Property stamp duty can be one of the biggest hidden costs when buying a home in Malaysia. This guide shows you how to calculate stamp duty Malaysia in 2026 across the SPA, MOT or DOA, and loan agreement, plus the legal fees to budget for. It also covers key Budget 2026 updates, exemptions, self assessment changes, and how to pay without triggering late penalties.

Subscribe to us on Telegram for the latest property insights and updates.

Subscribe to us on Telegram for the latest property insights and updates.

Buying a property in Malaysia involves more than just paying a deposit; one of the most significant and often overlooked costs is property stamp duty. Understanding how to calculate stamp duty Malaysia accurately will help you budget smartly, avoid surprises, and make confident decisions.

In this refreshed guide, we bring you the most up-to-date information (including key Budget 2026 updates), explain how stamp duty and legal fees are calculated, detail exemptions, and walk you through how to pay.

What Is Property Stamp Duty?

Property stamp duty is a tax charged on legal instruments, not directly on the property. In Malaysia, the Inland Revenue Board (LHDN) administers the duty under the Stamp Act 1949.

When you buy a house, several documents are involved, notably your Sale and Purchase Agreement (SPA), the Memorandum of Transfer (MOT) or Deed of Assignment (DOA), and your loan (financing) agreement. Each of these instruments may attract distinct stamp duty charges.

Paying stamp duty ensures these documents are legally valid and enforceable in court. Understanding how much duty applies and the exemptions available helps you plan your finances better and avoid surprises during your property transaction.

How to Calculate Stamp Duty Malaysia: Rates and Examples

Stamp duty is a key part of property transactions, and the amounts vary depending on the type of instrument involved. Understanding how each component contributes to the total cost helps you budget effectively.

Here’s how to calculate stamp duty in Malaysia for the most common property-related instruments.

1. Transfer Duty (MOT / DOA)

Stamp duty for transferring property (via MOT or DOA) in Malaysia uses a tiered (progressive) rate system for Malaysian citizens and permanent residents:

| Property Value (RM) | Rate of Stamp Duty |

| First RM 100,000 | 1 % |

| Next RM 400,000 | 2% |

| Next RM 500,000 | 3% |

| Above RM 1,000,000 | 4% |

These rates reflect the standard ad valorem duty on property transfers.

Example calculation:

Say you purchase a property at RM 750,000. To calculate the property stamp duty:

- First RM 100,000 × 1 % = RM 1,000

- Next RM 400,000 × 2 % = RM 8,000

- Remaining RM 250,000 × 3 % = RM 7,500

Total transfer duty = RM 16,500

2. Loan Agreement Duty

For your loan or financing agreement, stamp duty is 0.5 % of the total loan amount.

Example:

If your home loan is RM 675,000, the stamp duty on the loan is:

0.5 % × RM 675,000 = RM 3,375

3. Sale and Purchase Agreement (SPA)

Every SPA (Sale and Purchase Agreement) requires a fixed stamp duty of RM 10 per copy, regardless of the property price.

When you combine all the following, you arrive at your total property stamp duty cost for the transaction.

- Transfer duty (tiered)

- Loan duty (0.5%)

- SPA duty (RM 10)

By adding together the transfer, loan, and SPA duties, you can determine the total stamp duty payable and plan your property purchase with confidence. Having a clear view of these costs ensures a smoother and more efficient transaction process.

Planning ahead also helps you avoid last-minute complications during your property purchase.

Check your loan eligibility with the home loan eligibility calculator.Fees Other Than Stamp Duty When Buying a House in Malaysia

