| Effective Lending Rate = Reference Rate + Spread (Borrowing cost of your loan) (E.g. Base Rate, SBR) (Includes credit and liquidity risk premiums, operating costs, profit margins) |

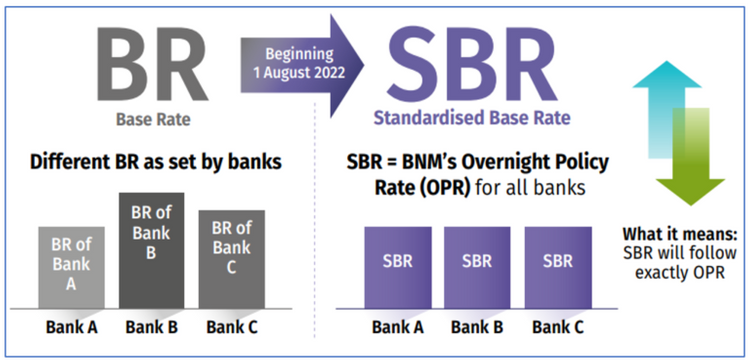

According to Bank Negara Malaysia (BNM), a new Standardised Base Rate (SBR) will replace the Base Rate (BR) for new retail floating-rate loans in Malaysia. The revised Reference Rate Framework will be effective on 1 August 2022.

Subscribe to us on Telegram for the latest property insights and updates.

Subscribe to us on Telegram for the latest property insights and updates.

As the Standardised Base Rate (SBR) will be linked solely to the Overnight Policy Rate (OPR), changes to the SBR will only occur following changes in the OPR, which is determined by the Monetary Policy Committee of BNM. This new framework is aimed at helping consumers make more informed decisions as it offers greater transparency and compatibility of loans across all banks in Malaysia.

What is the Standardised Base Rate (SBR)?

The Standardised Base Rate was introduced by Malaysia’s central bank as a common reference rate for all financial institutions, including banks, for their new retail floating-rate loans. This will be the new framework or system for pricing floating-rate loans, including housing loans and personal loans.

Why did BNM introduce the Standardised Base Rate?

Under the new framework, the Standardised Base Rate will be used as the common reference rate for all banks for their new retail floating-rate loans. In comparison, under the Base Rate (BR) framework, lenders utilized various methods to set their respective base rates, and this has made it more difficult for consumers to compare the loan products.

The Standardised Base Rate will be pegged solely to the Overnight Policy Rate (OPR). Hence, there will only be changes in your loan’s interest rate if the central bank increases or slashes the OPR. Other elements of loan pricing like a borrower’s credit profile, liquidity risk premium, bank’s operating costs, profit margin and other costs will continue to be reflected in the spread added on top of the Standardised Base Rate.

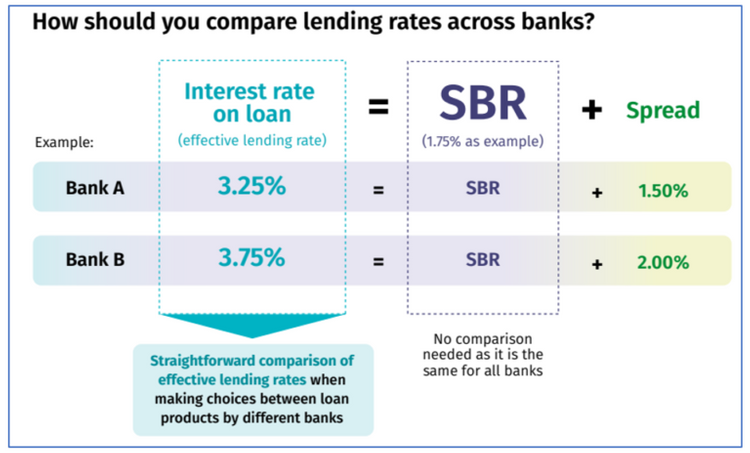

Your housing loan’s interest rate (also known as the effective lending rate) is made up of a reference rate and a spread. The reference rate is the interest rate that is used as a benchmark whereas a spread refers to the bank’s operating costs and profit margin, as well as a premium based on how much risk the bank is taking by lending to you.

What is an effective lending rate (ELR)?

A lending rate is an all-in rate that affects the repayment amount.

What is a reference rate?

The Standardised Base Rate is an example of a reference rate. It determines the changes in borrowers’ repayments on floating rate loans throughout the tenure.

What is a spread?

