| Classification Of Shopping Centre | Characteristic / Concept | Typical Main Anchors | Net Lettable Area (ft2) |

| Super-regional | Large-scale version of a regional mall. Similar to regional malls but has more variety of fashion apparel, mass merchant, and entertainment/ leisure. Serves as the dominant shopping venue for the region within a certain radius. Catchment’s area/Target drive time market: More than 1 hour Target tourists both local and international Number of anchors/ tenants 3-6 | Supermarkets(s) Department Stores General/Specialize Merchandise Store Cinema/ Entertainment/ Leisure | More than 1,000,000 Example: Mid Valley Megamall Sunway Pyramid |

| Regional | General merchandise and/or fashion-oriented offerings. Focus is on non-discretionary retail and entertainment/leisure. Catchment’s area/Target drive time market: Between 30 minutes to 1.5 hours Number of anchors/ tenants 2-4 | Supermarket(s) Department Store(s) General Merchandise Store (GMS) Cinema/Leisure | 500,001 to 1,000,000 Example: MyTOWN Shopping Centre Sunway Velocity |

| Neighbourhood | General merchandise and/or convenience-oriented. Offerings wider range of apparel and other discretionary retail with a heavy focus on foods & groceries, and other essential products. Catchment’s area/Target drive time market: Less than 30 minutes Number of anchors/ tenants 2-3 | Supermarket(s) General Merchandise Store (GMS) Department Store | 200,001 to 500,000 Example: 1 Mont Kiara Cheras Leisure Mall |

| Community | A form of street retail concept/stand-alone building F&B has been a great draw in malls. A platform of socializing Convenience-oriented Catchment’s area/Target drive time market: Less than 15 minutes Number of anchors/ tenants 1 – 2 | Supermarket/gym/ school/spa | 50,000 to 200,000 Example: Metro Point Kajang Damansara City Mall |

Public discourse is ongoing, debating whether Malaysia is graced with an excess of shopping malls. Within this article, we delve into a comprehensive analysis of the quantity, classifications, performances, and evolving roles of shopping malls in the post-pandemic era.

The Strategic Reasons Developers Favor Building Shopping Malls

Shopping malls are one of the preferred options for many developers. Not only that the mall generate rental rates and capital appreciation that brings new revenue streams, but it is also a commercial component that helps to justify the investment return of mixed-use development while mitigating risks from sole reliance on the residential segment in times of uncertainty.

From the developer’s point of view, it is the catalyst effect of the mall that brings substantial capital investment to an area that had previously attracted little.

By capitalizing the property value with the injection of shopping malls, developers can garner more interest from the public, leading to an overall positive market sentiment that will spur growth further.

This is because the proximity of any proposed developments to a shopping mall, especially those large-scale mega malls, tends to be associated with higher rental yield, property “sell-out,” as well as infrastructure connectivity and social amenities development, which then intensifies the transformation of vicinity areas into high opportunity and hot neighbourhoods with higher economic benefit.

More importantly, like Singapore and Hong Kong, developers in Malaysia have started to sell matured malls into real estate investment trusts (REITs) to raise their profile and recycle their capital while continuing to generate rental income and create asset management opportunities. By contributing their assets to a publicly traded REIT, developers can realize marked-to-market growth in the value of the properties on a real-time basis while maintaining the option to exit their investments through the public markets.

Besides, by contributing assets to a REIT in exchange for shares, developers can create liquidity through the shares, including using various tax-advantageous financing structures that do not require the actual taxable sale of the shares (such as margin loans).

