| Pros | Cons |

| Can see it for yourself; no risk of delays or abandoned projects which can occur in new developments | Older properties, where repairs and renovations are likely required |

| Trendier design | Older design |

| Can move in or rent out within a year, compared to new projects with 36 or 48 months of construction period | Higher acquisition cost, including the Sale and Purchase Agreement (SPA), loan agreement, stamp duties, and many more |

| Mature neighbourhoods has more available amenities, established communities, better infrastructure, with lower chance for view disruption if there are no more land for other projects | Shared facilities within a development can become faded over time |

| Negotiable | Bank valuations can differ from asking price, which creates a financing gap |

Everything has its pros and cons, right? There’s no avoiding it and the same goes for subsale properties. To decide whether purchasing a subsale property is right for your housing or investing needs or budget, you need to know the ins and outs as clearly as possible. Let’s discover some insights about subsale properties, especially those in high-end locations such as the Kuala Lumpur city centre, Mont Kiara, and Bukit Jalil alluring.

When you’re looking for a residential property to purchase, there are three main types of property markets you can consider — primary, secondary, and auction. Primary market refers to buying a brand new property from the property developer, whereas secondary (also known as subsale) means that you’re buying from a homeowner.

Auction property is when a financial institution sells a foreclosed property due to a home loan default by the borrower. This time around, let’s zoom in on subsale properties in high-end areas.

Pros and cons of purchasing a subsale property

For subsale properties, the main benefit is that property seekers can inspect the actual unit itself. Additionally, they can review the maintenance of the facilities and common areas, the surrounding areas, population density, degree of traffic congestion, available infrastructure and amenities, and discover a thing or two about potential neighbours.

At times, purchasers may even come across good deals, when there’s a motivated seller who’s willing to let their property go at below market value. However, there are also times when a seller decides not to sell the property to you due to a better offer from another buyer.

The main issue with subsale properties is usually the renovation and repairs required. Depending on the age and maintenance of the property, you might need to redo the electrical and plumbing works and repaint.

You’ll also need to renovate if the current built-in furniture and fittings are not to your liking, or are in bad shape. Plus, there could be defects that could only be known after living in the unit for some time. Then, there’s also the possibility that some units might have an unfavourable history.

Regardless of the location of a subsale property, the points above still ring true. So, how is the subsale market in high-end locations such as Bukit Jalil, Kuala Lumpur city centre, or Mont Kiara different from other locations?

According to Darren Goh, Group Leader from Dutama Properties, these high-end locations are distinct due to the following factors:

- Prime locations: Bukit Jalil, KLCC, and Mont Kiara are prime and sought-after locations in Kuala Lumpur. They are known for their central positions, accessibility, and proximity to various amenities, business districts, and entertainment hubs. This prime location can lead to higher property values.

- Upscale: These areas predominantly feature upscale and luxury properties, including high-rise condominiums, penthouses, and landed homes. The quality of construction, finishes, and facilities in these properties tend to be high-end.

- International community: KLCC, in particular, is known for its expatriate community due to its proximity to multinational corporations, embassies, and international schools. This international presence can influence the property market and rental demand.

- Infrastructure and connectivity: KLCC and Mont Kiara, in particular, benefit from excellent infrastructure and connectivity with major highways, public transport, and easy access to Kuala Lumpur’s central business district.

If these factors appeal to you, then Darren suggests these three considerations, when looking to purchase a subsale property in Bukit Jalil, KL city centre, or Mont Kiara.

- Year of construction: The age of the property can impact its condition, maintenance costs, and resale value. Consider whether you prefer newer or older buildings.

- Asking Price vs. Bank Valuation: Compare the owner’s asking price with the property’s bank valuation to ensure that you are paying a fair market price.

- Resale potential: Consider the property’s resale potential by analysing historical price trends in the area and the overall demand for properties in high-end locations.

You may refer to iProperty Transactions for historical trends on Mont Kiara, KL city, and Bukit Jalil.