A spread includes credit and liquidy risk premiums, operating costs, and profit margin. A spread is usually different across banks and individuals as it is based on your own credit risk and each bank’s risk appetite. It is also generally fixed throughout the lifetime of the loan.

The formula above shows how a bank determines the effective lending rate of your housing loan and this is how banks will quote their lending rates using the SBR moving forward.

Difference between Standardised Base Rate and Base Rate (BR)

The SBR is meant to replace the Base Rate (BR), a reference rate that was introduced in 2015. The BR itself was introduced to replace another reference rate, the Base Lending Rate (BLR). Under the existing reference rate framework, each bank is allowed to set its BR. This means that every bank has a different BR. When the new framework kicks in, however, the banks will all use a single rate – the SBR. The SBR will be the same for each bank.

With the Standardised Base Rate (SBR), the methodology for determining the interest rate of a housing loan will be uniform across all banks operating in Malaysia. While the base rate will be the same, the difference will lie in the spread, with some financial institutions adding a lower or higher spread.

For more information on the Base Rate and BLR, read: What to know about Base Rate (BR), Base Lending Rate (BLR) and Spread Rate when selecting a housing loan?

SEE WHAT OTHERS ARE READING:

How much home loan can I get from my salary in Malaysia?

How much home loan can I get from my salary in Malaysia?

How to calculate Debt Service Ratio (DSR) & how does it affect my loan approval?

How to calculate Debt Service Ratio (DSR) & how does it affect my loan approval?

How does the Standardised Base Rate benefit you?

The BR is internally determined by banks, based on the benchmark cost of funds and the Statutory Reserve Requirement (SRR). Unless you work in the financial industry, you may be unfamiliar with this term. It does not help either that each bank has a different methodology for calculating its BR.

Therefore, the move to the standard base rate makes lending rates more transparent. By setting a single reference rate that is driven solely by the OPR, it helps consumers like us understand the changes in our loan repayments when interest rates change. With a single reference rate, you can also compare lending rates across banks without accounting for different BRs. This makes it easy to see which banks are charging lower spreads.

What loans does the Standardised Base Rate apply to?

The SBR only applies to new floating-rate loans and financing for individuals beginning 1 August 2022.

What are floating-rate loans?

Floating-rate loans refer to loans where the interest rate can change throughout the loan’s tenure. It applies to housing loans and personal loans but is generally not applicable to fixed-rate loans such as hire purchase loans (car loans) and SME or corporate loans.

How does the SBR affect your existing and future loans?

Here is how the new reference rate framework will affect your loans:

Existing loans

Loans approved before 1 August 2022 will still be priced against the BR or BLR until the loan is fully repaid by the borrower. From 1 August 2022, the reference rates (BR or BLR) move in tandem with the OPR. This means that if the OPR increases or decreases by 0.50%, the BR or BLR will increase or decrease by 0.50% too.

Future loans

New loans approved from 1 August 2022 onwards will be priced against the SBR. The SBR also moves in tandem with the OPR.

Will the SBR affect effective lending rates?

BNM states that the new framework will not really affect the lending rates of retail floating-rate loans for existing borrowers. Some borrowers might question if they are being charged more under the SBR as the spread is larger. If the Effective Lending Rate is the same, then borrowers are not being charged more.

BNM also added that new borrowers would be unaffected by this revision, as effective lending rates for new borrowers would continue to be competitively determined and influenced by multiple factors, including a financial institution’s assessment of a borrower’s credit risk profile, funding conditions and business strategies. Nevertheless, on the outlook, SBR seems to be ideal for making comparing lending rates easier and more transparent.

NOTE: Borrowers who have any queries or complaints can either contact their respective banks’ complaint units or get in touch with BNMLINK via email or phone at 1-300-88-5465.

What are the latest lending rates by banks in Malaysia?

Amidst the rising interest rate environment, it has become more important for would-be home buyers to be selective when it comes to choosing the right housing loan package that would suit their financial appetite in the long term. A single-digit difference in interest rate can save you thousands of Ringgit, given that you will be repaying the mortgage for several decades. To help you shop around, we have compiled the latest BR, BLR & Effective Lending Rates for banks in Malaysia.

TOP ARTICLES JUST FOR YOU:

? Commercial vs residential: Can I convert commercial title to residential title?

? A beginner’s guide to Islamic home financing in Malaysia

?️ A complete guide: Takaful vs conventional insurance in Malaysia

This article was repurposed from BNM Announces New Standardised Base Rate: What Does It Mean For Your Loans? first published by imoney.my and is written by Jen-Li Lim.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.