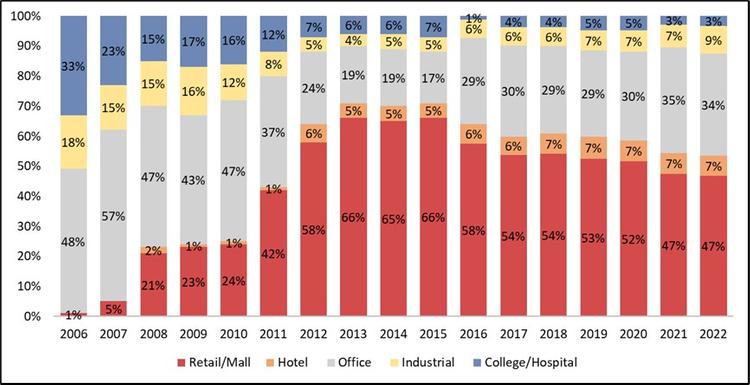

To note, there has been a growing preference for shopping malls as a property allocation strategy by M-REITs since 2006, where the percentage of allocation to retail/mall increased substantially from 1% in 2006 to 66% in 2015.

Though the allocation peaked in 2015 and has gradually declined since then, it is still the biggest contributor compared to other building types, with a percentage of 47% in 2022 (Figure 1).

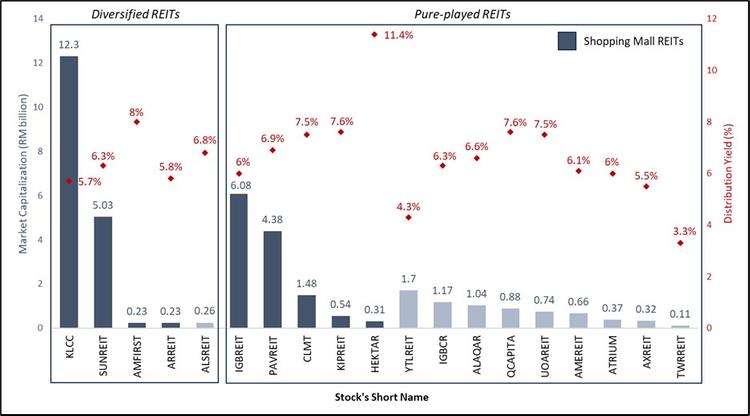

Currently, there are 9 out of 19 listed M-REITs can be considered “shopping mall REITs” as they cover at least one shopping mall in their portfolio (Figure 2). KLCC REIT is amongst the “shopping mall REITs” with the largest market cap (RM12.3 billion), followed by IGB REIT (RM6.08 billion), Sunway REIT (RM5.03 billion), Pavilion REIT (RM4.38 billion), and CAPITALand Malaysia Trust (RM1.48 billion).

These so-called “shopping mall REITs” encompass a total of 30 shopping malls across the country with a total floor space of 16,768,184ft2, which is equivalent to 11.4% of the overall shopping mall floor space (142,351,221ft2) in Malaysia.

Source: Bursa Malaysia

Source: Bursa Malaysia

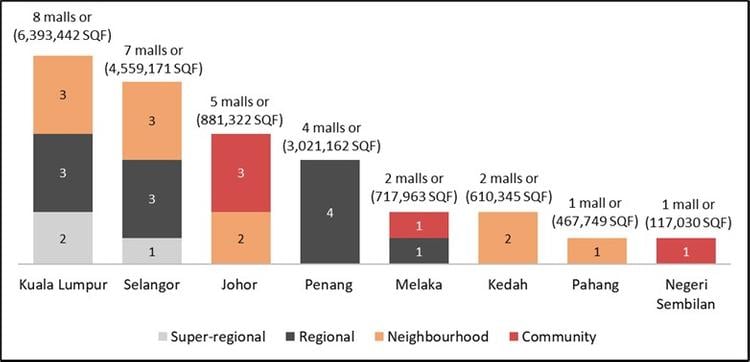

Shopping malls under the coverage of M-REITs are mainly concentrated in the prime real estate markets: Kuala Lumpur (8 shopping malls or 6,393442ft2), Selangor (7 shopping malls or 4,559,171ft2) Penang (4 shopping malls or 3,021,162ft2), and Johor (5 shopping malls or 881,322ft2), encompassing 14,855,097ft2 or 88.6% of the overall net lettable area under “shopping mall REITs” (Figure 3).

