Real estate is often seen as an alternative investment for many retail investors. Those who are considering purchasing an investment property in Malaysian should view it as another financial risk, similar to how one might assess a stock or gold investment. This article provides one way to undertake such an analysis.

✉️ Follow us on Telegram for the latest property insights and updates.

Like any investment, there are risks when investing in real estate. While there are several ways to assess the viability of investment property, this article looks at its risks from a financial investment perspective – which is the likelihood that what a property investor makes from both capital gain and rent is less than the original investment.

We can then adopt the risk management framework to identify and mitigate negative returns when purchasing an investment property in Malaysia. This article aims to provide a framework for real estate investors to:

1. Compare risks between different locations and/or types of properties in Malaysia.

2. Establish mitigation measures to protect against getting negative returns on investment.

Financial returns from investment property

I will analyze risk from the perspective of someone buying a property for long-term investment ie. your second or third property. This will ensure that the analysis is not skewed by issues related to buying a property to live in. The returns from investing in real estate are the result of the following:

Capital gains

This is the difference between the selling price and the purchased cost as reflected in the Sale and Purchase Agreements (SPA). The capital gain will be net of the various transaction costs such as legal fees, stamp duty, real estate agent commissions, and property gain taxation in Malaysia.

Net operating income

This is the difference between rental income and the various running expenses such as statutory charges, real estate agent commission, building repairs, and income tax.

Financing charges

I will treat the financing charges as separate items by themselves as this is applicable only to those who invest using loans. The financing component will reduce total returns.

Financial returns can then be represented as Financial return = Capital gain + Net operating income – Finance charges.

The financial risk in real estate investing is then the possibility that you suffer a loss in your original investment. It does not matter whether the loss is due to the capital part, or the income part as long as it is not a positive financial return.

There are some characteristics that should not be considered as risks as they do not cause any negative returns. These are

- Real estate is capital intensive.

- Real estate is long-term investing in that it may take years for property prices to change.

- It is an asset with limited liquidity ie it takes time to sell.

- Many tax systems treat rental income differently from capital gains.

I am also coming from the perspective that if you are a prudent investor, you do not invest in real estate if

- You do not have the necessary financial resources.

- You do not have a long-term investment horizon.

- You are not going to abide by the tax code.

If you chose to speculate because you do not have the capital or other reasons, no amount of risk management is going to help you.

MORE: Memorandum of Transfer (MOT) and Stamp Duty in Malaysia

Investment Property risk management framework

- Identifying the causes that can lead to risk.

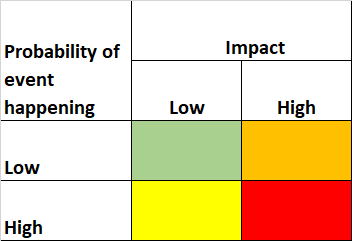

- Assessing the risk in the context of the impact and the likelihood of the occurrence.

- Planning the mitigation measure to manage the risk.

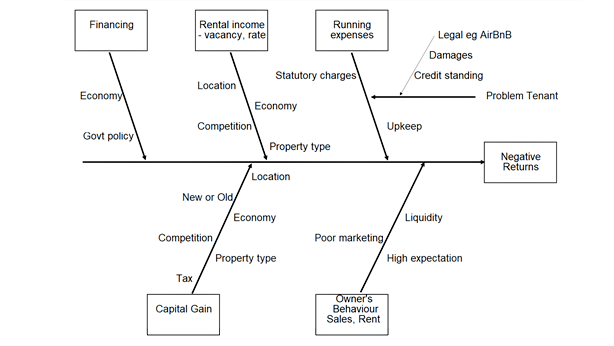

How to identify investment property risks?

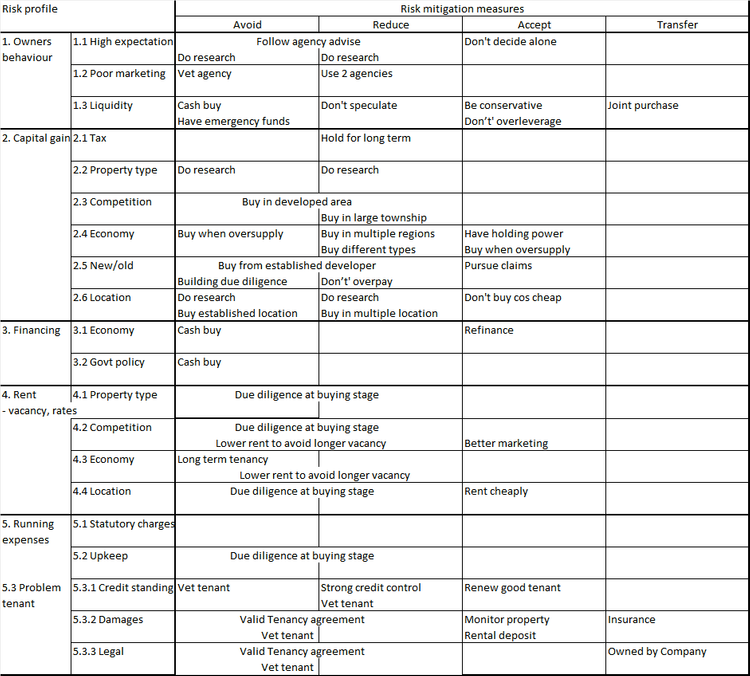

Property Owner’s Behaviour

- Having a high expectation of the selling price or rental may affect how long it takes to sell or rent the property.

- The selling price and rent will also be affected by how well the property is marketed.

