Understand MOT stamp duty in Malaysia for 2026, including updated rates, exemptions, and how to calculate total property acquisition costs before you buy.

Purchasing property is one of the most important financial decisions many Malaysians make in their lifetime. Beyond the headline price, understanding legal costs and taxes, especially MOT stamp duty, is crucial for accurate budgeting.

In 2026, the Malaysian Government introduced updated policies affecting both domestic and foreign buyers, including extended exemptions and revised stamp duty rates. This guide explains everything you need to know about MOT stamp duty, how it works, who pays it, and how to calculate your total acquisition costs with clarity.

Understanding The Memorandum Of Transfer (MOT)

The Memorandum of Transfer (MOT) is a legal document that officially transfers ownership of a property from the seller to the buyer in Malaysia. It is executed after both parties have signed the Sale and Purchase Agreement (SPA) and all conditions, including payment obligations, have been satisfied. The MOT is filed with the relevant state land office to update the title deed in the buyer’s name.

Without a properly executed and stamped MOT, the change of ownership is not legally recognised, meaning the buyer could face difficulties if they later wish to refinance, sell the property, or prove title in legal disputes. This is why the MOT stamp duty must be paid and the document lodged correctly with the Land Office.

The MOT is typically prepared by a lawyer or legal firm acting on behalf of the buyer. Once executed, it becomes the primary basis for calculating stamp duty, which is a tax imposed by the Inland Revenue Board (LHDN) on instruments of transfer.

The Role Of MOT In The Property Buying Journey

The property buying process in Malaysia generally unfolds in the following stages:

- Signing the SPA: This is the agreement where the buyer and seller commit to the sale. A deposit is typically paid at this stage.

- Loan Approval: If financing is involved, the buyer’s lender assesses and approves the mortgage.

- Execution of MOT: After approval and fulfilment of conditions, the MOT is signed and submitted to the land office.

- Stamp Duty Payment: The MOT stamp duty must be paid before the MOT is accepted by the Land Office.

- Title Registration: Once the stamp duty is paid and documentation accepted, the title is updated in the Land Office.

The MOT is pivotal because it marks the point at which legal ownership enters the public record. Delays at this stage can delay possession, affect refinancing, and complicate legal rights. Many buyers mistakenly think that paying the purchase price alone completes the transaction, but until the MOT is stamped and registered, the legal transfer is incomplete.

Working closely with a conveyancing lawyer ensures that the MOT and its associated requirements, including MOT stamp duty, are handled properly and submitted in a timely manner.

What Is MOT Stamp Duty?

MOT stamp duty is a tax payable to the Malaysian Government on the instrument of transfer when a property changes ownership. The duty is charged on the higher of either the purchase price or the market value of the property and is payable by the buyer.

The purpose of the tax is to formalise the transfer instrument so that it is admissible in court and recognised by public officers. An unstamped or insufficiently stamped MOT is not considered valid evidence and could result in legal and financial complications for the buyer.

Stamp duty must generally be paid before or at the time of lodging the MOT with the Land Office. Failure to pay on time may result in penalties or interest, increasing the total cost of acquiring the property.

Browse available properties for purchase in major citiesMOT Stamp Duty Rates In Malaysia 2026

Stamp duty is a key consideration for anyone buying property in Malaysia, impacting the overall cost of acquisition. Understanding the rates and how they are calculated helps buyers plan their finances effectively.

1. Standard Progressive Rates (For Malaysian Citizens And Permanent Residents)

In 2026, the MOT stamp duty for Malaysian citizens and permanent residents continues to be calculated on a tiered or progressive structure:

| Property Value (RM) | Stamp Duty Rate |

| First RM100,000 | 1% |

| Next RM400,000 | 2% |

| Next RM500,000 | 3% |

| Amount Above RM1,000,000 | 4% |

Example: For a property valued at RM750,000:

- 1% on the first RM100,000 = RM1,000

- 2% on the next RM400,000 = RM8,000

- 3% on the remaining RM250,000 = RM7,500

- Total MOT stamp duty = RM16,500

This tiered approach ensures progressivity in taxation; buyers of more expensive homes pay a higher total amount but only at incremental thresholds.