By cross-reference with NAPIC’s classification of shopping malls based on net lettable area (Table 1), these shopping malls are found ranging from the scale of community to super-regional: 3 super-regional malls, 11 regional malls, 11 neighbourhood malls, and 5 community malls.

Source: Bursa Malaysia; NAPIC

Commercial Properties to Rent

Table 1: NAPIC’s shopping centre classification

Evolution of Shopping Mall Roles: Understanding Key Transformations for 2024 and Beyond

The role of shopping malls has been evolving and expanding, due to the structural changes in technology (e-commerce), socio-demography (aging population, rise of millennials, dual-income households, and single-person households), and consumer shopping habits.

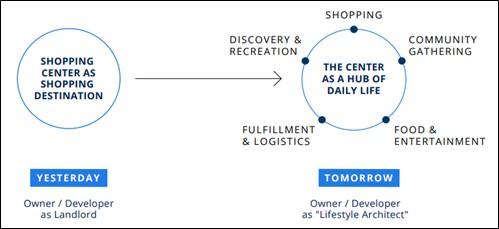

Over the years, the mall’s function has been shifting from a symbol of pure consumerism and go-to shopping hubs for urban/suburban societies into lifestyle centres that provide shopping and entertainment for shoppers who want to shop and play (Figure 4).

Correspondingly, mall owners and operators have been adapting to these changes, either by establishing larger new malls or by extending the existing malls, to provide one-stop convenience that incorporates a diverse set of services to meet commercial, recreational, cultural, educational, and socializing purposes.

Source: Brookfield

Shopping malls in the country have grown larger in size these years, as building a sizeable mall (let’s say more than 800,000ft2) can serve a huge population catchment area while providing enough footfall to support the mall’s tenants.

Up until the beginning of 2020, larger malls were consumers’ favourite destinations in metropolitan areas, as they were recognized as multipurpose spaces that allowed customers to complete procedures, such as paying for services, all in one place, consolidating their role as a comprehensive and convenient option for multiple needs.

A survey conducted by the Malaysia Shopping Malls Association (PPK Malaysia) in 2018 found that 76% of the survey respondents indicated the size of a shopping mall has a direct influence on their choice when deciding on a mall to visit.

Meanwhile, 74% of the survey respondents indicated that the number of stores available in a mall is an important factor for their decision in deciding which mall to visit (Figure 5).

Source: Focus Malaysia

Mall size plays an important role in influencing mall visitation. A “larger mall” has the advantage of facilitating a greater variety of shops and a more pleasant environment to lure shoppers from a wider distance.

In contrast, a “smaller mall” will likely be facing the challenge of securing good quality tenants, since strong retailers prefer to position themselves in a larger mall that can incorporate a wide range of leisure and entertainment options to differentiate itself from others. This, in turn, will affect the ability of a smaller mall to entice more prospective shoppers and eventually becomes a critical survival issue for the smaller mall.

However, in the post-pandemic era, the functional aspect of shopping malls has been further fostered, where malls are no longer just a place to deliver superior customer experiences, but also to centre on “convenience” and “placemaking.”

While larger size “regional” malls that function as all-in-one shopping destinations might continue to stay relevant in terms of offering “convenience” to the population they serve; smaller size “local” malls that meet the needs of the locality are expected to perform better in terms of “placemaking” through mixing shopping with living and working at the human scale to produce a new urban lifestyle experience, thereby leading to the new shopping centre formats that “are central to, and fully integrated with, the communities that surround them.

