While the affordable/social housing development obligations imposed on the private sector have helped reduce the burden on the government to provide affordable/social housing, the main concern is its far-reaching impact in distorting the Malaysian housing market towards high-end properties.

How is Affordable / Social Housing Development Made Viable in the Current Industrial Practice?

Providing affordable/social housing has been one of the primary concerns for many countries. Given that the development cost of affordable/social housing often exceeds the capped selling price set by the regulators, the building of affordable/social housing can only be made viable through cost subsidy.

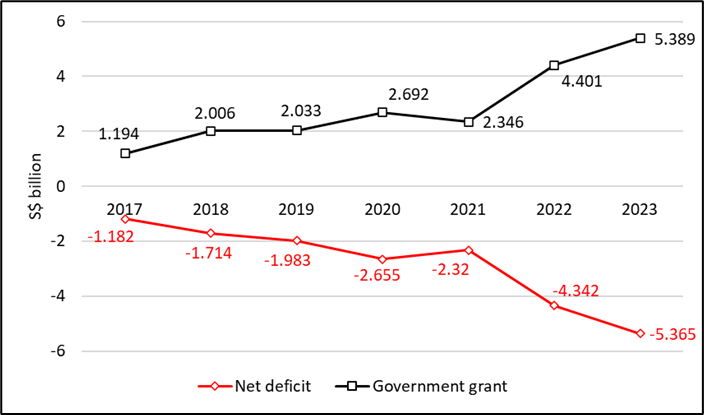

For example, Singapore’s Housing Development Board (HDB) public housing model – has been regarded as the most successful affordable housing program in the world, with nearly 80% of the population living in government-built public flats that are sold below market value and about nine in ten owning their homes – is heavily subsidised by the Singapore government (Figure 1).

Based on the HDB annual report, the cumulative government grants provided to HDB since its establishment in 1960 until 2023 amounted to S$48.361 billion (or RM161.9 billion). In 2023 alone, HDB has incurred a net deficit of S$5.365 billion (or RM18 billion) – the highest ever deficit recorded since the inception of the public housing program – and is offset via a S$5.389 billion (or RM18.081 billion) government grant.

Unlike Singapore’s HDB model, which is exclusively a government-led program, the private sector has been playing a critical role in providing affordable/social housing in Malaysia, which has been imposed as a quota nationwide. According to the National Housing Policy 2018 – 2025, every private housing development must deliver 30% of its project to affordable housing. This requirement has been in place since 1981. Imposing affordable/social housing quota in every housing development for the sake of lower- and moderate-income groups may be defended on social justice. Still, the impact of implicit tax on the free-market houses is inequitable. This is because the building of affordable/social housing is funded by the profits made from free-market housing, and these profits will cover any losses derived from pricing affordable/social housing below its market value.

The fact that cost subsidy is required in building affordable/social housing is evident in a statement made by the Ministry of Housing and Local Government (KPKT) at the Asia Real Estate Leader’s (AREL) Study Tour Hong Kong and Shenzhen, China Edition when introducing a new public housing mode – the Program Residensi Rakyat (PRR) – where each of these PRR units has a construction cost of RM300k with the government subsidising a portion of the price (as high as RM240k) so that each of these units can be sold at RM60k, making them accessible to the low-income group.

While the affordable/social housing development obligations imposed on the private sector have helped reduce the burden on the government to provide affordable/social housing, the main concern is its far-reaching impact in distorting the Malaysian housing market towards high-end properties.

Since all housing projects are required to have a certain number of affordable/social housing units – regardless of land suitability and the selling price of free-market housing – the commercially rational response by private developers is to build high-end priced houses (RM500k and above) rather than providing mid-range priced houses (RM300k to RM500k) that is affordable to the middle-class families; to cover deficits made in building mandatory price-controlled units while maximising profit margins in free-market housing. Consequently, overpriced housing dominates the free-market housing segment, making houses more difficult for the masses to access.