- The financial position of the owner will also affect the capital gain and/or rental income. A person without a strong financial standing may be forced to sell at a lower price because of cash flow needs. The asking rent could be lower if the owner has liquidity problems.

Capital gain

- In Malaysia, real property gains tax (RPGT) varies with how long you have held the property. At the same time, the Malaysian government has in the past amended the property taxation rate.

- The capital gains are also affected by the type of houses in Malaysia as can be seen below, the Malaysian National Housing Price Index for different types of properties has changed over the past 3 decades.

Economy – The property market is cyclical and property prices will be affected by when you transact the property. Refer to When is the best time to buy a house in Malaysia?

Competition – This refers to whether there are many more developments coming up in your neighbourhood. This will affect the supply of units and hence your selling price. It is possible that new properties may make your property less attractive as they may not have the same facilities.

New/Old Property – If you are buying a house that is currently under construction, there is then the construction and completion risk to consider. Check out the latest list of blacklisted Malaysian property developers. Or, if you are buying from an existing owner, you need to check the building compliance.

Location – Location of the property will affect the capital gain. In the Malaysian context, properties in KL have higher capital gain than those in Johor.

Property Financing

- Changes in the home loan structure due to dire economic situations may affect the total amount of financing charges. Imagine the impact if you do not have interest protection clauses in your financing scheme.

- There could also be changes to the government policy on credit thereby affecting your financing charges.

Rental income

- Location – Property price is also a function of the rent. Being in the “wrong” location affects the rent as well as the potential selling price of the property.

- Economy – The economic situation may impact the demand for the properties thereby impacting the asking rent.

- Competition – Rental rates are affected by supply and demand. If there are new properties in your housing neighbourhood, it may affect your asking rent.

- Property type – Some types of properties are easier to rent and this could impact both the occupancy and rental rates.

Running expenses

- Different statutory charges eg quit rent and assessment in the Malaysian context.

- Unforeseen upkeep. If you own properties long enough, you will meet some form of disaster. Examples are burst water pipes, water tank leaking, electrical wiring problems, roof leaks.

- Problematic tenants who could either damage your property, default on rent or use the premises for illegal purposes.

Assessing the threats of investment property

- The assessment of its impact.

- The likelihood of it occurring.

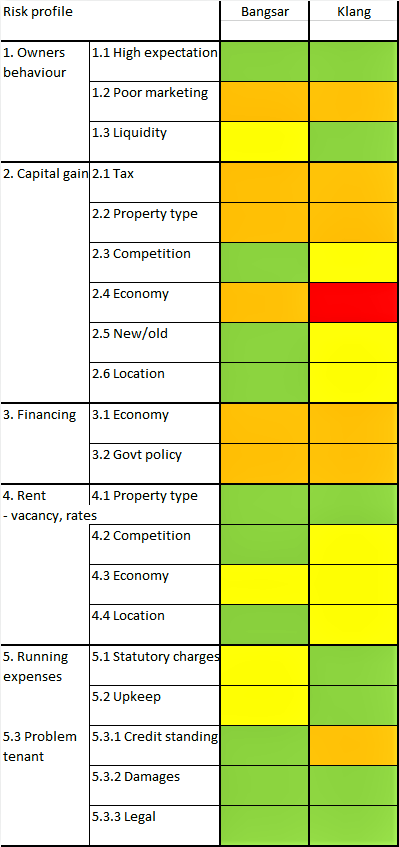

- Compare the risks between different locations and/or types of properties.

- Identify the various risk mitigation measures.

Comparing risks when investing in real estate

- Both properties are currently tenanted and you will continue with the tenancy.

- One property is located in an established part of Bangsar where the tenant has paid all the rent on time.

- The other property is located in one of the newer townships in the outskirt of Klang where the rent has been paid late occasionally.

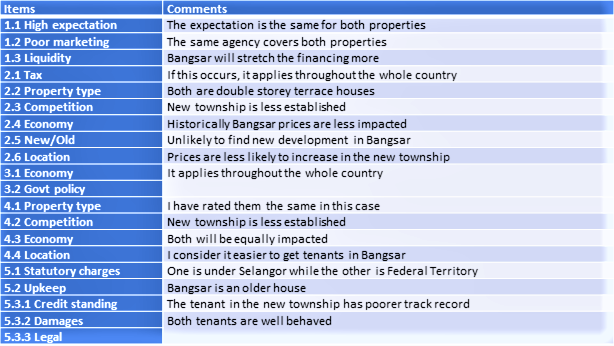

Some comments on my rationale for the risk comparisons are presented below:

- Some of the measures focus on the likelihood.

- Some focus on the impact.

- Some cover both likelihood and impact

1. Do your due diligence at the buying stage on the location, developer, and type of properties.

2. Don’t’ rush to buy or sell. If possible, buy during an over-supply situation.

3. Financing – have an emergency fund and don’t overleverage.

4. At the tenancy stage – focus on occupancy rather than rent as you will lose more waiting for another month or so to get an extra 10% rent.

5. Tenants – Vet tenants and have a proper tenancy agreement. Find out what are the stamp duty and legal fees for tenancy agreements in Malaysia.

Note: The risk item numbers in the chart corresponds with the item numbers in Chart 5 and 6 so that you can relate the mitigation measures with the threat assessment.

Pulling it all together

If you enjoyed this guide, read this next: Properties vs stocks: Which is a better investment in Malaysia?

*This article was repurposed from “Baby steps in assessing real estate risks as financial risks“, first published on i4value.asia.