A move by the government to control affordable housing prices in urban areas may have been done with the best of intentions, but in practice, it will backfire and contribute towards the overhang conundrum. No amount of price control can overcome the basic economic forces of supply and demand for any significant length of time.

With increased vaccination and the reopening of state borders, more business activities will be generated in the coming months, especially considering that various countries are undergoing economic expansion and the Malaysian economy is poised to register a significant rebound in the near term. In line with this recovery, the Malaysian housing market is expected to regain its momentum.

However, for this recovery from the pandemic to be durable, a return to the business as usual (BAU) model of environmentally destructive investment patterns and activities must be avoided. Instead, the concept of ‘build back better’ should be advocated. Our response to the pandemic should include not only getting the economy back on its feet but also to address well-being, inclusiveness and various systemic vulnerabilities that can potentially impede sustainability in the long run. Hence, in the discourse around reforming the housing industry, efforts should be devoted to designing policies for efficient, inclusive and sustainable housing.

Housing initiatives under RMK-12

Many households faced sudden economic losses during the course of the pandemic and this has brought a renewed urgency to address housing affordability in the country. Under the newly released 12th Malaysian Plan (RMK-12), the national homeownership agenda has been geared towards developing and providing adequate affordable housing to the rakyat. Access to quality and liveable affordable housing will be prioritised. This will certainly set the tone for the upcoming Budget 2022 in terms of strategising measures to navigate the fragmented housing industry along the challenging road ahead.

It is heartening to see the government taking a deep dive into the crux of the issue afflicting the Malaysian housing industry: the rising cost of property development and construction activities. Escalating land costs, particularly in urban and densely populated areas, have caused significant increases in the costs of property development. Coupled with the tedious and time-consuming approval processes in meeting regulatory compliances, this has pushed the cost even higher which is then passed on to the buyer.

Under the RMK-12, the government will introduce initiatives to manage the construction costs of affordable houses. These include standardisation of charges and fees imposed by local authorities and utility providers and a review of existing industrialised building system (IBS) incentives to encourage developers to use IBS to manage costs and improve efficiency. And to increase ownership of affordable housing for selected target groups, there will be an effort to capitalise on government-owned and waqf lands.

On the demand side, access to affordable housing will continue to be enhanced through the provision of financing facilities for first-time home buyers and the Rent-to-Own (RTO) housing programme for the poor and low-income households. On top of that, a data centre on housing that integrates data from the federal and state governments as well as private developers will be established to strengthen the institutional capacity to monitor the supply of affordable housing. In short, through RMK-12, the government has outlined a more holistic affordable housing approach in an attempt to reform the country’s housing market post-COVID-19.

CHECK OUT: How much have land prices increased in KL & Selangor and what is the impact on affordable housing?

Why price control on affordable housing is not a good move

Having said that, one particular initiative – a move to control affordable housing prices in urban areas – appears to negate basic economic principles. By putting a cap on the resale or subsale values of price-controlled social housing schemes such as RUMAWIP, RSKU and PR1MA (priced at RM300k and below), the government intends to keep price speculations at bay through market intervention and to ensure these houses remain affordable in the subsale market and that they will only benefit the deserving households.

The price control is to also help increase the stock of affordable homes in the market. This is in line with the objectives of other housing initiatives for the rakyat such as limiting the purchase of affordable houses per eligible citizen to one unit and by making the construction of affordable houses a prerequisite in new township development for property developers.

No doubt doing so will increase the homeownership rate of the low-income group in the short term – which could be defended on the ground of social justice. However, this move will severely affect the value appreciation of these houses in the long run. Eventually, all houses constructed under the price-controlled social housing scheme will end up sharing the same fate as low-cost housing, driving eligible buyers away. Malaysians after all are very much driven by sentiment. Few would want to be seen owning a low-cost property.

Complications of owning low-cost property

For example, in Selangor, if a house falls under the low-cost category, consent is needed from the Selangor Housing and Property Board (LPHS) before it can be sold. This is because according to the state housing policy, once a unit is categorised as low-cost, it shall always remain as low-cost and cannot be treated as a free-market product.

House buying is the single greatest investment most people will make in their lifetimes. Failure to recognise a house as a driver of value can limit the property’s overall performance in enhancing the owner’s income status; which in turn affects its marketability among potential buyers.

