many buyers of Lelong house Malaysia units mistakenly assume they will secure financing easily. Always secure pre-approval first.

3. Title Transfer Complications (Direct vs Double Transfer)

The transfer process depends on the property type:

Direct Transfer

Possible when:

- Developer consents

- Maintenance and sinking fees are paid

- No administrative issues exist

Double Transfer

Needed when:

- The developer refuses consent

- The title is still under master title

- Outstanding fees are present

Double transfer means:

- Higher legal fees

- Two sets of stamp duties

- Longer processing time

Understanding transfer risk is critical before bidding on a malaysia auction property.

4. Outstanding Utility Bills & Maintenance Charges

Auctioned properties may come with overdue:

- Electricity (TNB)

- Water (Air Selangor)

- Sewerage

- Management fees

- Sinking fund

- Quit rent

- Assessment tax

- Insurance

- Late penalties

Check the POS carefully to identify who will bear these charges:

- The bank

- The new purchaser

- Split responsibility

Even if the bank is responsible, the buyer usually has to pay upfront and claim later. Budgeting this cost is critical when analysing a Lelong house Malaysia listing.

5. Property Limitations & Restrictions

These may not always be obvious at first glance. Examples include:

- Bumiputera lot restrictions

- Leasehold tenure with fewer than 20 years remaining

- Land category mismatch (e.g., commercial land used residentially)

- Zoning rules

- Plot ratios

- Height restrictions

Some banks do not finance properties with short leasehold balance remaining, placing additional risk on the bidder.

6. Caveats on the Property

A registered caveat is a legal claim placed to stop property transfer.

Common caveat sources include:

- Co-owners

- Private lenders

- Contractors

- Purchasers with unresolved agreements

Banks often refuse financing until caveats are lifted, meaning buyers must be prepared to settle the Malaysia auction property purchase entirely in cash if necessary.

7. Existing Tenants or Previous Owners

Auction units are sold as is, and possession is rarely vacant. If occupants refuse to leave:

- The buyer must negotiate

- Legal eviction may be required

- The process can take months

Legal fees for eviction commonly range between RM3,000–RM15,000, depending on complexity. This is extremely common with Lelong house Malaysia listings in high-density areas where long-term tenants are present.

8. Property Condition Risks

Auctioned properties cannot be inspected internally before purchase. Many have:

- No power or water

- Long-term vacancy

- Vandalism

- Leaking roofs

- Damaged tiles

- Termite issues

- Broken wiring

Renovation costs for a malaysia auction property can range from minor repainting to full refurbishment. Getting a contractor to estimate external damage before bidding is advisable.

Stay ahead with Malaysia’s latest property auction listingsFinancing Challenges & Bank Approval Risks

Financing an auction purchase is not always straightforward. Banks apply stricter assessments on auction properties, compared to typical sub-sale units, because they are seen as higher-risk assets. Several factors contribute to this:

- Valuation may differ from winning bid price: If the bank’s valuation comes in lower than what the buyer paid, the buyer must top up the shortfall in cash.

- Physical condition concerns: Bad property condition reduces bank confidence in its resale or recovery value.

- Legal complications: Caveats, unpaid maintenance charges, land disputes, or missing documentation can slow the mortgage process.

- Restricted loan disbursement: If a caveat or legal block exists, the bank may hold back the loan until issues are resolved.

If the mortgage application is delayed or rejected, and settlement deadlines are missed, the buyer risks losing their deposit, usually 5% to 10% of the property price.

Advice for buyers in 2026:

- Get a loan pre-qualification: Know your borrowing power before stepping into the auction hall.

- Check valuation in advance: Property agents or valuers can offer an indicative price range.

- Seek legal review before auction day: Lawyers can spot hidden issues in the POS (Proclamation of Sale) and COS (Conditions of Sale).

- Maintain a cash buffer: A financial cushion protects you if valuation is lower than expected or if urgent post-purchase expenses arise.

Legal & Physical Risks Buyers Must Understand

Buying at auction carries risks that buyers must be mentally and financially prepared for.

Risk 1: No Internal Access

Most buyers only view the property externally or rely on auction photos. Without internal inspection, hidden structural damage may go unnoticed until after completion.

Risk 2: Unclear Defects

Problems like leaking pipes, weakening beams, hollow tiles, mould, or faulty wiring might only be discovered after you take possession. Repairs can range from a few thousand to significant renovation budgets.

Risk 3: Legal Claims or Charges

Some properties come with:

- Caveats

- Unpaid developer fees

- Outstanding maintenance charges

- Ongoing disputes

These might affect mortgage approval, delay loan processing, or require legal resolution before the property is fully released.

Buyers should always review legal documents thoroughly or have a lawyer check them to minimise unpleasant surprises.

Eviction & Vacant Possession Process

Winning an auction doesn’t always mean immediate access. Some Malaysia auction property units are still occupied by previous owners, tenants, or even third parties. If they refuse to leave, the buyer may need to begin a formal eviction process.

