|

Valuation – 3 approaches | |

| Basis | House purchase analogy |

| Relative valuation | Your house is worth the same as your neighbour’s house |

| Asset-based valuation | Your house is worth the cost to buy the land and build it |

| Earning based valuation | Your house is worth the rent you get over its life |

There is an analogy between valuing a house and valuing a property company that is listed on Bursa Malaysia. This article looks at the nuances when valuing property companies through such a lens.

There are two main ways to engage with the stock market:

- The first is to focus on market prices. You spend your time figuring out how the market will react to events and news about the economy, business, or even politics.

- The other is to invest based on fundamentals. Here you focus on the business prospects. You look for opportunities to buy when the market price is less than the value of the business as determined by its fundamentals.

If you follow the former, you treat the stock market as a place to buy and sell pieces of paper. You don’t worry about the business. This is a sentiment-driven approach and your success depends on your ability to read crowd behaviour. Most likely you are a stock trader rather than a buy-and-hold investor.

But if you follow the latter, one of the key requirements is to be able to assess the value of the stocks. This is what many fundamental investors refer to as estimating the “intrinsic value”.

So how do you determine the intrinsic value of a stock? I will illustrate this by using the property valuation of a house as an analogy. I will also refer to sample valuations of several Bursa Malaysia property companies to illustrate these concepts. But this is not meant to be any recommendation on the stocks.

Market prices and business values

We have established that for a fundamental investor, market prices are also important. You are buying and selling based on how the market prices compare to the intrinsic values. Both price and value are the two sides of the investing coin.

Understanding the difference between price and value is an important part of investing. While you can get the stock price for listed companies on Bursa Malaysia, there is no quoted intrinsic value. In practice, you have to estimate the intrinsic value yourself.

Different investors will have different estimates of the intrinsic value of a company. Compare this with the stock price – while the stock price may fluctuate at any one point, there is one price representing the thinking of the crowd at that time. The market price represents the perceived value by the crowd and is not the intrinsic value. Market price changes frequently whereas intrinsic value does not change daily.

To the fundamental investor, there is a difference between the stock price and the intrinsic value. Most of the time, the stock price is determined by the supply and demand for the stocks. In the short term, this is driven mostly by market sentiments. If you are a fundamental investor, you believe that in the long term, the stock price will reflect the business prospects. If the market price is less than the intrinsic value, you take this as a buying opportunity and vice versa.

Thus, intrinsic value is not given by any stock quotations. You have to estimate it. This is the realm of valuation.

What are the 3 methods of valuation?

For a fundamental investor, to determine whether a stock is cheap – you compare its market price with its intrinsic value. Your reference point is the intrinsic value. How do you value companies? This is not a treatise on the mathematics of valuation. Rather I am going to introduce 3 simple approaches to valuing companies:

- Relative valuation.

- Asset-based valuation.

- Earnings-based valuation.

The simple way to understand stock valuation is to use the analogy of how houses are valued. Refer to the chart below. Details are presented in the subsequent sections.

When you are buying or selling a house, all 3 approaches make sense. This is not the case when valuing companies. When it comes to determining the fundamental value of a company, you are looking at business prospects. Many would rely on either asset-based or earnings-based methods as they reflect the business prospects.

But from a business prospect’s angle, the relative valuation may not always show a realistic picture. Imagine a situation where the prospects for a sector/industry are bad – a company may do well relative to the sector. Relative valuation will show that this is a good stock when in reality the prospects are dim. But many people use relative valuation because it seemed so easy to value companies with this approach.

TOP ARTICLES JUST FOR YOU

10 properties in Bukit Chagar near the RTS project

10 properties in Bukit Chagar near the RTS project

➡️ Can developers compel homebuyers to waive the LAD?

Method 1: Relative valuation

If you are thinking of selling your house, one way to get the value of the property is to look for the comparable value of houses in the neighbourhood. You might scale it to account for some of the differences in these properties, such as the extent of home renovations, number of bedrooms, etc.

For example, if your neighbour’s house is worth $X on 2,000 sq ft of land, you may conclude that since your house is on 3,000 sq ft of land, it is worth $1.5 X.

When it comes to valuing property companies/stocks, there are several common bases for comparison such as Earnings, Book Value or Revenue. And a common way to account for the different sizes of the companies is to consider the metrics on a per-share basis.

Once you have the Earnings or Book Value per share, you then compare it with its market price. You then have for example the Price to Earnings ratio commonly known as the PE multiple. You can also have the Price to Book Value ratio or the PBV multiple. You can imagine having various types of multiples such as the Price to Sales or Price to Cash Flow.