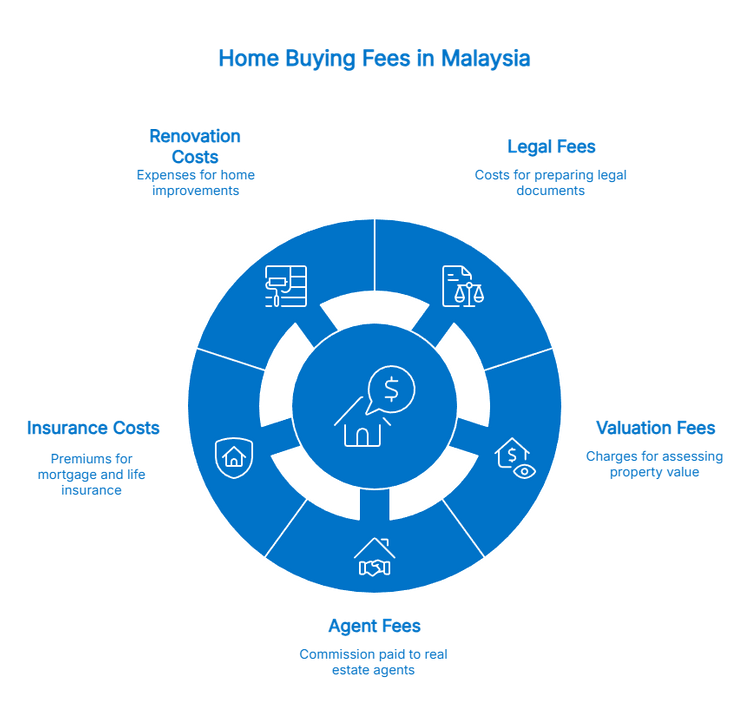

In addition to property stamp duty, there are several other costs you should budget for when purchasing a home. These other fees can add up, and being aware of them helps you form a realistic total cost picture.

1. Legal Fees When Buying a Home

In addition to stamp duty, you need to budget for legal fees, which are charged by your solicitor for preparing the SPA, your loan agreement, and other legal documentation.

On top of basic legal fees, there may be disbursements (search fees, registration, courier, etc.), so always ask your solicitor for a full breakdown.

2. Property Valuation Fees

Lenders usually require a valuation of the property before approving your home loan.

The valuation fee is calculated based on tiers, depending on the property’s value. Some standard valuation-fee scales are:

- First RM 100,000 → 0.25%

- Next up to RM 2 million → 0.20%

- Next RM 7 million → 0.167%

- Next RM 15 million → 0.125%

- Next RM 50 million → 0.10%

- Next RM 200 million → 0.067%

- Next RM 500 million → 0.05%

- Above RM 500 million → 0.04%

3. Property Agent Fees (Brokerage)

If you engage a real estate agent (especially in the secondary market), expect to pay a commission. The maximum is usually 3%, though many agents may charge less, depending on negotiation.

It’s important to clarify and confirm the agent’s commission before you commit, as this ensures your budgeting for the total purchase cost is accurate.

4. Mortgage / Home Insurance

Most banks will require you to take out insurance when you take a home loan. Common options include:

- Mortgage Reducing Term Assurance (MRTA): This covers your loan if something happens to you. The payout decreases as your loan balance declines, so the insurance primarily protects the outstanding loan balance. Premiums usually increase with age.

- Mortgage Level Term Assurance (MLTA): This pays a fixed amount if you pass away, regardless of how much you still owe on your loan. It provides consistent coverage throughout the loan term.

- Term Life Insurance: A flexible insurance plan that provides financial protection for your family. While it’s not tied directly to your loan, it’s important to consider it as part of your overall property costs.

The exact cost depends on your age, loan amount, and chosen insurance plan. Always shop around and factor in this cost early.

5. Renovation and Fit-Out Costs

After the purchase, you may want to renovate, repaint, or upgrade finishes in your new home.

While there’s no fixed legal cost for this, many experts recommend spending no more than 10% of the property’s value on renovations to maintain good financial discipline.

Budgeting for renovation, even roughly, helps prevent cash-flow surprises once you move in.

The Budget 2026 updates bring important changes that every homebuyer and property investor should note. Staying informed on exemptions, higher foreign buyer rates, and the self-assessment regime will help you plan your property transactions effectively and remain compliant.

Browse rental homes across Malaysia.Stamp Duty Exemptions & Reliefs (Budget 2026 Updates)

The Budget 2026 introduced several important changes to stamp duty that homebuyers, especially first-timers, should be aware of. These updates aim to reduce upfront costs and provide clearer guidelines for buyers navigating property transactions in 2026.

1. First-Time Homebuyers (Extension of Exemption)

The full stamp duty exemption on the instrument of transfer and loan agreement for first-time homebuyers purchasing residential properties priced up to RM 500,000 has been extended to 31 December 2027.

This means property stamp duty on those two key documents may be fully waived, significantly reducing your upfront cost.

2. Higher Rate for Foreign Buyers

From 1 January 2026, non-citizen individuals (excluding permanent residents) and foreign companies purchasing residential property will face a flat stamp duty rate of 8% on the instrument of transfer, instead of the current 4%.

This means that calculating stamp duty in Malaysia becomes more expensive for foreign buyers in that category. It’s a major consideration for international investors.