More importantly, such a cross-subsidy model is only suitable for large projects with economies of scale and good market conditions. In downturn markets where demand is susceptible to price changes, this model becomes unviable as the market cannot absorb higher-priced free-market units that are factored into the cost of the subsidised units. Not to mention the continuously increasing costs of doing business in the past decades that have been pressing profit margins of free-market units, making this model unsustainable in the long run.

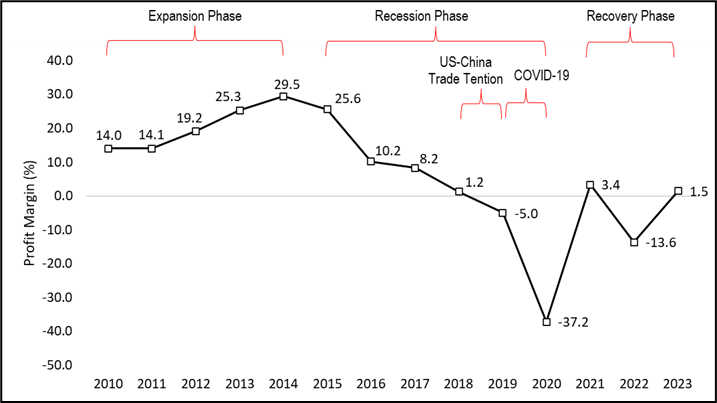

To note that the property market has been facing tremendous challenges since 2010, following an ever-increasing competitive marketplace. A contraction in developers’ profitability was prevalent: from an average of 14% increased to 29.5% during the expansion phase in 2010 – 2014, which then declined to an average of 1.2% in 2018 – in tandem with the recession induced by the US-China trade tensions – and further dropped to the bottom with an average of -37.2% upon the onslaught of COVID-19 in 2020 (Figure 2). Although the real estate market is recovering, an environment of economic growth uncertainty and rising cost of living has prompted caution about the market outlook. This could further erode the companies’ profitability.

Is Residensi MADANI a Sustainable, Affordable / Social Housing Program?

Residensi MADANI is a newly introduced affordable/social housing program that aims to help low-income people own comfortable, quality homes in the Federal Territory. It is derived from the MADANI concept, which is based on six pillars: sustainability, prosperity, innovation, respect, trust, and compassion.

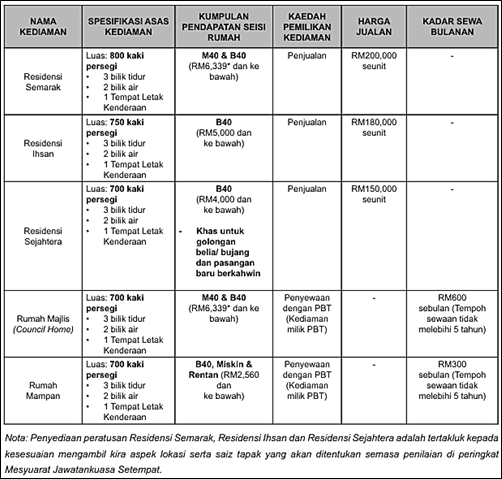

In his recent speech when launching the MADANI Civil Servants Public Housing (PPAM Madani) Pixel Permaisuri, the Prime Minister said that future housing projects in the Federal Territory must allocate one or two blocks for affordable MADANI units, which are to be dedicated to the B40 and some M40 income groups with a selling price range from RM150k to RM200k per unit, and with a minimum size of 700 square feet (Table 1).