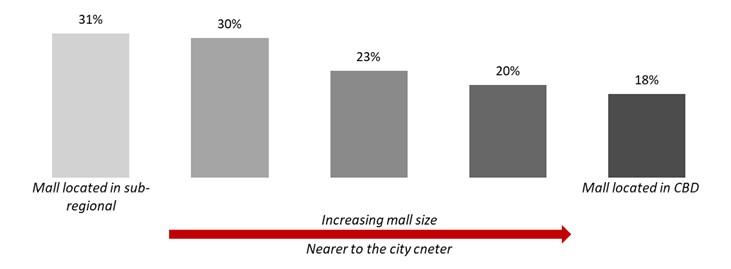

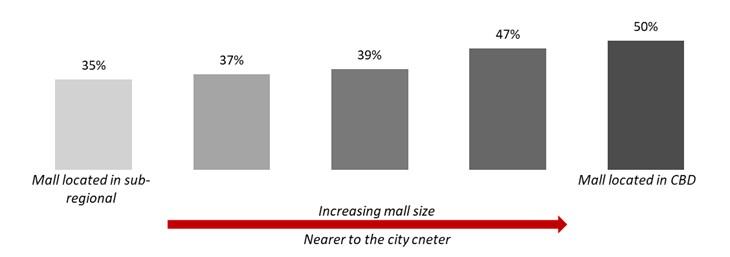

This is evidenced by the study conducted by Cistri to explore mall visitation in Kuala Lumpur Metropolitan, where a majority of the visitors (50%) who visited malls located in the center business district (CBD) – which can be considered as super-regional malls in prime urban area – are residing beyond 10km from the malls; compared to only 18% of the visitors staying within 3km from the malls, which can be considered as local shoppers (Figure 6).

In contrast, 31% of the visitors who visited malls located in the sub-regional areas are local shoppers that reside within 3km from the malls; compared to 35% of the visitors residing beyond 10km from the malls.

This not only supports the argument saying that malls with larger sizes can provide shoppers with great experiences and one-stop conveniences, and hence can draw more footfall from significantly larger catchments, thereby ensuring a better mall performance; but more importantly, it also indicates that a smaller size mall but is unique and is enduring to meet the needs of the locality can do well in the current retail landscape.

% of visits by resident location within 3km (local shoppers)

% of visits by resident location beyond 10km

Figure 6: Percentage of visits by resident location within 3km and beyond 10km from malls with different sizes. Source: Cistris

This signifies the process of mall polarization – a phenomenon that occurred way before the pandemic and is becoming more obvious after the pandemic – where consumers either prefer to shop in a larger mall with a wider range of stores and services; or in smaller, attractive, focused, and convenient mall.

Both the smallest size “Community” mall (with the size of 50,000ft2 – 200,000ft2) and the largest size “Super-regional” mall (with the size of more than 1 million ft2) are deemed to serve different purposes and face different challenges.

However, these “extreme size” shopping malls will ultimately become successful schemes in the current retail landscape, as they are closely aligned with the needs and aspirations of today’s consumers. The ‘raison d’être’ of larger size “regional” malls will still be a destination, one-stop shopping, a full day out experience, infrequent but big basket shops, while smaller size “local” malls will emphasize on higher frequency lower ticker shopping trips, which are far more locality and convenience-led.

What concerning the most is malls that fall between the two stools of “Community” and “Super-regional” malls – which is the “Neighbourhood” (with the size of 200,000ft2 – 500,000ft2) and “Regional” (with the size of 500,000ft2 – 1 million ft2) malls – as these types of “intermediate size” shopping malls will need a strong differentiating element, or even to reposition themselves to reach out to the niche or underserved market. In other words, they will need to navigate between experience-driven “Super-regional” malls and hyperlocal “Community” retail, to stay relevant in the changing retail landscape.

READ: 15 Properties to Rent Close to New Shopping Malls in KL

Analyzing the Supply and Demand Dynamics of Malls in Malaysia

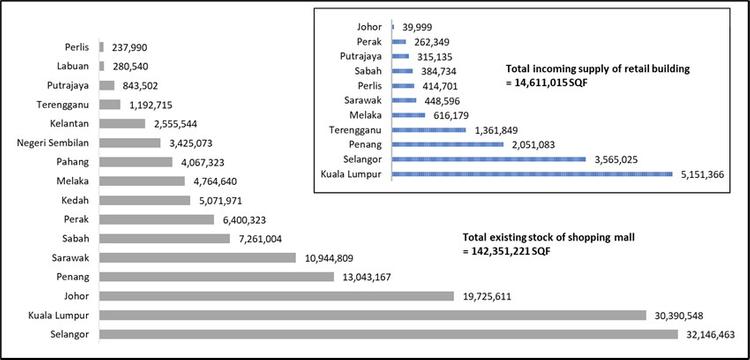

With so many existing malls and incoming retail spaces, especially around the Klang Valley region (Figure 7); new malls could be located too near to the existing ones, thereby leading to the overlapping of malls’ catchment area.