2. Foreign Buyer Stamp Duty (2026 Update)

Budget 2026 proposals include a significant update: from 1 January 2026, the MOT stamp duty rate on instruments of transfer of residential property for non‑citizen individuals (excluding Malaysian permanent residents) and foreign companies will increase from 4% to a flat 8% of the property value.

This applies regardless of when the SPA was signed if the MOT is executed on or after that date.

This measure helps manage foreign demand and prioritise Malaysian buyers’ access to residential property, while also supporting a more balanced property market.

Stamp Duty: What It Is And How It Relates To The MOT

Stamp duty in Malaysia is a tax imposed on legal instruments. In property transactions, this includes:

- MOT stamp duty: Tax on the instrument of transfer

- Loan agreement stamp duty: Tax on the financing document (usually 0.5% of the loan amount)

The MOT is critical because it is the primary instrument that legally transfers ownership. Without stamp duty, the MOT is not considered stamped and therefore does not have full legal effect.

Stamp duty on the MOT must be calculated based on the higher of the purchase price or market value. Lawyers often estimate this amount in advance to ensure buyers are prepared, especially if the property has appreciated significantly or is acquired via sub‑sale.

Understanding how stamp duty relates to the MOT helps buyers avoid pitfalls such as underestimating costs or incorrectly lodging documents with the Land Office.

Stamp Duty Reliefs And Exemptions You Should Know

Malaysia’s Government has long used stamp duty exemptions to make homeownership more affordable. In Budget 2026, several key reliefs were reaffirmed and extended.

1. First‑Time Homebuyer Exemption

Under Budget 2026, Malaysian citizens who are first‑time homebuyers purchasing a residential property priced up to RM500,000 can enjoy a 100% exemption on MOT stamp duty on both the instrument of transfer and the loan agreement. This exemption applies to SPAs executed between 1 January 2026 and 31 December 2027.

This relief significantly reduces upfront costs, particularly for younger families or middle‑income buyers.

2. Transfers Between Family Members

In previous budgets, stamp duty exemptions were offered for transfers between parents and children or grandparents and grandchildren up to certain value thresholds.

While the specifics of these exemptions vary by fiscal year and Gazette orders, they typically help families transfer property with minimal tax if the transfer is classified as “by way of love and affection”.

Buyers should consult legal counsel and LHDN guidelines to confirm whether such exemptions apply in 2026, as reliance on them without proper documentation can lead to disputes or additional taxes.

3. Affordable Housing And Government Programmes

Certain affordable housing schemes supported or subsidised by the Malaysian Government, such as Program Residensi Rakyat (PRR) and Rumah Mesra Rakyat (RMR), may offer stamp duty benefits or reduced rates for eligible buyers. These programmes aim to address housing gaps and improve accessibility for low‑ and middle‑income groups.

4. Corporate Transfers And Special Cases

Companies transferring residential property for employee housing, corporate restructuring, or other legitimate business purposes sometimes qualify for specific exemptions or reduced rates under tax laws, subject to LHDN approval. Buyers involved in corporate acquisitions should seek professional advice to optimise their tax position.

New In 2026: Key Updates For MOT Stamp Duty

Malaysia’s property market is evolving, and staying updated on MOT stamp duty rules is essential for all buyers. These 2026 changes impact how both local and foreign purchasers plan their budgets.

1. Self‑Assessment System

Starting 1 January 2026, Malaysia is implementing a stamp duty self‑assessment system, where buyers (or their legal representatives) are responsible for assessing and declaring the correct duty amount before payment. This modernises the process and aligns with digital submission systems, but requires careful attention to accuracy and compliance.

2. Foreign Buyer Rate Changes

As mentioned, the Government increased the flat rate for foreign buyers (non‑citizens and foreign companies) from 4% to 8% on residential MOT stamp duty, effective 1 January 2026. Permanent residents (PR) remain subject to the standard tiered rates.