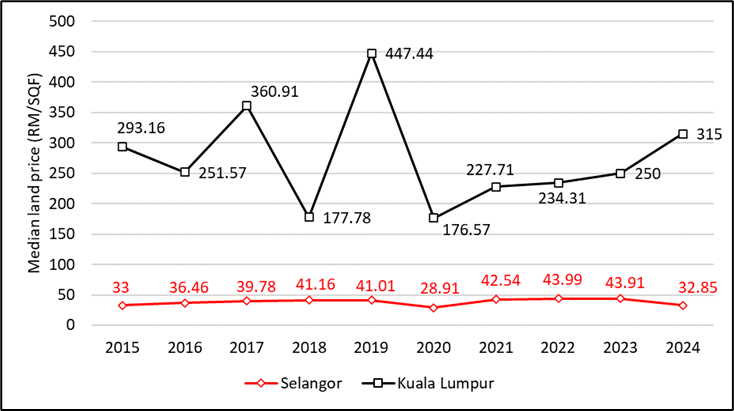

Inevitably, the building of MADANI units will require significant cross-subsidization of free-market housing, as the units are sold at below-market prices but are located in areas with higher land costs, especially in a highly urbanised area like Kuala Lumpur, where land is a scarce resource. As one can observe, the per-square-foot controlled selling prices for Residensi Semarak, Ihsan, and Sejahtera are RM250, RM240, and RM214, respectively, but based on land transactions data up to May 2024, the per-square-foot median land cost in Kuala Lumpur, alone, is as high as RM315 (Figure 3), which causes a deficit to be borne by private sector in building any affordable/social housing in Kuala Lumpur. This deficit will increase in tandem with the rising building cost and will eventually be reflected in a higher free-market housing price to be passed on to the end users.

Table 1: Specifications for Residensi MADANI Kuala Lumpur

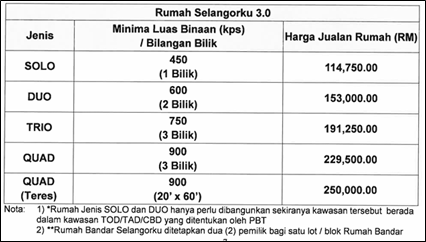

When compared to Rumah Selangorku 3.0 (RSKU) – an affordable housing program initiated by the Selangor state government where developers of qualifying developments are mandated to construct a certain amount of affordable units as part of their overall project, with specified house type, size, and capped selling price, based on the location and size of development – the per-square-foot controlled selling price of the RSKU 3.0 unit (regardless of the unit size) is found capped at RM255, which is higher than the Residensi MADANI (Table 2).

Table 2: Specifications for RSKU 3.0

One should realise that land cost plays a vital role in determining developers’ profit margins, though it is small (and often not more than 15%) of the project’s gross development value (GDV). Since construction cost is the major contributor to GDV and is subject to the free-market force, regulatory requirements, and industrial practices, which are deemed fixed and have little room for adjustment, the lower the land cost, the higher the profit margin. Given that the median land cost in Selangor is relatively lower than the one in Kuala Lumpur (Figure 3), the construction of RSKU 3.0 units becomes more financially viable to the private sector, and this would incentivise the building of more RSKU 3.0 units.

[PropTalk] Will Affordable Housing Nearby Affect My Property Value?How Private Developers Can Play a Bigger Role in Ensuring a Successful Affordable / Social Housing Provision?

There is always a “cost” to build affordable/social housing selling below market price. It is just that this “cost” is either paid by the government (like Singapore’s HDB model) or borne by the private sector (like the Malaysian cross-subsidization model). Should the effort of building more affordable/social housing be preserved and furthered, an effective “public-private collaboration” must be established.

Instead of making the public or private sector the sole party responsible for the supply of affordable/social housing, this public-private collaboration should look for ways to improve the “buildability” of affordable/social housing by addressing the following issues that often deemed as challenges faced by many in affordable/social housing development:

Scarcity of land in urban areas

Realizing that the unsustainable supply of affordable/social housing in urban areas, like Kuala Lumpur, is due mainly to the high land cost, which can only be made possible through cross-subsidization of free-market housing, the government should unlock its land in the Federal Territory for future affordable/social housing development.