For example, the Pavilion Damansara Heights Mall, which is a newly opened regional mall with a net lettable area (NLA) of 529,353ft2, is located next to the Damansara City Mall, a community mall with an NLA of 190,005ft2.

Source: NAPIC

While both malls do have the advantage of being located along the Sungai Buloh-Kajang MRT line, and thus, can draw shoppers from areas along this train line; the primary catchment for both malls is mainly occupants from offices and residences in the surrounding luxury precinct.

Given the new-to-market F&B, premium fashion, and accessories brands that feature more prominently in the Pavilion Damansara Heights Mall, the newly opened full-fledged regional mall should be able to pull in a wider group of customers. This can pose challenges to the Damansara City Mall (a community mall), as larger malls will put pressure on smaller malls to compete for both the tenants and shoppers, owing to the high floor space per capita – a ratio of square footage inventory of shopping mall to population – within the same area.

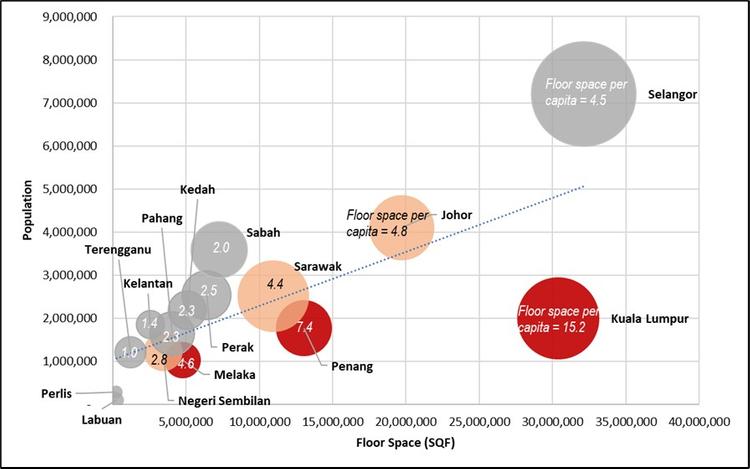

By studying the floor space per capita at the state level, which is a proxy indication of the health of supply and demand in each location, one can find that malls are mainly concentrated in areas with higher populations and gross domestic product (GDP) (Figure 8).

With a relatively higher ratio of floor space per capita, states like Kuala Lumpur (15.2), Penang (7.4), and Melaka (4.6) can be considered as an oversupplied market; while states like Johor (4.8), Sarawak (4.4), and Negeri Sembilan (2.8) are near to saturation. Selangor (4.5) is not yet an oversupplied market, due mainly to its relatively larger GDP and higher population. The remaining states are considered as manageable market.