How do you then determine whether the property stock is cheap or expensive?

There are 2 common approaches:

- Compare it with the historical multiples of the company.

- Compare it with the multiples of comparable companies.

Chart 1 is an example of the former. It shows the PBV multiple for SP Setia stock in the past 10 years. Looking at it, you can see the multiple has declined from a high of 2 times to currently 0.5 times. You could then conclude that if it was trading at 2 times Book Value in the past, the current price is undervalued.

Chart 2 illustrates the other approach. It compared the PBV multiple of SP Setia with several other property companies on Bursa Malaysia. Based on this comparison, you can then judge whether it is undervalued relative to the panel.

For example, on 26 April 2021, the SP Setia stock was trading at a PBV of 0.36. The multiples for the other companies ranged between 0.39 to 0.62. On this basis, you would conclude that SP Setia was “cheap” then.

With the relative valuation approach, you have two questions to consider:

- Which is the relevant multiple to use?

- How do you select comparable companies?

Acquirers’ multiple: Why it is superior

I seldom use relative valuation in my analysis. But if I had to do so, my preference is for the Acquirer’s Multiple. Developed by Tobias E.Carlisle, the Acquirer’s Multiple compares the total cost of a business (if you were to buy it outright) to its operating income or enterprise value divided by operating earnings, or simply put as EV / EBITDA where:

- EV = Enterprise Value = Market Capitalization + Minority Interests + Debt – Cash.

- EBITDA = Earnings Before Interest, Taxes, and Depreciation & Amortization.

Carlisle did a study where he compared the returns with several valuation multiples. He found that the Acquirer’s Multiple had the most success identifying undervalued stocks. Wall Street’s favourite metric – Price-to-forward Earnings estimate – was by far the worst-performing ratio.

Chart 3 shows the past 12 years’ Acquirer’s Multiple for the SP Setia stock.

According to Carlisle, an Acquirer’s Multiple of less than 6 would denote an undervalued stock.

Industry Profile

When determining the value of your house, you would compare it with similar houses within your neighbourhood. It is unlikely that you would compare it with houses in another state or another country.

But when it comes to valuing property companies, the choice of comparable companies may not be so clear. In the first place, companies have different business models and structures. Looking at size within the same sector may not be sufficient. Professor Damodaran has suggested that comparable companies be based on the cash flows and risk profile rather than sectors. This is in contrast to the common approach of having companies of the same industry or size.

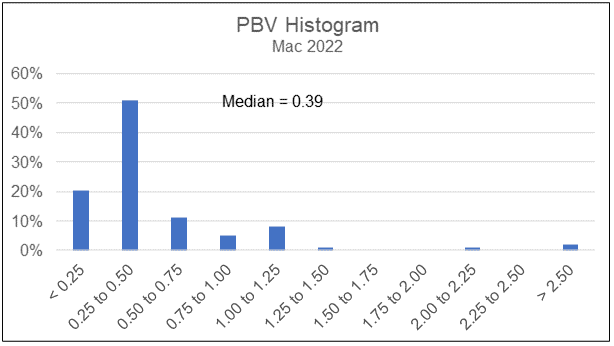

To get around this, I normally would compare the company with the whole sector. Charts 4 and 5 show the distribution of the PE multiple and PBV multiple of the Bursa Malaysia property companies as of March 2022.

- The PE multiple distributions are skewed towards both ends.

- The PBV multiple distributions are skewed towards the lower end.

Unlike the valuation of houses, relative valuation is not determining the real worth of a company.

Relative value is not intrinsic value. Relative value is assessing the worth of a company by comparing it with a panel. Intrinsic value is based on the company’s fundamentals in an absolute sense rather than relativey. That is why I rely on the Asset-based or Earnings-based approaches when estimating intrinsic values.

➡️Not certain how much you should sell your property for? Use iProperty’s Transactions Section! This online platform provides accurate and up-to-date pricing information on transacted properties in Malaysia, sourced from brickz.my.

Method 2: Asset-based valuation

This is valuing your house based on what it cost to buy the land and build the house with an adjustment for loss in usage or depreciation. You might use the historical cost to serve as the floor value or you might use the current cost.

In the context of valuing your house, this is referred to as the cost approach. As defined by Investopedia, this is a method where the price for a property is equal to the cost to build an equivalent building. It yields the most accurate market value for when a property is new than through alternative methods.