“Pocket lands” or land reserves owned by government agencies or its corporatised bodies that have been left idle, especially those that are suitably located near town or transit centres, can be allocated for affordable/social housing development. By doing so, the private developers will only need to bear the construction and compliance costs of affordable/social housing development. This will free them from paying substantial land costs and enable them to provide housing units below market price in a stand-alone project, without even cross-subsidizing the profits made in free-market housing units.

In line with the development of transit rails and stations within the Klang Valley region, transit-oriented development (TOD) sites should be fully utilised and prioritised for affordable/social housing development. This is because TOD is an essential component of a comprehensive, affordable housing strategy, where living adjacent to public transportation can significantly help reduce a household’s transportation costs, thereby increasing housing accessibility.

With this respect, major TOD sites like Bandar Malaysia and Kwasa Damansara should be reviewed to refocus on large-scale affordable/social housing developments, in which developments near transit stations should be significantly incentivised with higher density and lesser parking requirements or other facilities, to ensure more members of the population benefit from the proximity to the transit stations, as well as to spread out the land infrastructure costs to make such developments are more affordable and accessible to many.

Besides, the government can provide affordable/social housing through inner-city urban renewal projects. According to a report titled ‘Decent Shelter for the Urban Poor: A Study of Program Perumahan Rakyat (PPR)’ by Khazanah Research Institute (KRI), a large portion of residential projects developed more than 20 years ago are generally not in good condition and have a negative impact on the quality of life of residents. These settlements are obsolete and no longer a good fit for the current mixed-used urban compact development concept. By acquiring and redeveloping these sites, the government can revitalise the city centre to strengthen its competitiveness and attractiveness in investment and include sufficient housing provisions for low-income households in strategic locations. Working along this line, enabling legislative provision for redevelopment (i.e. Urban Regeneration Act) is crucial.

Though Residensi MADANI is an affordable /social housing program targeted for Federal Territories, areas located in neighbouring states like Selangor can be of great potential for developing MADANI units. This is because these areas are outside the prime real estate areas and have relatively lower land costs. The government can acquire land in these areas or incentivise the private sector to take over these areas by aligning the development of mass-volume MADANI units with the TOD/transportation master plan. Again, this not only improves the buildability of affordable/social housing in a stand-alone project but also ensures the connectivity of these units with town centres, thereby overcoming the issue of unsold units due to location mismatch.

Unsuitability of location

Since private developments are imposed with a certain compulsory quota of affordable/social housing units, development of such housing could be very fragmented and may be built in locations that do not provide nor support the required ecosystem for B40 and M40 groups to live, work, and play. This is because private developers with limited and scattered land banks cannot provide an ecosystem conducive to B40 and M40 groups in every development, except for developments of larger-scale townships, which are rarely carried out in urban centres.

In the case of Residensi MADANI, where an entire block or two needs to be made into Madani housing, it will not be able to fulfil the government’s aspiration for conducive affordable housing schemes. Still, it may lead to a mismatch in demand and supply when proposed developments are outside areas served by efficient public transportation systems. This has been proven in the previous government’s affordable housing scheme – PR1MA – where the take-up rate of many PR1MA projects is low as there is a lack of integrations between these housing units and the ecosystem crucial to B40 / M40 living. Most often, these developments are ahead of public transport availability, thus making such housing units, albeit affordable, not an attractive option for the target market.

To avoid repeating the same mistakes, future affordable/social housing developments should be conducted based on the effective demands of the B40 / M40 population in the locality. It is important to require an affordable/social housing ecosystem to match the target group’s needs rather than supplying housing stocks in quantity just to accomplish the political agenda.

Just like in Singapore, where the HDB undertake the role of coordination and execution of social housing projects, the government can “master” plan its affordable/social housing program more comprehensively to achieve conducive ecosystems through close cooperation with public transport authorities, planning authorities, and other relevant parties, as well as leveraging on the large tracts of “cheaper” government’s land.