Source: DOSM;NAPIC

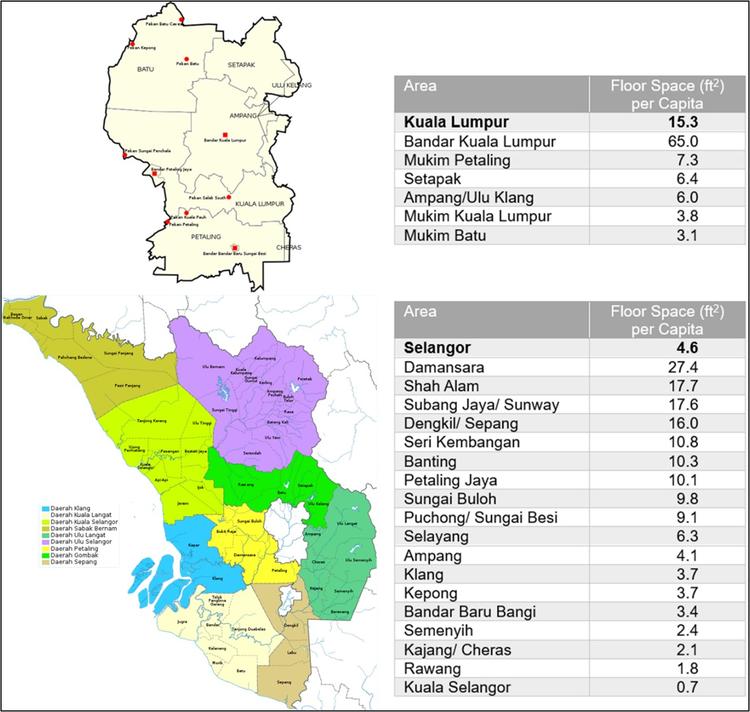

Further zooming down to the city level, especially for the highly concentrated and urbanized Klang Valley region, one can find that there are areas with either oversupplied or underserved markets in the locality (Figure 9).

In Kuala Lumpur, for example, the highest floor space per capita is found in the center business district (CBD) (Bandar Kuala Lumpur) (65.0), followed by Mukim Petaling (7.3), Setapak (6.4), Ampang/Ulu Klang (6.0), etc. While in Selangor, the highest floor space per capita is found in Damansara (27.4), followed by Shah Alam (17.7), Subang Jaya/Sunway (17.6), Dengkil/Sepang (16.0), Seri Kembangan (10.8), Banting (10.3) etc.

Since the ratio of floor space per capita is an indication of the supply and demand balance in a particular area, understanding how this ratio plays out its role will help mall owners and operators devise mall strategies to stay afloat.

For example, should a developer want to establish a new mall in Kajang (with a floor space to capita of 2.1), the size of the mall, together with its footfall drawing capability, must be taken into account seriously, as it requires different types of malls and business strategy than establishing a mall in Damansara (with a floor space to capita of 27.4).

(Note: The floor space per capita ratio in the city level is based on 2020 statistics)

Source: DOSM;NAPIC

READ MORE: Top 10 Most Searched Areas by Homebuyers in Malaysia in 2023

Optimizing Mall Performance: The Impact of Size on Shopping Centers

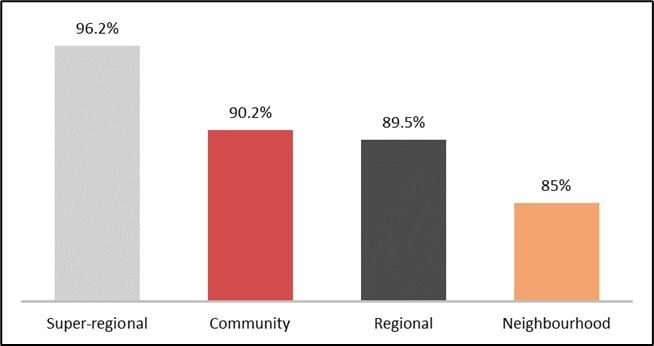

A higher mall occupancy rate is an indication of greater mall visitation or crowd magnetism. A glance at the occupancy rate of different types of malls derived from 30 shopping malls under the M-REITs coverage found that the mall with the highest average occupancy rate is the super-regional mall (96.2%), followed by the community mall (90.2%), the regional mall (89.5%), and the neighbourhood mall (85%) (Figure 10).

This shows that a larger mall may have the advantage in physical size to serve a wider catchment area, but under certain circumstances or in certain locations, a smaller local mall could be performing more outstanding than the larger one, especially in areas with a lower ratio of floor space per capita.

