How can you determine the best time to buy a house in order to get the best capital gains? This article looks at historical evidence in Malaysia and finds that if you buy house a year after an economic downturn, you will get the best return on investment.

For many buying a live-in property, one of the considerations is whether the property will achieve good capital gains in the future. There are of course many factors that may affect capital gains from location to economic conditions.

However, I would argue that historically in Malaysia, the year that the property is bought makes significant difference on capital gains. To illustrate this, I analysed capital gains over a few 20-year periods for several house types across 4 major states in Malaysia.

The results showed that the best capital gains were from buying property in 1999, a year after the 1998 economic recession. If history repeats itself, 2021 will be a good time to buy property in Malaysia.

Why is it a good idea to buy a house in 2021?

2021 is a favourable time to invest in property for the following reasons:

- Lower interest rates for your housing loan.

- Attractive stamp duty exemptions under the HOC 2020 (Home Ownership Campaign) and for first-time home buyers as announced under Budget 2021.

- You may get a higher loan % relative to the price of the house.

All of the above will affect the potential return on investment. Capital gains are the difference between the market value of the property in the future and the current purchase price. While you do not know the future market value of the property, you have a choice of buying at the “best” time.

The best time is when there is an oversupply situation or when people have a wait-and-see attitude about buying properties. This generally coincides with an economic downturn. This article will show that in Malaysia:

- Historically, the best capital gains are from buying property when the economy recovers from negative gross domestic product (GDP) growth.

- The capital gains from buying at the correct time far outweigh the gains from closing costs and lower interest rates.

Capital gains from property investment in Malaysia

To derive capital gains from investing in real estate, I compared the Malaysian Housing Price Index (HPI) over various 20 years periods. (Refer to Note 1). I used the HPI for the relevant region for 4 types of houses – Terrace, Semi-D, Detached and High-Rise. For example, I derived capital gains for the National Terrace house for a particular 20-year period as follows:

- 1990 to 2009 – Based on the difference between the National Terrace HPI in 2009 and 1990.

- 1991 to 2010 – Based on the difference between the National Terrace HPI in 2010 and 1991.