Bukit Jalil, KLCC, and Mont Kiara: An overview of their potential

Darren also shared his assessment on the potential for rental income, capital appreciation, and infrastructure or amenities, that buyers should take note of for these high-end locations.

Bukit Jalil

- Rental Income: Bukit Jalil offers a range of properties, including condominiums and landed homes. Rental income potential depends on factors such as location within Bukit Jalil, property size, and condition. Closer proximity to amenities, public transport, and educational institutions can enhance rental demand.

- Property appreciation: Over the years, Bukit Jalil has seen moderate property appreciation due to its improved infrastructure and connectivity. Property values tend to appreciate steadily, but the rate may vary between different types of properties.

- Infrastructure and amenities: The completion of the MRT Line 2 has significantly improved connectivity to Bukit Jalil, making it more accessible for residents and commuters. This has boosted the area’s attractiveness for property investment. The Bukit Jalil Sports Complex, home to various sporting events and concerts, continues to be a major attraction in the area. It also hosts the National Sports Institute and National Aquatic Centre.

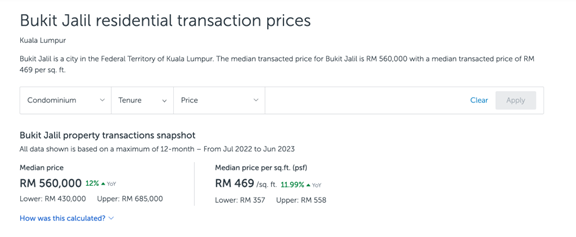

Based on iProperty Transactions, the median price for condominiums in Bukit Jalil is RM560,000, and condominiums with the highest number of transactions from June 2022 to July 2023 are:

- The Z Residence

- Bukit OUG Condominiums

- Savanna Condominium

- The Rainz

- Kiara Residence 2 (Residensi Kiara Jalil 2)

Kuala Lumpur City Centre (KLCC)

- Rental Income: KLCC is a prime area with high demand for both luxury condominiums and high-end apartments. Rental income potential is substantial, especially for well-maintained and strategically located properties. Foreign expatriates often rent properties in this area.

- Property appreciation: KLCC has historically experienced good property appreciation due to its central location, iconic landmarks, and international appeal. Property values in KLCC tend to appreciate well, making it a desirable area for investors.

- Infrastructure and amenities: KLCC’s skyline continues to evolve with the construction of iconic skyscrapers and mixed-use developments. These include The Exchange 106, a prominent financial hub, and the upcoming Merdeka PNB 118 tower, set to be one of the tallest in Malaysia. KLCC is also known for its cultural and entertainment attractions, such as the Petronas Twin Towers and the Suria KLCC shopping mall. These landmarks contribute to the area’s popularity among tourists and residents alike.

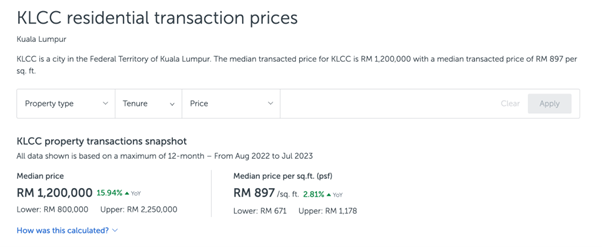

Based on iProperty Transactions, median price for properties in KL city centre is RM1.2 million, and those with the highest number of transactions from August 2022 to July 2023 are:

Mont Kiara

- Rental Income: Mont Kiara is known for its expatriate community, and rental demand for condominiums and apartments is strong. Rental income potential is relatively high, particularly in well-managed and sought-after developments.

- Property appreciation: Mont Kiara has shown consistent property appreciation over the years. The area’s cosmopolitan lifestyle, international schools, and amenities contribute to its appeal. Property values have generally seen healthy growth.

- Infrastructure and amenities: Mont Kiara has become a hub for diverse dining options, from local street food to international cuisines. It also offers a variety of retail outlets and lifestyle amenities, catering to the preferences of its cosmopolitan residents. Mont Kiara is also home to several renowned international schools, making it a preferred choice for expatriates and families with school-going children. This has contributed to steady rental demand.