Steps may include:

- Issuing a written notice requesting the occupant to vacate peacefully.

- Attempting friendly negotiation, which often resolves faster and cheaper.

- Engaging a lawyer if the occupant refuses cooperation.

- Filing for a court-ordered eviction, supported by proof of ownership.

- Bailiff enforcement, where court officers legally remove occupants.

The entire process normally takes two to six months, but could take longer depending on the court’s scheduling, complexity of the case, and whether the occupant challenges the application.

Navigate buying, selling, and investing with property guidesCommon Mistakes Buyers Make When Purchasing Auction Properties

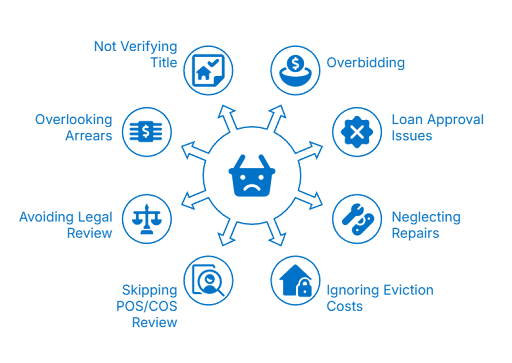

Many first-time purchasers entering the auction market face avoidable problems because they underestimate the risks involved. Common mistakes include:

- Overbidding due to excitement or competition, leading to paying above valuation and straining finances.

- Assuming loan approval is automatic, only to discover valuation shortfalls or legal barriers.

- Failing to budget for repairs, which can significantly increase total cost of ownership.

- Not factoring in eviction costs, legal fees, and time delays if the unit is occupied.

- Ignoring the Proclamation of Sale (POS) and Conditions of Sale (COS), which contain critical terms.

- Skipping legal review, increasing exposure to hidden risks.

- Failing to check outstanding utility or maintenance arrears, which the new owner may be responsible for.

- Not verifying title status, especially for leasehold, master title, or strata status complications.

Avoiding these pitfalls can protect buyers from thousands of ringgit in unexpected expenses.

When Buying a Malaysia Auction Property Makes Sense

Despite the risks, auctions can be extremely rewarding when approached strategically. They are ideal for buyers who:

- Want to secure a property below market value

- Have strong savings and financial buffers

- Understand the auction process well

- Have loan arrangements ready

- Can estimate renovation and repair costs

Investors targeting Lelong house Malaysia properties in good locations may enjoy excellent rental returns after refurbishment. Many auction buyers also build strong capital appreciation once improvements are made and market conditions rise.

Who Should Avoid Auctions?

While auctions offer attractive opportunities, they are not suitable for everyone. Buyers who may struggle in this environment include:

- First-time buyers without savings, who may be financially stretched by unexpected renovation or legal costs.

- Buyers relying 100% on bank financing, since loans are not always guaranteed.

- Individuals who cannot wait for legal processing, mortgage approval, or eviction timelines.

- People uncomfortable with uncertainty, especially regarding internal condition and repair obligations.

- Buyers expecting guaranteed vacant possession, which is not always the case in auctions.

For such groups, a standard sub-sale purchase may be simpler, more predictable, and less stressful.

iProperty Tips for Buying Auction Properties in Malaysia

Buying through auction can be rewarding, but success depends on preparation. These practical tips help buyers minimise risks and make more confident decisions in 2026.

1. Conduct Thorough Due Diligence

Before bidding, review land status, outstanding bills, title conditions, caveats, auction history, and market valuation. This helps you avoid legal or financial surprises later.

2. Always Inspect Externally

Even without internal access, visit the location to assess the visible condition and surroundings. Neighbours can often share useful information such as vacancy length, known issues, and previous occupants.

3. Engage Professionals

A lawyer and valuer can verify documents, spot risks, and confirm fair pricing, offering added protection for buyers unfamiliar with the auction process.

4. Bid With Logic, Not Emotion

Set a maximum price based on valuation and stick to it. Getting carried away in a competitive auction can eliminate any cost advantage.

5. Have Financing Backup

Since loans are not guaranteed, have a cash buffer or credit line ready. This prevents deposit loss if financing falls short or is delayed.

With the right information and financial planning, purchasing at auction becomes far more manageable. A disciplined approach ensures that buyers secure real value, not unexpected stress.

Should You Buy A Malaysia Auction Property?

Buying a Malaysia auction property in 2026 can offer outstanding value, from units priced far below market value to strategic investments in high-demand areas. Yet the risks are real. Auctions place far more responsibility on the buyer than sub-sale purchases, and everything from unpaid maintenance fees to legal caveats will need to be addressed by you.

If you are financially prepared, do your due diligence, and obtain legal and financial advice before bidding, auctions can be a powerful way to build a property portfolio or enter the market at a reduced price. But for those new to the process, consider starting slowly, perhaps observing several auctions before making your first successful bid.

Find upcoming property auctions and get opportunities to bid on residential and commercial units. Explore Auction Listings on iProperty.