For example, if the market value of the land is RM 500,000 and the cost to construct a duplicate of the house is RM 150,000, the total cost is then RM 650,000. If the house is 10 years old, you would then have to deduct an amount for depreciation. Let’s say this is RM 50,000. Then the value of your house based on the cost method is RM 600,000.

There are several ways to determine the value of companies when using the Asset-based approach. For example, we could use:

i. Book Value

ii. Reproduction Value, and

iii. Revised Net Asset Value (RNAV)

Asset-based valuation focuses on the value of the company’s assets. In its most basic form, the Asset Value is equal to the company’s Book Value or shareholders’ Equity. The Asset Value is obtained by subtracting liabilities from assets.

The PBV multiple then gives a simple way to assess whether a stock is trading below its intrinsic value. If you have a situation where the PBV multiple is less than 1, you can conclude that the stock is cheap relative to its intrinsic value.

If you look at the current PBV distribution as per Chart 5, you can see that most of the property companies are trading below the Book Value. The median PBV currently is about 0.4. There are several ways to interpret this:

- The market is irrational.

- The market is expecting some of the assets to be impaired. In other words, the future Book Value would be lower.

- The companies are going to experience a few years of losses and hence the future Book Value would be lower.

You can see that your assessment of the prospects has a bearing on how you look at the PBV multiples. The Book Value may not necessarily reflect the market value of the assets or liability in the current environment, because the Book Value captures historical costs.

Furthermore, the depreciation rates may cause the Book Value of plant and equipment to differ from the current market values. At the same time, some intangible assets such as patents and customer relationships may not be captured in the Book Value.

Because of this, many people adjust the Book Value when using the Asset-based approach to value a company. There are several perspectives under this approach such as the Reproduction value and the RNAV.

The Reproduction Value looks at how much it will cost to purchase the assets and liabilities required to run the company. In practice, it is very challenging to determine the Reproduction Value. You are trying to estimate what it takes to re-create the company before it charges out various expenditures.

Customers’ relationship costs, product branding, and R&D expenditure are examples of items charged out. For some sectors, you may have to reduce the value of its Plant, Property, and Equipment. This is because it is now possible to build a new plant cheaper due to technological progress.

For property-based companies with significant landbank, many analysts estimate the RNAV. This is the Revised or Re-valued Net Asset Value to account for the current market value of the land. The most reliable way to estimate the RNAV is to base the property value on a professional valuer’s assessment.

However, I have seen many analysts estimating the RNAV based on the projected earnings from developing the land. This is different from what property valuers would do when they use the earnings method. So, I have doubts about some analysts’ RNAV approach as they include the development profit element as well.

The Reproduction value and the RNAV are likely to be higher than the Book Value of most property companies. As such you can understand why I consider the Book Value as the floor intrinsic value.

Valuing a REIT based on asset value

Accounting rules require the values of properties held for investment to be “mark-to-market”. This meant that the Book Value of the assets should reflect the current market value. One way to achieve this is to have the value of the properties be determined by a certified land surveyor/valuer.

This is what is happening to Malaysian REITs. Most of the REIT assets are properties. As such, you can safely assume that the assets reflect the current market values. In other words, the asset value of a REIT is a good picture of its intrinsic value.

If you take the perspective, then the PBV of a REIT can give you a picture of whether the REIT is overvalued or undervalued. Note that I am not looking at the PBV in comparison with other REITs. Rather I am using the PBV as a gauge of the difference between the market price and intrinsic value.

READ: How to invest in REITs in Malaysia?

Table 1 below presents the PBV of the Malaysian REIT at the end of Feb 2022. You can see that most of them are trading below the intrinsic value.

| REIT | PBV |

| TWRREIT | 0.28 |

| AMFIRST | 0.31 |

| HEKTAR | 0.36 |

| ALSREIT (s) | 0.46 |

| CLMT | 0.49 |

| ARREIT | 0.52 |

| YTLREIT | 0.59 |

| IGBCR | 0.60 |

| SENTRAL | 0.76 |

| UOAREIT | 0.79 |

| KIPREIT | 0.84 |

| ALAQAR (s) | 0.88 |

| KLCC (s) | 0.89 |

| SUNREIT | 0.95 |

| PAVREIT | 1.00 |

| ATRIUM | 1.15 |

| AXREIT (s) | 1.21 |

| IGBREIT | 1.33 |

Table 1: Price Book Value of Malaysian

Liquidation Value

In the property sector, you can sometimes have a forced sale value. According to Jordan Lee and Jaafar, “Forced sale value is the amount that may reasonably be received from the sale of a property under forced sale conditions that do not meet all the criteria of a normal market transaction. It is a price which arises from disposition under extraordinary or atypical circumstances, usually reflecting an inadequate marketing period without reasonable publicity.”