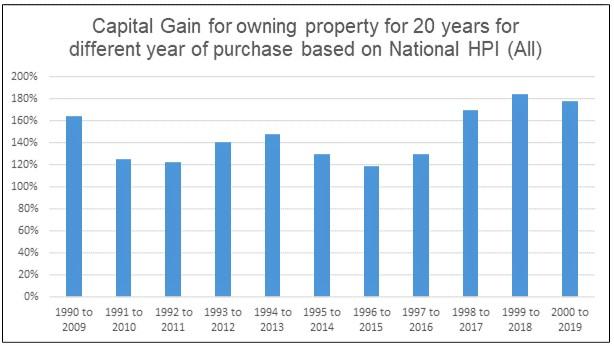

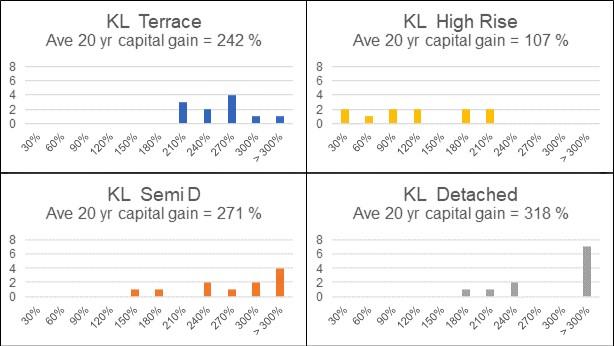

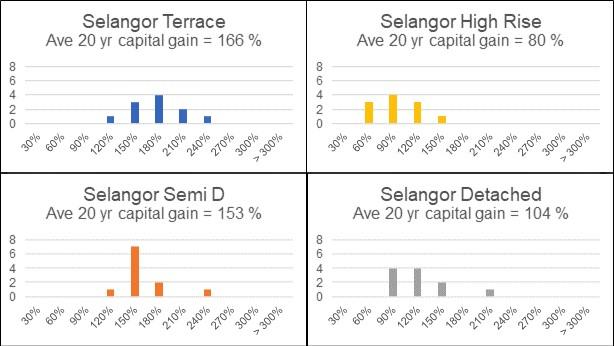

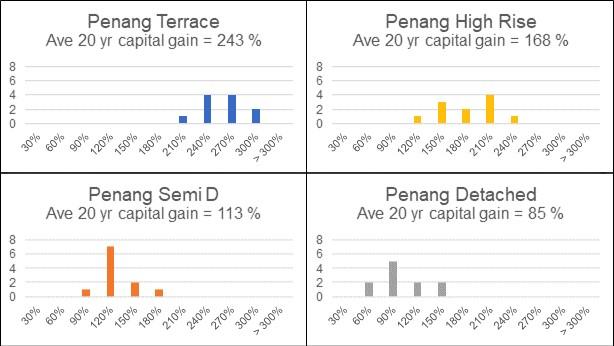

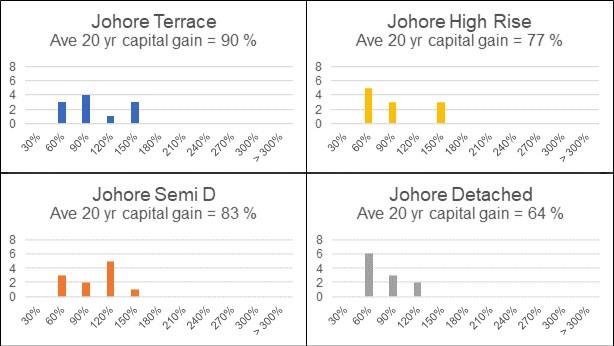

Based on the data available, there were 11 rolling 20-year periods from 1990 to 2019. I computed the capital gains for each of the 20-year periods and compared them as shown in Chart 2.

The analysis showed that the best capital gains for these 11 periods came from buying property in 1999. The results were quite consistent for the various types of properties. Of course, the analysis excluded closing costs such as brokerage fees, legal fees and other statutory charges.

Although the focus of the article is on when to buy property for the best capital gains, you should note that even in a worst-case scenario (ie buying a National High-Rise in 1990) there were still some capital gains.

What happened during the last economic downturn?

What was so special about 1999?

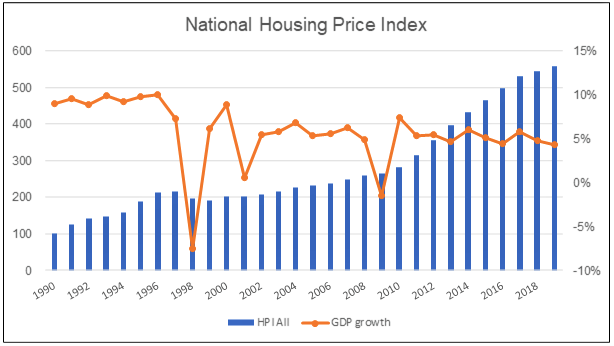

It was a year after the Asian Financial Crisis in 1997-1998 that began in Thailand and spread to the rest of its neighbouring countries. In July 1997, the Malaysian Ringgit was traded by speculators. The overnight rate jumped from under 8% to over 40%. This led to rating downgrades and a general sell-off in stock and currency markets.

By the end of 1997, the KLSE had lost more than 50% of its value, falling from above 1,200 to under 600 points, and the Ringgit had lost 50% of its value. The then Prime Minister Tun Dr Mahathir Mohamad imposed strict capital controls and introduced a 3.80 peg against the U.S. Dollar.

In 1998, the output of the real economy declined and plunged the country into its first recession for many years. The country’s GDP plunged to -7.6 % in 1998.