3. Self-Assessment Regime

The Government is shifting to a self-assessment system for stamp duty, effective in phases starting 1 January 2026. Under self-assessment, you (or your appointed agent) will calculate your own stamp duty and submit a return via LHDN’s STAMPS system.

There are new compliance requirements: you’ll need to keep records for seven years, and there are penalties for incorrect or late filing.

4. Employment Contracts

The wage threshold for stamp duty exemption on employment contracts is being raised from RM 300 to RM 3,000 per month, effective 1 January 2026. This is less directly about property, but it is part of the broader stamp duty reforms in Budget 2026.

5. Conversion Incentive for Developers

There is a special tax deduction of 10%, capped at RM 10 million, for eligible expenses incurred when converting commercial buildings into residential units.

While not a direct stamp duty relief, this incentivises property development that could feed into affordable housing, potentially affecting supply and pricing dynamics.

Understanding the various stamp duty exemptions, reliefs, and compliance requirements helps you navigate property transactions with confidence. Proper planning ensures a smoother process and avoids surprises along the way.

The Shift to Self-Assessment for Stamp Duty

One of the most significant reforms in how to calculate stamp duty Malaysia going forward is the transition to a self-assessment regime. Under the old system, LHDN would assess the duty payable after you submit the documents; from 2026, you’ll be responsible for calculating, declaring, and paying the stamp duty yourself.

Here’s what you need to know:

- The rollout will be implemented in phases, giving taxpayers time to understand the new system and adjust their processes gradually.

- You will use the STAMPS (Stamp Assessment and Payment System) portal to calculate, submit, and pay your stamp duty. Records must be kept for seven years, and accuracy is crucial.

- Penalties are more stringent under self-assessment: failure to file returns, incorrect submissions, or failure to retain records may lead to fines of up to RM 10,000.

This reform gives more autonomy to taxpayers, but also demands greater diligence. Being proactive and accurate with your calculations will help you stay compliant and confident throughout the process.

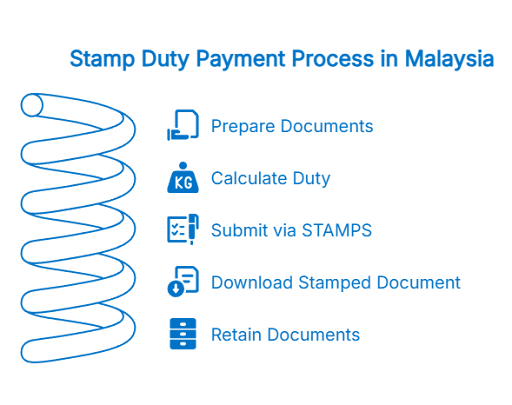

How to Pay Stamp Duty: The Process

Knowing the right steps helps you complete your property stamp duty payment smoothly and correctly. Here’s a step-by-step guide for paying your property stamp duty in Malaysia:

- Prepare your documents

- SPA

- Memorandum of Transfer (MOT) or Deed of Assignment (DOA)

- Loan/financing agreement

- Any other relevant instrument

- Calculate your duty

- Use the tiered rate for transfer duty

- Compute 0.5% on your loan

- Add RM 10 per SPA copy

- If self-assessment applies, calculate via STAMPS

- Submit via STAMPS portal

- Log in to the STAMPS system (LHDN)

- Upload your instruments

- Declare the stamp duty owed

- Pay through the portal or via appointed banks

- Download your stamped document

- Once payment is confirmed, download the e-stamped instrument.

- Keep a copy for your records. It’s your legal proof.

- Retain documents

- Under self-assessment, you must keep all relevant records for seven years.

Paying your stamp duty correctly safeguards your legal rights and helps you stay compliant with LHDN requirements. Keeping thorough records also makes future dealings, such as resale or refinancing, much easier.

Penalties for Late Stamping

If you miss the 30-day deadline to stamp your documents, you may face penalties. The rules (including under Budget 2026 reform) are:

- If you stamp within three months after the due date, the penalty is RM 50 or 10% of the unpaid stamp duty (whichever is higher).

- Beyond three months, the penalty is RM 100 or 20% of the unpaid duty (whichever is higher).

- Under the self-assessment regime, failure to file or incorrect filing can lead to fines up to RM 10,000, plus special penalties for underpaid duty.

It’s important to meet deadlines and comply with the documentation rules to avoid extra costs.