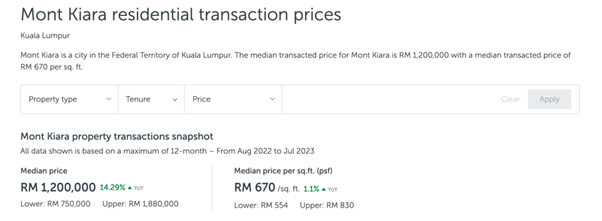

Based on iProperty Transactions, median price for condominiums in Mont Kiara is RM1.2 million, and condominiums with the highest number of transactions from August 2022 to July 2023 are:

High-end locations usually mean higher prices. Should first-time buyers look for properties elsewhere?

According to Darren, it all depends on the individual buyer’s preferences, budget and specific qualities of each property and location.

First-time home buyers should assess whether the property’s price aligns with their budget and financial capabilities. If the property is below market price or offers good potential for appreciation, it might still be a viable option.

Darren added, “High-end locations can potentially yield higher rental income due to demand from expatriates and affluent tenants. Consider the potential rental yield and whether it meets your investment goals.”

He also cautioned that high-end properties often require larger down payments and have stricter loan requirements. So, it’s important for first-time home buyers to ensure that they’re eligible for a bank loan and can comfortably manage the mortgage payments.

Darren shared three key considerations that first-time home buyers should take note of when purchasing subsale properties.

- Legal aspects: Verify the property’s legal status, including ownership documents, land titles, and any outstanding issues like disputes or encumbrances.

- Amenities: Consider nearby amenities such as shopping centres, hospitals, parks, and schools, as they affect your quality of life and property value.

- Negotiation: Be prepared to negotiate with the seller or property agent. Research market prices and be willing to walk away if the deal doesn’t meet your criteria.

Maintain professionalism and respect throughout the negotiation process. Avoid making lowball offers that could offend the seller. Present your offer in a clear and organised manner, by including all relevant details, such as your proposed purchase price, deposit amount, financing arrangements, and desired closing date.

Negotiations may take time, especially if there are multiple counteroffers. Be patient and avoid rushing into a deal.

Discover New Property Launches here!Steps to purchasing a subsale property

For those considering buying a subsale property in Malaysia, here’s a step-by-step guide to help you through your subsale property purchase journey.

1. Determine your budget

Find out what you can afford based on how much you can borrow from financial institutions. You may use these tools to help you out:

Here are some estimated figures:

- Gross annual income: RM180,000 (RM15,000 per month)

- Loan term: 30 years

- Interest rate: 4%

- Max. percentage of income to be spent on loan: 30%

- Monthly debt obligations: RM2,000

So, based on the figures above:

- Maximum monthly mortgage payment: RM4,000

- Maximum loan amount: RM838,000

Thus, if you’re looking for a unit in Mont Kiara, Bukit Jalil or KL city centre, you can go for units that are priced at about RM922,000, assuming that you’re paying a 10% down payment. For a 20% down payment, you could purchase units priced at about RM1 million.

2. Search and shortlist properties

Once you know your budget, your search can begin! Shortlist those that meet your needs, and view the units. Take your time, and also visit the property or area at different hours of the day to get a better assessment of the property or area.

“Inspect them carefully to assess their condition, layout, and features. Check for any maintenance issues or renovations that may be needed,” Darren advised.

Darren also suggested working with a reputable real estate agent who specialises in the locations you’re interested in. An experienced agent can provide valuable insights, access to listings, and negotiate on your behalf.

3. Secure the unit you want!

Decided on a unit? Then it’s time to make an offer. Once the price has been agreed between you and the seller, then you’d both sign the Letter of Offer to Purchase. You’ll also pay an earnest deposit which is usually 2% to 3% of the purchase price to the seller.

It is also advisable to hire a lawyer to assist you throughout the property transaction to safeguard your interest, such as ensuring that there are no title issues or disputes related to the property.