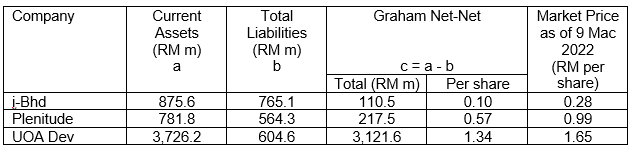

In the context of valuing companies, the equivalent is the liquidation value of a company under distress. As a retail investor, it may be difficult for you to determine the liquidation value. But there is a shortcut. The Graham Net-Net is considered by many as a shorthand for finding the liquidation value. It is defined as = Current assets – Total liabilities.

Let me illustrate this with some examples based on the Dec 2021 financial statements for a sample of property companies as shown in Table 2.

You can see that none of the sample companies is trading below the Graham Net-Net. It is not often that you find ongoing companies trading below their respective Graham Net-Net. If you do, it is a no-brainer that the stock is very cheap.

When you use Asset-based valuations, you are looking at the assets as a store of value. Many would argue that companies use their assets to generate value. A more appropriate way then is to value a company from the perspective of using the assets. This is the logic behind the Earnings-based valuation approach.

Discover properties for saleMethod 3: Earnings-based valuation

When valuing properties that are generating rental income, valuers use the income approach. This is sometimes referred to as the income capitalization approach. According to Investopedia, the income approach estimates the value of a property by taking the net operating income of the rent collected and dividing it by the capitalization rate.

For example, if the annual rental for a house is RM 45,000 but you have to spend about RM 5,000 per year on assessment, quit rent, and repairs, then the annual net income is RM 40,000. If the capitalization rate is 8 %, the value of the house is then RM 40,000/0.08 = RM 500,000.

The income approach for real estate valuation is akin to the discounted cash flow (DCF) for valuing companies. The capitalization rate is similar to the discount rate used in the DCF method. For valuing companies, the variables to consider are then what to use as the cash flows, the discount rate, and how to account for the life of the business.

There are two options when using Earnings-based approaches. The first is to ignore growth and determine what is known as the Earnings Power Value (EPV). The other way is to incorporate growth into the projections to determine the Earnings Value with growth. There are of course many valuation models. For this article, I will cover 2 simple ones assuming that there is no growth.

- EPV = Book Value X (ROE / Discount rate). Note that this formula considers the Book Value as well as the returns generated.

- EPV = PAT / Discount rate. This model looks at earnings.

There are then two issues to consider. What to use for the numerator (ie ROE or PAT as the case may be) and the discount rate. The parameters used will affect the value. I will illustrate with two examples. The first is to use the current ROE while the other is to use the past decade of average earnings to represent the PAT.

As for the discount rate, it is meant to account for the time value of money as well as the risks associated with the cash flows. I will use the cost of equity as the discount rate as this represents the returns that investors expect. I have carried out many valuations over the past 2 decades. Based on this history, I have found that the median cost of equity for Malaysian companies is 0.12. For this illustration, I will use this discount rate for all the companies.

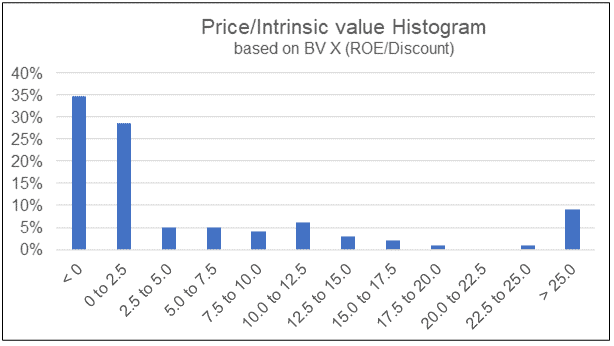

To then determine whether the stock is cheap I compared the price with the computed intrinsic value. Chart 6 shows the Price to Intrinsic value distribution based on EPV = Book Value X (ROE / Discount rate). The BV and ROE were as of March 2022 extracted from KLSEscreener.com.