Low financial capacity for B40 and M40 income groups

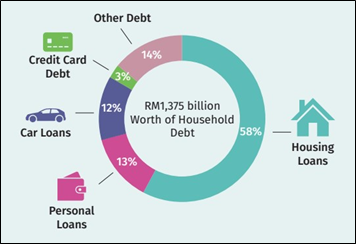

Statistics from Bank Negara Malaysia (BNM) revealed that the ratio of household debt to gross domestic product (GDP) in Malaysia has reached 81.9% in 2023, compared to 70% in 2009. In other words, Malaysians shouldered nearly RM1.4 trillion worth of debt, of which 58% is derived from housing loans (Figure 4). Meanwhile, based on the Real Estate and Housing Developers’ Association’s (REHDA) survey, many home loan applications are rejected due to the applicant’s unqualified income and poor credit, and most of the households from the B40 income group and some of the M40 households can hardly be eligible for house loans due to their high financial commitments.

In the case of Residensi MADANI, only households with a gross income of not more than RM5,000 per month are eligible for application. However, households in this income group will likely face difficulty applying for housing loans, as owning a house could burden them amid the rising living cost. In contrast, renting a house is a more viable option for them as this can reduce their exposure to severe financial risk debt. This does not mean they have to forego homeownership altogether; instead, they opt for long-term renting until they can buy as their income grows or have reached a certain income level where they no longer require social rental housing.

If the government wants to improve low-income groups’ homeownership status and living environment, the focus should be on providing more rental social housing rather than subsidising the cost of purchasing social housing for low-income groups. This is because social housing units are highly subsidised, while building social rental housing can help minimise the depletion of land in future. The government should channel more public funds towards the provision of rental social housing to eligible lower-income groups subject to income means test and close monitoring of income growth. These rental units will remain as affordable housing stock that can benefit several renters instead of one individual purchaser.

Just like Singapore’s HDB model, the government can establish a “national affordable housing trust” which will be entrusted to build and maintain rental social housing units for B40 while only building affordable housing units in suitable locations through the above-mentioned public-private collaboration and be sold to targeted M40 households who are not eligible for social rental housing. Private developers, on the other hand, should focus on providing free-market units that are built according to the local affordability threshold.

To ensure a successful rental housing system, a proper monitoring mechanism has to be put in place, not only to identify renters who have moved up financially and are able either to rent or buy outside the social rental housing parameters but also to ensure that rentals payable remain constant at a certain percentage of the renter’s income and not fixed at a nominal amount throughout their stay. This is the practice of local authorities today.

Cost subsidy by free-market housing

Cross-subsidization is not a “healthy” practice for the entire housing industry as it can skew the house price towards a higher level. Instead, it is a “desperate” move to make the existing affordable/social housing programs possible despite declining public funding for affordable/social housing. As such, a genuinely effective public-private collaboration should be the one that can improve the buildability of affordable/social housing while ensuring a “win-win situation” for both parties. The private sector should be incentivised to build more affordable/social housing rather than being heavily regulated with various legislative hurdles such as compliance cost, Bumiputera quota, rigid planning requirements, one-size-fits-all housing standards, etc., the private sector should be incentivised to build more affordable/social housing.

In areas where they are aimed for TOD projects, densities/plot ratios can be further enhanced to allow more residents to benefit from the transport system and, at the same time, reduce road congestion and car parking requirements in city centres. Whilst quality living is important, such requirements should be weighed against increased construction costs, and efforts must be made to optimise land use without compromising liveability through innovative designs and flexible planning controls.

Bumiputera quotas imposed by local authorities on affordable/social housing should be removed as building affordable/social housing for the people is a noble national agenda that should be implemented regardless of race. Additionally, any affordable/social housing development should not impose additional compliance costs to increase the project’s viability while reducing cost subsidies. Other incentives such as premium discounts, development charges and service improvement funds will also go a long way in making housing more buildable and affordable.