In Malaysia, most banks impose a fee for loan documents. Unbeknownst to many, this practice is actually illegal. HBA has been urging BNM to crack its whip on banks to get them to reevaluate their profit-making schemes.

✉️Subscribe to iProperty.com.my on Telegram for the latest property insights.

The Bar Council’s Conveyancing Practice Committee has called out banks and said it is high time for them to review this illicit practice. Its (immediate past) chairman Datuk Roger Tan said the practice was against the law and has become a burden that consumers could do without. He said the fee was imposed on the banks’ loan documents, which borrowers sign when taking, for example – a housing loan. These documents are largely standardized documents for each bank.

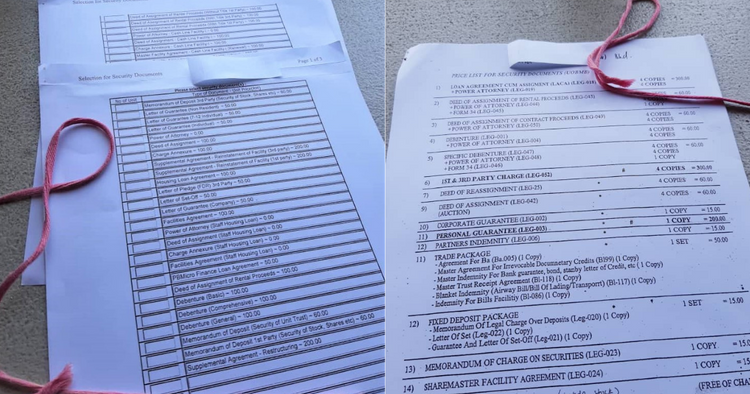

“The bank’s solicitors will typically download the documents from the bank’s website and, after completing the particulars relating to the borrower and the loan, print for the borrower’s signature,” said Tan. Banks currently charge a fee for the ‘purchase’ of these documents ranging from RM100 to RM500, even though the cost of printing the documents is borne by the solicitors.

He cautioned against imposing the fees as the sale of loan documents is a breach of Section 37(2) of the Legal Profession Act 1976. That subsection states that any unauthorised person either directly or indirectly draws or prepares documents relating to any immovable property for or in expectation of any fee or gain shall be guilty of an offence under that subsection.

Unsavoury practice had been highlighted time and time again

The National House Buyers Association (HBA) concurs with the Bar Council of Malaysia’s press statement and have reported on this dilemma in 2019, but our pleas fell on deaf ears. We have always stood against the sale of loan forms. Banks in this context refers to commercial banks, Islamic banks, other financial institutions and financial service providers. Prior to this, as early as 2013, we have written several articles on the issues related to ‘Simplified housing Loan Agreement’.

Law firms undertaking bank’s work have to purchase standardized pre-printed forms or, typically download the documents from the bank’s portal at a fee, which ranges from RM100 to RM500. There are instances where the price is higher.

Such expenses are, of course, passed down to the borrower as disbursements, usually under the column “purchase of bank’s printed forms”. Couldn’t a soft copy be made available to law firms to adopt and print at their own cost and expense? After all, printing charges are only limited to RM50, as approved by the Bar Council.

READ: Housing loan checklist: 4 documents you need to prepare if you’re an employed person

Why are banks insisting on charging fees for home loan documents?

In a recent meeting with PEMUDAH’s Technical Working Group on Getting Credit (TWGGC) initiated by Malaysia Productivity Corporation (MPC) on 28 April, HBA reiterated our stand on this issue.

The meeting was chaired by YBhg Dato’ Pardip Kumar Kukreja and in attendance were permanent members from the Association of Banks Malaysia (ABM), Association of Islamic Banking & Financial Institution (AIBIM), Bar Council, Malaysia, Real Estate & Housing Developers Association (REHDA) and Bank Negara Malaysia (BNM).

The bankers insisted that banks are not prohibited to charge ‘fees’ on standard loan documents. They elaborated that there are no regulations forbidding banks from doing so. If such acts are allowed, when attempting to regulate, there will be an issue of competition, as alleged by the banker. They emphasized that BNM does not have power over the Competition Act, 2010.

This statement is mind-boggling as senior Bar Council member, Datuk Roger Tan has repeatedly emphasized that it is an offence under section 37(2) of the Legal Profession Act, 1976 for any unauthorized person who either directly or indirectly draws or prepares any document or instrument relating to any immovable property, for or in expectation of any fee, gain or reward.

BNM stood by the bankers and clarified that:

Banks do not sell standard forms but the ‘fees’ levied reflect the actual costs incurred in ‘developing standardized loan documents’. There is manpower involved in reviewing the documents and thus, the cost is recovered via the ‘fees’.

CHECK OUT: Basic term VS semi flexi VS full flexi loan: Know the difference

Why HBA don’t agree with the banks reasoning

This sale of a standard form for a ‘fee’ has been going on since 2013. Surely, such costs must have been amortized over a period of time. Must the banks continue to profit from the sale of forms? Isn’t their major source of income derived from giving out loans? Surely, bringing the Competition Act into the equation has got nothing to do with the sale of printed forms. Contrary to BNM’s assertion that the banks do not sell the forms, don’t the act of charging a ‘fee’ implies the forms are sold ‘at a price’ which in this case is referred to as a ‘fee’?

BNM’s policies have always been in line with the Government’s aspirations especially when it comes to allocating funds for promoting affordable housing projects. Then, why are buyers of affordable housing still having to stomach the ‘fee’?

Exorbitant fees for simple letters is a common practice

The banking sector in Malaysia is a very tightly regulated industry. Any fees that banks intend to charge must be approved by BNM. It is disheartening to note that borrowers continue to be charged exorbitant fees even under the watchful eyes of BNM. Instances of borrowers being charged unreasonable fees for copies of redemption statements, EPF statements letters etc are common.

On top of that, for too long, loan borrowers have been at the losing end as many do not fully understand the terms and conditions (T&C) stated in housing loans. Even if they do understand them, they know all too well the bargaining power is not in their hands and they have to accept accordingly or risk having their loan applications rejected. Read more on Unfair housing loan terms: Have they been revised?

Is the FTFC only for show?

IN 2019, BNM came up with a policy document titled: Fair Treatment of Financial Consumers (FTFC) outlining how the banks should be responsive to the needs of financial consumers and to conduct their businesses in a way that engenders trust and confidence leading to high customer satisfaction and retention and hence, leading to sustained business performance over the long term.

Appendix 1 to the FTFC policy statement states inter-alia:

Sub-para (d): ‘does not impose excessive or unreasonable fees and charges that do not reflect the actual costs incurred in the provision of services offered or which significantly disadvantage certain groups of financial consumers’.

Has those policy statements been translated to actual and factual adherence? Has BNM conducted their annual audit check on banks including compliance and adherence of the newly minted ‘consumers friendly policies’? Has BNM or at the least with the assistance of ABM and AIBIM identified the ‘Good’ verses ‘Poor’ practices to arrive at ‘Fair’ practices?.

BNM to balance the scale

Surely, BNM cannot be waiting for the Federal Court to intervene again before it decides to act. BNM must lead and spare a thought for the borrowers and law firms who are often at the mercy of this unequal bargaining with the banks. BNM has a comprehensive legal power to regulate, supervise and monitor all participating financial systems. Similarly, the Ministry of Finance, ABM & AIBIM have a legitimate interest in the final shape of the banking industry as being one that is principled and “customer-friendly” and we sincerely hope banks heed the call.

IF you enjoyed this article, read this next: What to know about Base Rate (BR), Base Lending Rate (BLR) & Spread Rate when selecting a home loan?