Why are so few people buying affordable houses by the government?

Evidently, the rate of uptake of price-controlled social housing is lower than expected. In the case of RSKU, out of 189,892 applications received in the past five years, only 12.8% RSKU applicants (24,243) received offer letters and became homeowners. It is obvious that buying a free-market product is more attractive than buying an RSKU unit, especially when it is in conjunction with the Home Ownership Campaign (HOC) with incentives such as easy ownership schemes, additional discounts, rebates and lower deposits. Most importantly, the lifestyle and quality of living offered by free-market homes are perceived to be better than RSKU units, which are key to future property value appreciation.

Imagine a young family bought a free-market home priced around RM300k. Although the house was smaller than those under the RSKU scheme, it was decent. Over the years, as the family became financially more stable, they were able to sell the house which by then had appreciated in value and switch to a new house with bigger living spaces and better quality of life. Definitely, the upgrade cannot be accomplished if the true value of a property is limited by conditions imposed on the subsale price.

The public still associates RSKU units with low-cost housing although it is not. This is due to its limited value growth originating from perceived unattractiveness. RSKU houses are not attractive to eligible buyers due to the perception that these houses are meant for the low-income group and those who bought these houses have poor education, bad attitude and lower social class.

Since a neighbourhood tends to exhibit socioeconomic traits such as household income, family size, anticipated services and neighbourhood characteristics, the presence of low-income households in a neighbourhood is associated with social nuisance and lower living standards. Most importantly, neighbourhoods that are inhabited by low-income groups may repel high-value investment and physical development, eventually contributing to class discrimination and inequalities.

Because a neighbourhood’s amenities and disadvantages can serve as important determinants of house prices, free-market homes are better than price-controlled housing in terms of marketability. Though the maintenance fee for free-market products is higher due to common facilities and amenities, free-market products are usually better located, with good connectivity to the city centre, infrastructure and public transportation network. Taking into account the combined housing and transportation costs, this not only adds value but also enhances affordability in the long run.

POPULAR READS:

Government housing schemes for B40 and M40.

Government housing schemes for B40 and M40.

How you can buy a home worth RM500K for RM450K under the HOC.

How you can buy a home worth RM500K for RM450K under the HOC.

Rethink property price control

As a central planner, the government should avoid regulating house prices in the market, as it cannot capture the effective demands that reflect the actual market needs. This is because the government tends to treat housing affordability the same as other social policies; its aim is to help low-income and vulnerable populations without considering the dynamic change of the market over time. In fact, many cities fail to address the housing affordability crisis as they ignore the basic economic forces of supply and demand. The long history of countries implementing price control has shown that, at best, they are only effective on an extremely short-term basis. Over the long run, price control ends up hurting those it is intended to help.

The negative impact of price control can be seen in a housing policy implemented in New York City – rent control – where the government limits how much a landlord can charge a tenant or by how much the landlord can increase prices annually. While the intention of rent control is to make rental units cheaper for tenants than they would otherwise be, the net effect is it discourages real estate entrepreneurs from becoming landlords, thus creating a supply situation in which there is less rental housing available than the amount that would be created by the free market. This puts continual upward pressure on rental rates.

