Monthly instalment for an RM600,000 home loan at 4.5% interest rate per annum | |

| LOAN TENURE | MONTHLY INSTALMENT (RM) |

| 10 years | RM6,218 |

| 15 years | RM4,590 |

| 20 years | RM3,796 |

| 25 years | RM3,335 |

| 30 years | RM3,040 |

| 35 years | RM2,840 |

*This article was updated on 12 October 2020.

When you have something as large as your mortgage loan looming over you, you may be tempted to pay it off as soon as you can. But this may not always the best financial decision – here’s what you should know before you settle your home loan early.

An early payoff is a great idea if you want to save on interest payments – the faster you pay off your home loan, the less interest you pay down the road. Just paying it off a few years earlier could give you tens of thousands of ringgit in cash savings!

How to pay my off mortgage early?

Here are a few ways you can pay off your home loan early:

1. Refinancing to a shorter-term home loan

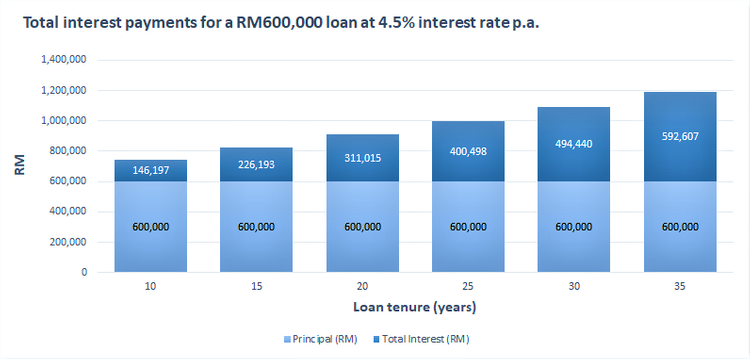

Refinancing means replacing your existing home loan with a new home loan from either the same bank or a different one. When you refinance, you can switch to another home financing product with a shorter loan tenure. By switching to a shorter term mortgage loan, you can save a lot of money in terms of interest rates. Here’s how different loan tenures affect your mortgage loan’s interest payments:

A shorter loan tenure means paying substantially less interest. The difference between a 20-year tenure and a 25-year tenure in the scenario above, for example, is almost RM100,000 in interest payments!

But before you decide to go for a shorter tenure on your mortgage loan, you will need to make sure that you can pay off the higher monthly payments that come with it:

READ: What is home loan refinancing & how can I do it?

2. Make small, additional payments every year

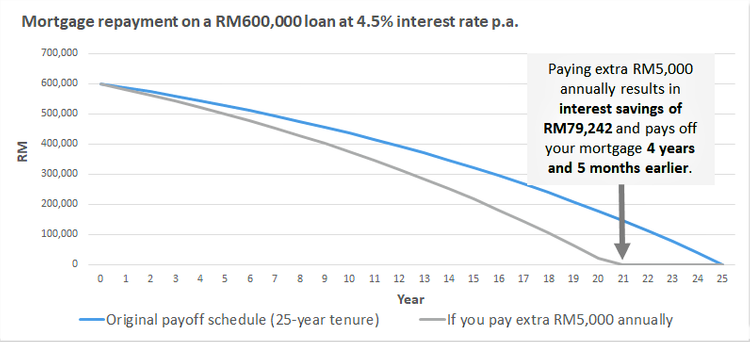

What if you put away extra money – such as your bonus – every year to pay down your mortgage loan? Over time, you could be saving thousands of ringgit in interest and pay off your mortgage loan years earlier. Here is an example of how much you can save if you made an extra RM5,000 cash payment every year on your home financing product:

3. Making a large capital repayment towards the principal

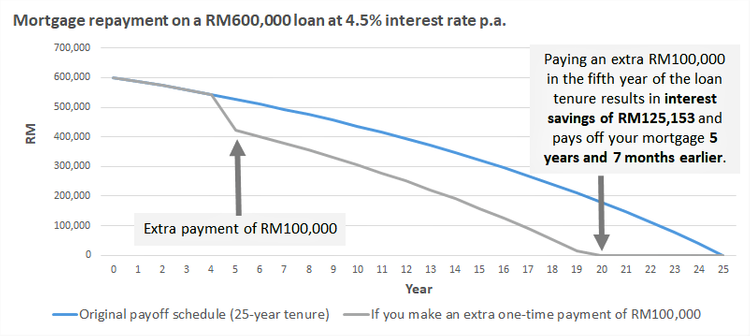

If you’ve amassed a large amount of savings and would like to put it towards paying off your mortgage, you’d be paying a lot less interest down the line. For example, here’s how much less interest you might be paying if you made a one-time payment of RM100,000 in the fifth year of your home loan tenure:

Is it smart to pay off your home mortgage loan early?

Although having to pay less interest on your home loan is a compelling prospect, there are a few situations in which you should refrain from doing so:

1. If it depletes your savings

You should not rush to pay off your home loan if that means using up all your savings. Your home is an illiquid asset – which means it’s hard to turn it into cash when you need it. If you’ve used all your cash on your home, it could be hard to deal with unexpected financial challenges, such as a sudden loss of income, a medical emergency, or a challenging period such as during the COVID-19 pandemic.