Not surprisingly, the 1998 National HPI contracted by 9.4 % compared to 1997 levels.

Relationship between Capital Gains and Malaysia’s GDP Growth

Comparing Charts 2 and 3, I concluded that the best capital gains were from buying property a year after negative GDP growth. For the period of 1990 to 2009, it meant buying property in 1999.

The next negative GDP period was in 2009 due to the US sub-prime crisis. However, there is not enough data from 2010 to 2029 for analysis.

You should not be surprised by these findings on 1999:

- During an economic downturn, prices of assets including properties are likely to decline.

- If you believe that prices will recover and go up even higher, then buying at market lows will boost capital gains.

I would argue that 2021 could be another “best” time to buy properties as this is after a negative growth year. In August 2020, Bank Negara Malaysia (BNM) revised its official GDP growth forecast for 2020 to between -3.5% and -5.5%. This was due to changes in world growth forecasts and the duration of the movement control order (MCO) to manage the COVIC-19 pandemic.

BNM is forecasting a growth range of between 5.5% and 8% for 2021. This is due to the improvements in external conditions and a gradual normalisation of economic activities. My point is that the extent of the negative GDP growth is not so critical. What is important is that 2021 is a recovery year. If history repeats itself, 2021 could be the best time to buy properties from a capital gains perspective.

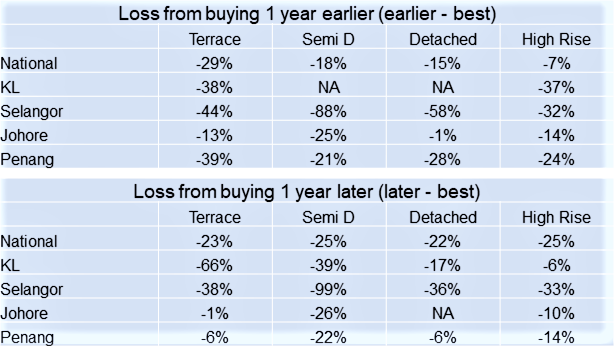

What happens if you buy a house a year earlier or a year later?

Not everyone is able to buy property during the best years. The table below shows the potential losses if you buy a year earlier or later. The losses can be quite significant depending on the type of properties or the location.

If you are in Kuala Lumpur or Selangor, missing out on the best year can make a significant difference to the capital gains.

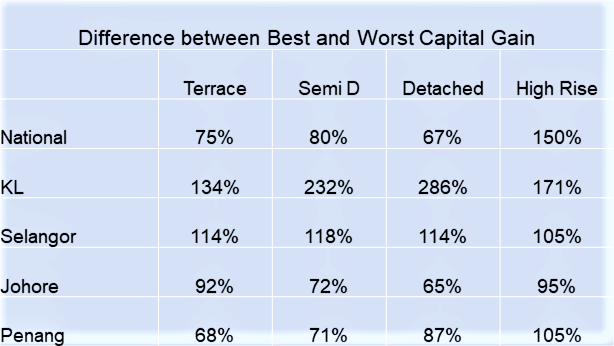

If are able to select the best time to buy property compared to the worst time, would there be significant differences in capital gains?

The results are actually significant. You could make at least 2/3 more if you buy at the best time compared to buying at the worst time. Of course, the differences vary by regions and property types as shown in the table and chart below:

• The best results are almost a fourfold gain – from Detached houses in Kuala Lumpur.

• The lowest is 2/3 gain – from Detached houses in Johor.

The largest impact is from timing the property purchase

The financial gains from buying a live-in property depend on the following:

- Capital gains resulting from the difference between the market price in the future and purchase price.

- The financing costs incurred in funding the house purchase.

- The various closing costs (eg real estate agent fees, legal fees, stamp duty fee).

- Property taxes.

I would argue that the capital gains due to timing are so large that it overshadows savings on the closing costs associated with buying property such as stamp duty and legal fees. At the same time, as taxes are generally based on a percentage of the gains, it would not be as significant as the capital gains.