3. Extended Exemptions

The full MOT stamp duty exemption for first‑time homebuyers up to RM500,000 is extended to 31 December 2027, providing certainty for aspiring homeowners and making budget planning more predictable.

These changes underscore the importance of careful planning and updated legal advice when budgeting for property acquisition in 2026.

Find rental homes that suit your lifestyle and budgetHow To Calculate MOT Stamp Duty: Step-by-Step Process

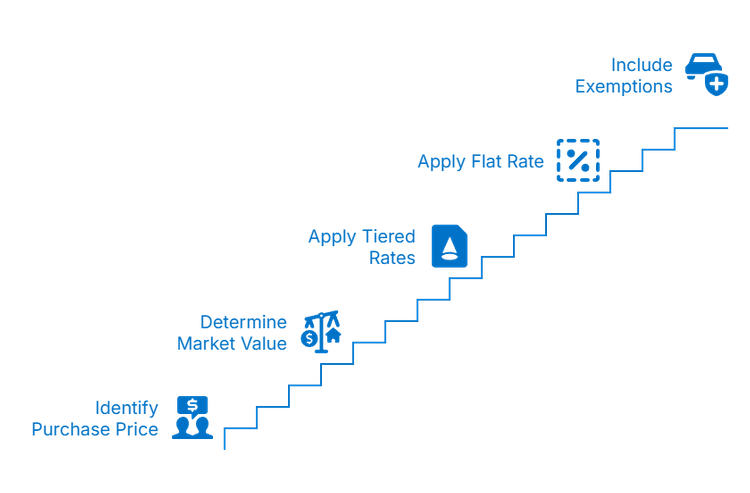

Understanding how to calculate MOT stamp duty is essential for budgeting when buying property in Malaysia. Correct calculation ensures you pay the right amount, avoid penalties, and can plan your total acquisition costs effectively. The process is straightforward if you follow the proper steps.

Step 1: Identify the Purchase Price

Start with the agreed amount in the Sale and Purchase Agreement (SPA), as this forms the basis of the calculation. Accuracy here is critical to avoid any disputes or adjustments later.

Step 2: Determine the Market Value

If the property’s market value is higher than the purchase price, use the higher amount. This ensures compliance with LHDN regulations and prevents undervaluation.

Step 3: Apply Tiered Rates for Malaysian Buyers

For citizens and permanent residents, the stamp duty is progressive. Apply the correct rates to each portion of the property price within the relevant tiers.

Step 4: Apply Flat Rate for Foreign Buyers

Non-citizens and foreign companies pay a flat 8% rate on the property value. Identifying the buyer type correctly is important to apply the right rate.

Step 5: Include Eligible Exemptions

Factor in any reliefs, such as first-time homebuyer exemptions, transfers between family members, or affordable housing schemes. Proper documentation is required to claim these exemptions.

By following these steps, buyers can calculate the correct MOT stamp duty, ensuring compliance and smoother property transactions while accurately budgeting for the total costs involved.

Total Acquisition Costs: Beyond MOT Stamp Duty

When buying a property, it is important to remember that the MOT stamp duty is only one part of the total acquisition cost. To budget effectively, you should consider all additional fees and charges involved in completing the transaction.

- MOT Stamp Duty: The primary tax on transferring property ownership, calculated on the purchase price or market value. Malaysian citizens pay tiered rates, while foreign buyers pay a flat 8%.

- Loan Agreement Stamp Duty: Tax on the financing agreement, usually 0.5% of the approved loan amount. Required if you are financing the purchase through a bank.

- Legal Fees: Charged by the lawyer handling the SPA and MOT, typically 0.4–1.0% of the property price. Covers document drafting, reviews, and coordination with the Land Office.

- Land Office / Registration Fees: Fees for registering the property in the buyer’s name, which vary depending on the state or property type.

- Valuation Fees: Charged by professional valuers to determine the property’s market value, generally 0.2–0.4% of the property price. Banks often require this for loan approval.