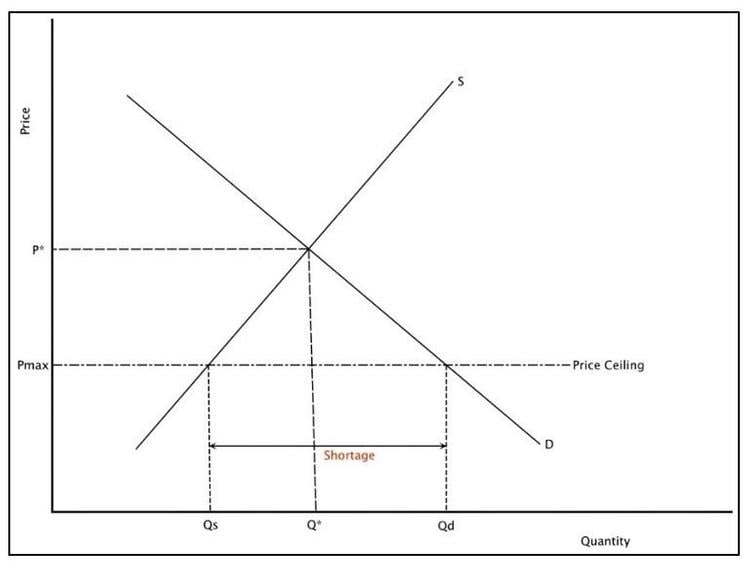

The economic basis of rent control is as depicted in Figure 1. With a price ceiling, the government has forced the maximum price to be Pmax, leading to a market equilibrium below the actual one. The original price is P*, but with the price ceiling the price falls to Pmax with quantity supplied is Qs and quantity demanded is Qd. The distance between Qd and Qs refers to a shortage, where there is a fall in producer surplus but a significant jump in consumer surplus. Consumers will demand a higher quantity at the lower price Pmax than producers are willing to supply at that price. This leads to a distortion in the market.

Case study of implementing price controls: The real effects of rent control

In reality, rent control decreases the availability of apartments. Since there is a queue of people willing to rent each apartment and landlords are not permitted to discriminate based on price, they will discriminate on whatever characteristic they please. Landlords may even ask for under-the-table payments from tenants or require renters to hand over an initial fee in order to sign the lease.

Besides, landlords have little incentive to maintain apartments, as it is more difficult to recoup the cost of improvements through the government-established price and, at the same time, there is a strong demand for apartments regardless of their condition. Consequently, the quality of housing stock also declines and the area may come to attract less affluent residents.

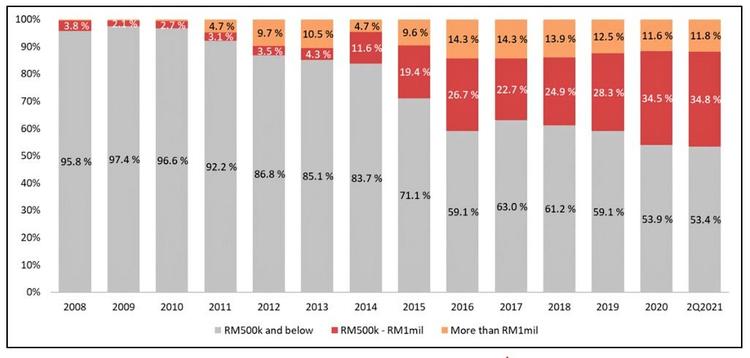

Back to Malaysia, imagine if the subsale market values of social houses are capped, the rate of uptake of these houses will likely be much lower than it is now. This will lead to an overhang in the market. As of Q2 2021, there are 16,601 units or 53.4% overhang of property priced at RM500k and below (Figure 2).

As high as 50.8% of these overhang units are contributed by houses priced at RM300k and below. This means overhang happens across the board of each housing product segment. It is worth noting that a large portion of these affordable houses is price-controlled social houses that have remained unsold for many years. Imposing price control on this category will definitely exacerbate the problem.

Addressing housing affordability certainly requires policy action across a wide range of domains while recognising complementarities and trade-offs among different policy objectives. All these challenges and associated policy choices will need to be considered against the background of a balanced ecosystem. Coping with the housing crisis will require not only a renewed commitment to building more affordable houses but also other structural economic adaptations such as higher wages for service workers and better career pipelines.

As a government measure, price controls may have been enacted with the best of intentions, but in actual practice, they do not work. No amount of price control can overcome the basic economic forces of supply and demand for any significant length of time. Therefore, the suitability of house price control needs to be considered deeply, especially from the perspective of economics. Meanwhile, the feasibility for implementing the rest of the policies also needed to be considered in detail to ensure a positive impact on the entire housing industry.

TOP ARTICLES JUST FOR YOU:

Overpriced, Oversupply & Overhang: Revisiting issues in the residential property market

Overpriced, Oversupply & Overhang: Revisiting issues in the residential property market

Top 10 most searched areas to rent in Malaysia in 2020

Top 10 most searched areas to rent in Malaysia in 2020

Corner lot vs intermediate lot vs end lot home in Malaysia: Know the difference

Corner lot vs intermediate lot vs end lot home in Malaysia: Know the difference