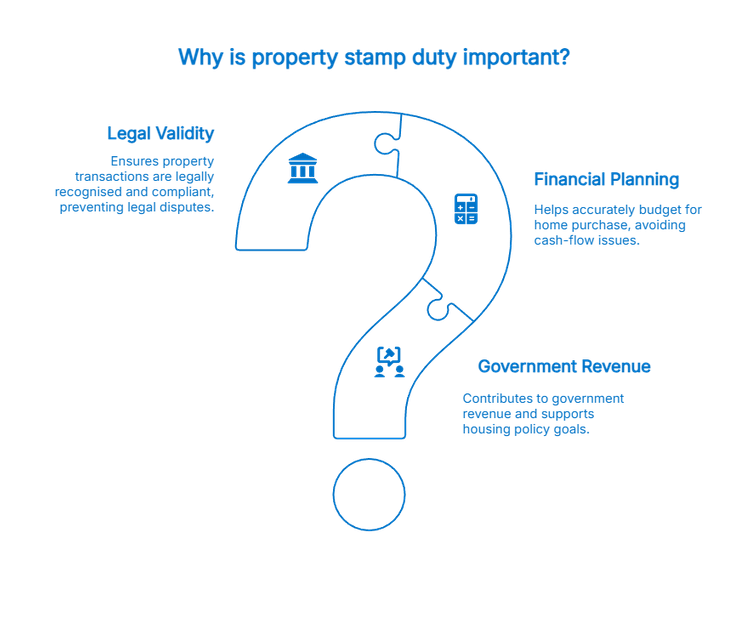

Explore homes for sale across Malaysia.Why Property Stamp Duty Matters?

Understanding property stamp duty is essential for every homebuyer. It not only affects your budget but also ensures your property transactions are legally recognised and compliant.

1. Legal Validity

Stamping your SPA, MOT, and other instruments ensures they are legally recognised. An unstamped agreement may not be legally enforceable in disputes or court proceedings.

2. Financial Planning

Accurately calculating stamp duty in Malaysia helps you budget properly for your home purchase. Underestimating these costs can lead to cash-flow issues.

3. Government Revenue & Housing Policy

Stamp duty is a reliable source of revenue for the Government. The reforms introduced in Budget 2026 reflect broader policy goals: promoting affordable home ownership, discouraging speculative foreign buying, and modernising duty administration.

Being aware of stamp duty rates and recent reforms helps you make informed financial decisions. Proper planning today ensures a smoother, more confident property buying journey.

iProperty Tips for Homebuyers

Navigating property stamp duty in Malaysia can feel overwhelming, but a few simple steps can make the process much smoother. Being informed early helps you save money, avoid penalties, and complete your purchase with confidence.

- Check if you qualify for the first-time buyer exemption: If your property is RM 500,000 or below, you may get full relief on transfer and loan duty until 31 December 2027.

- Use the STAMPS portal: Familiarise yourself now if you’re buying soon, especially with self-assessment coming.

- Ask your solicitor for a full legal-cost breakdown: Disbursements, search fees, and registration costs can add up.

- Keep accurate records: With self-assessment, you must retain your stamped instruments and supporting documents for seven years.

- Be punctual: Stamp within 30 days and avoid the penalties for late stamping.

- Consult professionals: A knowledgeable solicitor or tax adviser can ensure you correctly calculate and pay your property stamp duty.

By following these practical tips, you can stay on top of deadlines, exemptions, and calculations. Getting professional guidance ensures your property journey remains hassle-free and financially sound.

Summary & Key Takeaways

Stamp duty rules can feel technical, but getting familiar with them makes every step of your property transaction smoother. This quick overview brings together the most important points so you can move forward with clarity and confidence.

- Property stamp duty applies to SPA (RM 10), MOT/DOA (tiered rate), and loan agreements (0.5%).

- Legal fees are based on a prescribed scale, plus disbursements.

- Budget 2026 updates: first-time buyer exemption extended to 2027; higher flat duty for foreign non-PR buyers (8% from Jan 2026); self-assessment regime rolling out.

- Self-assessment provides flexibility, but requires careful calculation, record-keeping, and compliance.

- Late stamping penalties can be significant, so make stamping a priority.

- Use LHDN’s STAMPS system, budget proactively, and engage professional help where needed.

Having a solid grasp of how to calculate stamp duty Malaysia, along with the exemptions you qualify for, puts you in a stronger financial position. When you’re ready to move ahead, speaking with a lawyer or mortgage adviser ensures your next property decision is fully informed.

Discover the latest property launches in Malaysia. Stay updated on upcoming residential developments, from high-rise condos to landed homes.