- Agent Commission: If a property agent is involved, the commission is usually 2–3% of the sale price, paid according to the agreement between buyer and seller.

- Disbursements: Miscellaneous expenses, including document searches, photocopies, postage, and courier fees, which collectively contribute to the total cost.

Considering all these components allows buyers to understand the full financial commitment of purchasing a property. Proper budgeting helps avoid unexpected costs and ensures a smooth transaction from start to finish.

Documents Involved During Transfer Of Ownership

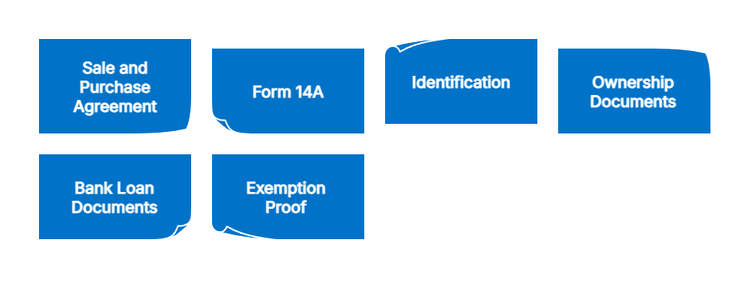

Accurate and complete documentation is critical to ensure the MOT is properly stamped and lodged. Having the right documents also prevents unnecessary delays and ensures that all legal requirements are met. The following documents are typically required:

- Signed Sale and Purchase Agreement (SPA): The SPA confirms the terms and conditions agreed upon by the buyer and seller. It serves as the legal basis for executing the MOT.

- Form 14A (Application for MOT): This is the official form submitted to the Land Office to apply for the transfer of ownership. It must be correctly filled out and signed.

- Buyer and Seller Identification: Copies of NRICs or passports are required to verify the identity of both parties involved in the transaction.

- Title Deed or Prior Ownership Documents: Proof of the seller’s ownership ensures the property can be legally transferred. For new developments, this may include developer-issued documents or master title references.

- Bank Loan Documents (if applicable): If the property is financed, loan agreements, letters of offer, and bank approval documents must be submitted.

- Proof of Eligibility for Exemptions: If claiming exemptions (e.g., first-time homebuyer relief, family transfer), supporting documents must be provided to validate the claim.

Ensuring all these documents are complete avoids delays, errors in stamp duty calculation, and possible penalties.

What Happens If The Property’s Title Has Not Been Issued?

For new developments or properties under a master title, the individual title may not be issued at the time of SPA. This situation requires additional legal arrangements to protect the buyer’s interests until the formal title is available. In such cases:

- Deed of Assignment (DOA): This temporary document represents the buyer’s ownership until the individual title is issued. It protects the buyer’s rights during the interim period.

- MOT Execution Upon Title Issuance: Once the individual title is issued, the MOT is executed and stamped at the Land Office, formally transferring ownership.

Buyers should coordinate closely with their lawyer to track title issuance timelines, as delays can impact financing, possession, or resale options.

Are There Any Other Closing Costs When Buying A House?

In addition to MOT stamp duty, buyers should budget for other fees that arise during property acquisition. Considering these costs in advance helps prevent financial surprises at the final stages of the transaction.

- Estate Agent Commission: Typically 2–3% of the property price, depending on the agreement. This fee is paid if a real estate agent facilitated the sale.

- Bank Loan Processing Fees: Charges imposed by the bank for administering the mortgage. This includes documentation, legal checks, and loan disbursement.

- Property Inspection and Insurance Costs: Some buyers pay for independent inspections, while insurance protects against fire, theft, or other property risks.

- Disbursements: Miscellaneous administrative costs, such as document searches, photocopies, postage, and courier fees, which collectively add to acquisition expenses.

Properly accounting for these costs ensures buyers avoid budget shortfalls and plan for the total financial outlay.

Get insider advice for buying, selling, or investing with property guides.Common Buyer Mistakes Related To MOT Stamp Duty

Understanding common pitfalls can help buyers avoid unnecessary delays or additional costs. Being aware of these mistakes early can save time, money, and legal complications.