Darren also shared, “Hire a professional appraiser to assess the property’s value objectively. A valuation report can provide strong negotiating leverage.”

4. Apply for a mortgage loan

Check and compare financing packages from a few banks. Banks would require the property to be valued, and if the valuation is lower than the asking price, you may need to pay a higher down payment to make up for the shortfall.

5. Sign the Sale and Purchase Agreement (SPA)

The SPA is usually signed by the buyer and seller within 14 days from the date of the Letter of Offer to purchase was signed. You’d need to pay the remaining deposit upon signing the SPA. If it’s a 10% down payment, then you’d need to pay 7% to 8% of the purchase price (depending on the percentage paid for the earnest deposit).

Prior to drawing up the SPA, you should also list all the items you’d want the seller to remove or leave in the property. Once agreed upon, this inventory list will be included in the SPA.

6. Loan agreement and Memorandum of Transfer (MOT)

Once your loan agreement is ready, sign it to confirm the financing from the bank. Check to ensure that all details are accurate, and you could have your lawyer take a look as well.

Next would be getting the property transferred to you by way of Memorandum of Transfer (MOT).

7. Getting the keys to your subsale property!

This is also known as vacant possession (VP), when you can expect to get the keys to your purchased subsale property. Once the payment of the balance purchase price and Agree Apportionments (maintenance fees, water bills, and so on) have been settled between you and the seller, then the keys will be delivered or given to you, either by the buyer or through the lawyers.

Generally, it takes about 3 months to complete the purchase, unless the property is subject to restrictions such as requiring the state authority’s consent to transfer.

For the full steps, you may refer to these comprehensive guides:

- The Complete Guide On Buying A Subsale Property In Malaysia

- How to buy a subsale house in Malaysia in 7 steps

- Budget 101: What To Prepare For Before Purchasing A Property?

Financial considerations when buying a subsale property

Here’s a quick rundown of how much you’ll need to prepare to purchase the property you want.

| Item | Cost |

| Down payment | 10% of the agreed purchase price |

| Legal Fees | Sale and Purchase Agreement (SPA); Loan Agreement |

| Stamp Duty for: 1) Memorandum of Transfer (MOT) 2) Sale and Purchase Agreement (SPA) 3) Loan Agreement | 1) 1% – 4% of the purchase price 2) 0.5% – 1% of the purchase price 3) 0.5% – 1% of the purchase price |

| Real estate agent fees/commission | Maximum of 3% of the property’s sale price, usually paid by the seller |

| Mortgage insurance (MLTA/MRTA) | The premium depends on the type you choose, whether you want a plan that only takes care of the home loan or one that has an additional cash payout at the end |

| Valuation fee | From 0.25% to 0.04% of the sub-sale property’s value |

| Bank’s processing fees | Usually it’s a few hundred ringgit for the processing of loan applications |

There’s also renovation costs, and monthly maintenance fees (if you purchased a unit in a high-rise residential building). There’s also stamp duty exemptions for first-time buyers, under the Malaysian Home Ownership Initiative (i-Miliki), which accords 100% stamp duty exemption for both instruments of transfer and loan agreement for a new launch or a subsale property.

For the full list of costs involved, you may refer to this: Budget 101: What To Prepare For Before Purchasing A Property?

3 common mistakes to avoid when buying a subsale property

Remembering these tips by Darren will help you avoid unnecessary stress, and possibly, losing money.

- Ignoring legal and documentation matters: Neglecting to review the property’s legal documents, such as the title deed, land use, and zoning regulations, can lead to legal complications later on.

- Foregoing professional guidance: Not seeking advice from professionals, such as real estate agents or lawyers, can result in missed opportunities or legal issues.

- Underestimating additional costs: Failing to account for additional costs like property taxes, maintenance, and homeowners’ association fees can strain your finances.

It’s a given that all properties and locations have their pros and cons. Remember to take your time to choose the best one that suits your needs, based on your risk appetite, financial readiness, needs and opportunities.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.