You can see that because of the current economic situation, many of the companies had negative ROE which led to negative intrinsic values. The median value is about 1.1. This meant that the market is pricing the median companies at about 10 % higher than the intrinsic value. This is of course looking at it from the Book Value X (ROE/Discount) model.

Greenwald analysis for large property companies

According to Professor Bruce Greenwald, an analysis of the Asset Value (AV) and EPV provides insights into how well the company has deployed its resources. There are 3 possible scenarios when comparing the EPV with the AV:

Scenario 1: EPV = AV. This is the most common situation where the return is equivalent to the cost of capital. In a competitive environment, a business with high returns would attract competition. Eventually, any excess returns would compete away so that the company just earns its cost of capital.

Scenario 2: EPV < AV. In this case, the assets are under-utilized possibly due to some issues with the business. This could be due to poor management, or that the business is in an industry in trouble.

Scenario 3: EPV > AV. In this case, the returns generated by the business far exceed the cost of capital. I would expect the company to have some form of an economic moat for it to continue to enjoy a return that is higher than the cost of capital.

Greenwald went as far as to say that you only consider Earnings Value with growth if you have Scenario 3. In practice, it is unlikely to have a situation where the AV exactly matches the EPV. I have assumed that AV = EPV when the computed difference is within +10% or -10% of each other.

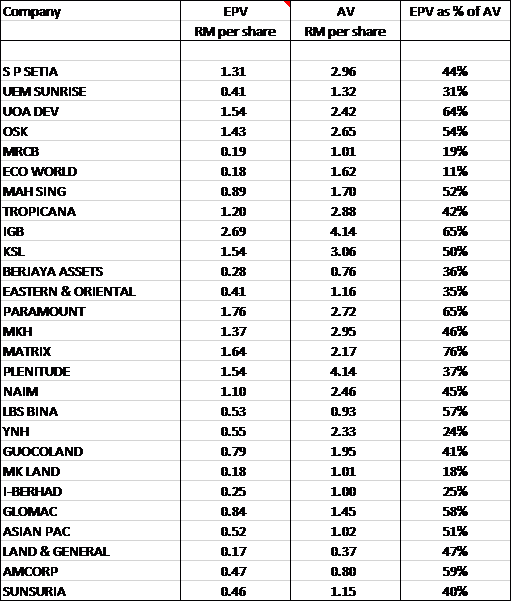

I carried out an EPV and AV comparison for the large property companies under Bursa Malaysia.

- I defined a large company as one with a shareholders’ fund of RM 1 billion or more based on its 2021 financial statements.

- The Asset value is based on the 2021 shareholders’ funds.

- The EPV was derived based on EPV = PAT / Discount rate model. I used 2010 to 2020 average PAT and 0.12 discount rate.

The results of the EPV vs AV comparison are shown in Table 3. You will notice that in all the cases, the EPV was less than the AV. On average the EPV was 44% of the Asset Value.

If you follow the Greenwald concept, it must mean that there are underutilized assets in these large companies. You should not be too surprised by the findings as many of the property companies have a large land bank. In many cases, the land bank is equivalent to decades of annual usage. Furthermore, many of them have cash reserves that generated low returns.

The interesting thing about this 44% is that it is about the same as the current PBV median of 0.4 as per Chart 6. Is this a coincidence?

Conclusion

There are several ways to estimate the intrinsic value of a property company. All valuations are based on assumptions and the different methods will result in different values because of these. That is why valuation is considered both an art and a science. The values are imprecise estimates.

To get around these “imprecise results”, many fundamental investors adopt the margin of safety concept. Instead of using the full computed value, they will reduce the computed value by a margin of safety. 30 % is commonly used.

In practice, this meant that if the computed value is RM 10 per share, you would consider the intrinsic value to be RM7 per share. In other words, you would only consider buying the stock if the market price is lower than RM7 per share. If the market price is RM8 per share, you would not consider this as cheap.

The other way around the “impreciseness” is not to rely on one valuation method, but to use a variety of approaches. The goal is for all the computed values to be pointing in the same margin of safety direction. This is following Warren Buffett’s famous saying: “It is better to be approximately right than precisely wrong.”

There are of course nuances to the various valuation methods. Consider those presented here as introductory ones. Nevertheless, I hoped it demonstrated that you do not need higher math to be able to value companies. More importantly, valuation should be complemented by a comprehensive company analysis. I would argue that understanding the business is far more important than crunching the numbers to get the value.

This article was originally published as Valuing property companies through a house valuation lens byni4value.asia and is written by Dato Eu Hong Chew.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.