Instead of using all your savings to pay off your home loan, make sure you have an emergency fund in place. Your emergency fund should cover about six months of your living expenses.

2. If you have higher-interest debts

Mortgage loan interest rates are comparatively lower than other types of loans such as personal loans or car loans. If you have other debts with higher interest rates – such as a credit card debt – it makes more sense to pay them off first.

MORE: BNM reduces OPR to 1.75% due to Coronavirus – How will it affect your home loan?

3. If your bank imposes penalties for prepayment

Your bank may impose a penalty if you settle your mortgage before your “lock-in period” (usually the first 3 to 5 years of your home loan tenure) expires. This penalty is typically 2% to 5% of your outstanding loan amount.

Even if you’ve passed your lock-in period, you can still be penalised for making a prepayment or clearing your mortgage loan payment in full, depending on your bank.

Before making an advance payment, check with your bank if these penalties apply, and if they can be waived. Otherwise, these penalties can negate any interest savings gained by an early payoff.

There are however different types of loans in the market, including the basic loan which this article covers, semi flexi loan and full flexi loan. If you opt to take a full flexi loan, you will be able to benefit from lower interest rates on the days where you have additional cash.

4. If you want to retain mortgage insurance

If you’re covered under mortgage insurance, your loan will be paid off in the event of death, terminal illness or disability. In such situations, you’ll be able to use the extra money to support yourself or your beneficiaries.

However, if you’ve used your savings to pay off your home loan, not only will your savings be tied up in your home, you will also lose the financial buffer provided by your mortgage insurance.

Is it better to pay off my home loan or invest the money elsewhere?

Finally, you would want to consider the trade-off between paying off your mortgage loan and using that money to invest instead.

Home loan interest rates in Malaysia can range from 4.2% to 5% per annum. If you can invest your money at a rate of return that outpaces your mortgage interest rates, then it might be worth doing that instead.

For example, let’s look at these scenarios:

1. Shorter loan tenure vs Investing

20-year home loan tenure |

25-year home loan tenure + investing |

| Home loan: RM600,000 Tenure: 20 years Interest rate: 4.5% Monthly Payment: RM3,796 The shorter, 20-year loan tenure results in RM311,095 in interest payments – that’s an interest savings of RM89,403 compared to a 25-year tenure. | Home loan: RM600,000 Tenure: 25 years Interest rate: 4.5% Monthly Payment: RM3,335 The extra five years results in total interest payments of RM400,498 – that’s an increase of RM89,403. However, you pay RM461 a month less. If you invested this amount every month for 25 years with an average of 6% per year, it would grow to RM319,470 (RM138,300 in deposits and RM181,170 in interest). |

2. Making small annual payments vs investing

Paying off your home loan |

Investing RM5,000 a year |

| Home loan: RM600,000 Tenure: 25 years Interest rate: 4.5%If you contribute an extra RM5,000 a year to paying off your home loan, you could save RM79,242 in interest and pay off your loan four years and five months earlier. | Instead of paying off your home loan, you invest RM5,000 every year for 20 years. If your investments return an average of 6% every year, it would grow to RM183,928 (RM100,000 in deposits and RM83,928 in interest). |

3. Making a large payment vs investing

Paying off your home loan |

Investing a RM100,000 lump sum |

| Home loan: RM600,000 Tenure: 25 years Interest rate: 4.5% If you contribute RM100,000 to pay off your home loan in the fifth year, you could save RM125,153 in interest and pay off your loan five years and seven months earlier. | Instead of paying off your home loan, you invest RM100,000. If your investments return an average of 6% every year for 20 years, it would grow to RM320,714. |

In the scenarios above, investing makes more financial sense. Instead of paying off your home loan earlier, you could make bigger contributions to your Employees Provident Fund (EPF), put your money in Amanah Saham Bumiputera (ASB) or even invest via a robo-advisor.

However, the investing scenarios above assume that you have a long time to grow your portfolio, and that you are comfortable putting your cash in moderate to high-risk investments.

But if these circumstances don’t apply to you – say, if you are nearing retirement – you may need to reduce your exposure to risky investments. This could mean a smaller rate of return. If your returns do not outpace the interest rate you are paying on your mortgage, then you should consider paying off your mortgage instead of investing.

You may need to make use of mortgage repayment calculators and compound interest calculators to help you determine if the trade-off between paying off your home loan and investing is worth it.

CHECK OUT: Home Ownership Campaign (HOC) extended until 2021! Here’s what homebuyers should know

So, should you pay off your home loan early?

In short, an early pay off could save you a lot in interest payments. But paying off your mortgage loan early could also be a bad idea if it:

- Depletes your savings

- If you can use your money to settle high-interest debts

- If you can invest in a way that outpaces your mortgage’s interest rate

Of course, if being debt-free is important to you, you can still choose to pay off the home loan early even if it doesn’t make the best financial sense – just as long as you’re aware of and can live with the financial consequences. After all, having no home loan, no debt and fewer monthly payments can feel liberating and you can’t put a price on peace of mind.

This article was repurposed from “Is Paying Off Your Home Loan Early A Good Idea?” on iMoney.com.my | Edited by Reena Kaur Bhatt

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.