Of course, the major cost generally associated with buying property is the interest charged on your home loan. Over a 20-year period, the amount of interest paid can be substantial and would vary depending on the interest rates.

Bank interest rates tend to vary with economic situations, as seen below:

You can take advantage of this to have a variable rate mortgage. But even if you have a fixed interest rate loan, you can refinance your property to take advantage of any significant decline in the interest rate. The differences in the interest charges are not as significant as the capital gains.

- This is because interest rates in Malaysia over the past 20 years have mostly ranged from about 4 % to 6 %.

- In contrast, if you consider the average capital gains of about 147 % over 20 years, this is equal to slightly above 7 % per annum.

The conclusion is that the capital gains far outweigh the gains from other/closing costs. Since the capital gains are affected by the timing of the purchase, house buyers should focus on the timing of their purchases, especially if the goal is to maximise financial returns.

MORE: Latest from BNM: Base Rate, BLR & Effective Lending Rates for banks in Malaysia

Property Investment tips in 2021

This article is not about where to invest to get the best return on investment. However, if you ignore timing and consider the average capital gains for each of the 11 rolling 20-year periods, the best capital gains would be in the following locations:

- For Terrace houses, it would either be in Kuala Lumpur or Penang.

- For Semi-D and/or Detached houses, it would be in Kuala Lumpur.

- For High-Rises, it would be in Penang.

- The worst place to invest for capital gains is Johor.

Property or Stocks?

In my earlier article “Properties vs stocks: Which is a better investment in Malaysia?” I have shown that for 20 years investment horizon:

“If you are in Selangor, Johor, and Penang and want to hold for 20 years or less, you get a better return on investment from the stock market. The only exception is holding a Terrace house in Penang for 20 years.”

However, this conclusion looks only at the average return. If you consider another dimension and look at the distribution of the returns, you will find that the stock market has a wider range of outcomes.

The chart below shows the frequency distribution of returns from investing in the Bursa Malaysia KL Composite Index (KLCI). It is based on various 20-year holding periods. You will notice that for the 11 periods, the returns ranged from the 30 % – 60 % category to the 210 % – 240 % category. We can conclude that the return on investment is volatile.

TOP ARTICLES FOR HOME BUYERS:

? What you should know about HOC 2020 (Home Ownership Campaign)?

? What are the government incentives for home buyers in 2021?

?Which were the 10 most searched areas to buy/rent in 2020?

Pulling it altogether

- Based on a 20- years ownership period, the best time to buy a house is the year after an economic downturn. For some types of properties in certain regions, the best time could be during an economic downturn.

- If you are not able to buy during the best year and buy had bought the property one year earlier or later, the “losses” can be quite significant depending on the type of properties or the location.

- If you want to more than break even taking into account your housing loan, picking the best time to buy is important.

- From an investment perspective, properties in Johor had the lowest capital gains compared to those in Kuala Lumpur, Selangor, and Penang.

If history repeats itself, from the perspective of maximizing capital gains:

• 2021 would be a good time to buy properties.

• You would probably be OK if you had bought your property in 2020.

Limitations

- The analysis looks at capital gains based on the Malaysian HPI from 1990 to 2019. Unfortunately, the data was only available to cover 11 rolling 20-year periods which covered only the 1998 economic downturn. I was not able to cover the 2010 economic downturn.

- At the same time, around 2013 to 2019 the HPI increased at a rate that was about double from 2002 to 2008, as seen in Chart 3. I am not sure whether this phenomenon will continue in the future.

- There is also not enough data to see whether the conclusion holds if a longer ownership period was considered (eg 30 years instead of 20 years).

*This article was repurposed from “Determining the best time to buy your house”, first published on i4value.asia

If you enjoyed this guide, read this next: How to buy a subsale property in Malaysia in 7 steps