Source: Bursa Malaysia

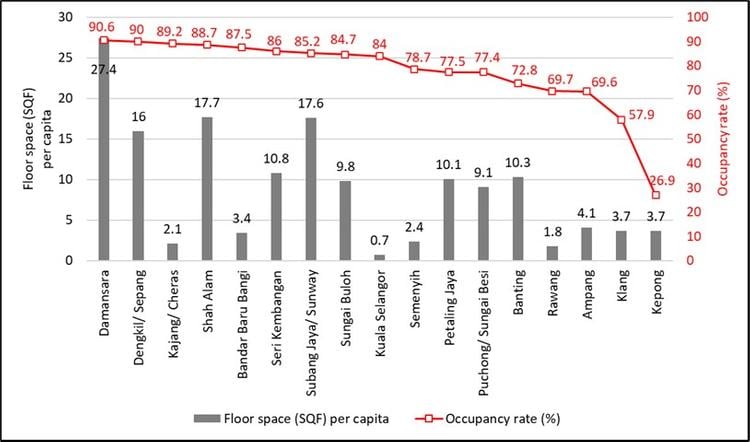

This is evidenced when cross-referencing the locality floor space per capita with the mall average occupancy rate (Figure 11), where a higher mall occupancy rate is either found in areas with higher floor space per capita (i.e. Damansara, Dengkil/Sepang, Shah Alam, and Subang Jaya/Sunway), or in areas with lower Floor space per capita (i.e. Kajang/Cheras, Bandar Baru Bangi, and Kuala Selangor).

This aligns with the phenomenon of mall polarization, suggesting that success hinges on having the correct combination of factors: the right mall design, foot traffic, location, and a strategic alignment with the target market in terms of branding and positioning. Only malls that effectively navigate these elements will thrive and excel in any market conditions. Conversely, those lacking the ability to compete, grappling with diminishing market shares, low foot traffic, and declining retailer turnover, will inevitably find themselves compelled to shut down.

What is the average rental of malls in Malaysia?

Source: NAPIC

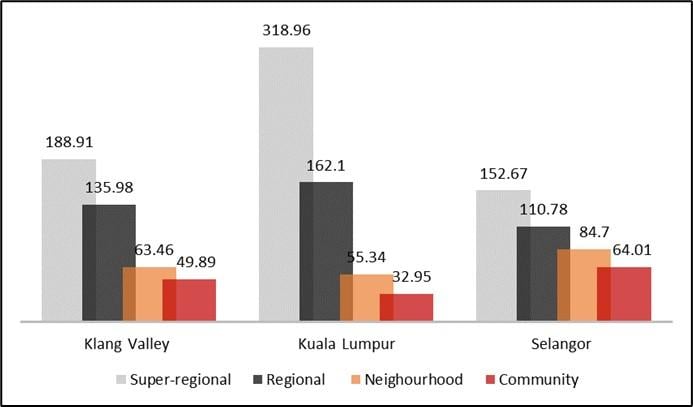

On the mall rental front, as shown in Figure 12, rentals for larger malls outpace smaller ones; where the average rental for a super-regional mall is the highest (RM188.91/m2), followed by the regional mall (RM135.98/m2), neighbourhood mall (RM63.46/m2), and community mall (RM49.89/m2). Similar trends are also observed in Kuala Lumpur and Selangor, where the average rentals are declining with the reduced mall size.

While it is unsurprising that rentals for those super-regional and regional malls located in Kuala Lumpur are higher than the one located in Selangor; rentals for smaller malls in Selangor – both the neighbourhood and community malls – are, in fact, higher than their counterpart located in Kuala Lumpur. For example, the average rental for a community mall in Selangor is RM64.01/m2, while its counterpart in Kuala Lumpur is RM32.95/m2.

Source: NAPIC

How can we improve mall construction for better functionality and appeal?

Again, building the right mall that matches the right target market requires not only the right positioning concept (mall size) but also subject to the right place (location). Different types of malls, in terms of size and location, will result in different income profiles, and will further diverge even more as different types of malls have repositioned to remain relevant. The ability to properly segment, identify, and understand individual customers and their desires for convenience and differentiated experiences will lead to the divergence between winners and losers in the retail sector.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.