- Assuming Exemptions Are Automatic: Not all buyers qualify for exemptions. Eligibility must be proven, and supporting documents must be correctly submitted to the Land Office.

- Underestimating Total Costs: Focusing only on MOT stamp duty and ignoring legal fees, loan charges, and registration fees can lead to financial shortfalls.

- Confusing Rates: Foreign buyers must pay a flat 8% stamp duty, which is higher than the tiered rates for Malaysian citizens. Misunderstanding this can cause unexpected costs.

- Delaying Documentation: Late submission of required forms and proofs can result in penalties and delay the registration process, impacting possession or loan disbursement.

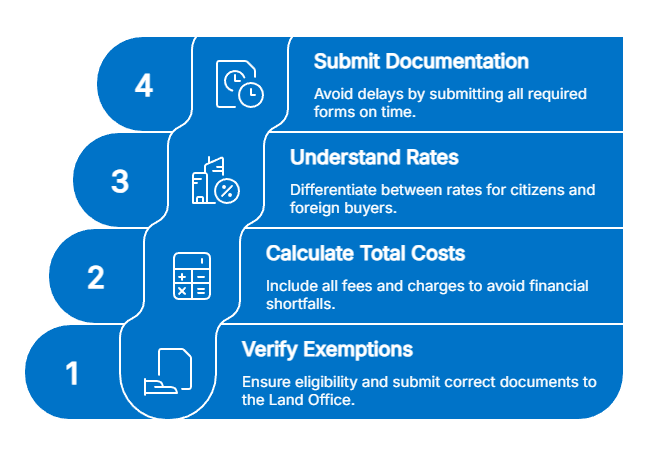

Quick Checklist Before You Budget For MOT Stamp Duty

A checklist helps buyers stay organised and avoid errors. Preparing in advance allows buyers to approach the property purchase with confidence and clarity.

- Confirm Buyer Status: Determine whether you are a first-time homebuyer, foreign buyer, or Malaysian citizen to identify applicable rates and exemptions.

- Verify Property Value for Exemption Eligibility: Ensure your property falls within the limits for any stamp duty relief or exemption.

- Discuss MOT Stamp Duty with Your Lawyer: Early consultation helps accurately estimate total costs and avoid mistakes.

- Ensure Accurate Title and SPA Documentation: Complete and correct documents to prevent delays and penalties.

- Allocate Contingency Funds: Set aside extra funds to cover unexpected fees or additional disbursements.

Key Takeaways For Property Buyers

Understanding MOT stamp duty and related costs is essential to make informed property decisions. Keeping updated on 2026 regulations allows buyers to plan accurately and avoid financial surprises.

- MOT Stamp Duty is Mandatory: All property transactions in Malaysia require payment of MOT stamp duty, based on purchase price or market value.

- 2026 Updates: Foreign buyers now pay a flat 8% rate, while exemptions for first-time homebuyers up to RM500,000 have been extended.

- Budgeting is Essential: Considering all acquisition costs, including legal fees, registration, inspection, and disbursements, avoids surprises.

- Work With Legal Professionals Early: Coordinating with lawyers ensures compliance with stamp duty regulations and smooth completion of the property transfer.

By staying informed and planning carefully, buyers can manage costs effectively and enjoy a smooth property purchase process. Proper preparation ensures compliance and reduces the risk of unexpected expenses.

Smart Planning for MOT Stamp Duty and Related Costs

Understanding MOT stamp duty and all related acquisition costs is essential for Malaysian property buyers in 2026. Proper planning, accurate documentation, and consultation with legal professionals ensure compliance, prevent financial surprises, and make the property transfer process smooth and stress-free.

Being informed about exemptions, foreign buyer rates, and total budgeting helps buyers make confident decisions and enjoy a seamless property purchase experience.

Easily plan your property purchase and check your borrowing capacity. Use the Mortgage Calculator on iProperty Malaysia.