Budget 2026 could influence how affordable homeownership feels for a first time home buyer, especially through stamp duty, tax reliefs, and overall living costs. While prices follow market forces, tax policy affects upfront costs, cash flow, and confidence, making it crucial to plan beyond headlines.

Budget announcements in Malaysia play an essential role in shaping the residential property market. Beyond headline fiscal numbers, the annual Budget serves as a policy compass, signalling the government’s views on housing affordability, home ownership accessibility, and long-term market stability.

As attention shifts towards Budget 2026, home seekers are once again assessing how tax-related measures may influence purchasing decisions. For the first time home buyer, this process is especially critical.

Without the financial buffers or equity advantages enjoyed by repeat buyers, first-time purchasers are more exposed to transaction costs, tax obligations, and policy shifts.

Why Budget 2026 Matters to the Housing Market?

Government budgets may not set property prices outright, but they play a decisive role in shaping the environment in which property decisions are made.

From affordability and financing access to buyer sentiment, fiscal policies quietly influence how confident, cautious, or committed buyers and sellers become.

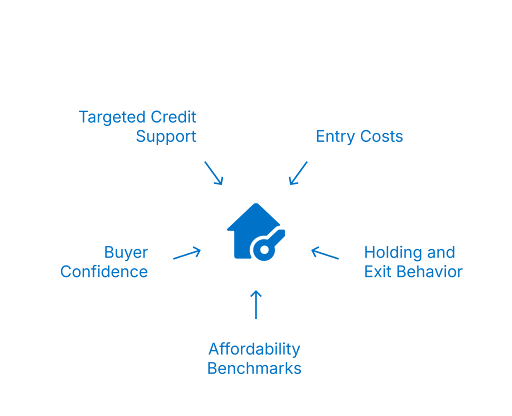

Budget measures, particularly those related to taxation and housing support, affect the market through several indirect but meaningful channels:

- Entry costs for buyers, including stamp duty, incentives, and financing thresholds, determine how accessible homeownership is across different income groups.

- Holding and exit behaviour, as tax structures and incentives can encourage owners to have longer, sell earlier, or defer transactions altogether.

- Affordability benchmarks used by banks influence loan eligibility, stress testing, and borrowing capacity.

- Buyer confidence during economic transitions, especially in periods of inflation control, subsidy recalibration, or fiscal tightening.

- Targeted credit support, such as government-backed guarantees for first-time buyers, most notably the expansion of housing credit guarantees to RM20 billion, supporting up to 80,000 applicants.

For home seekers, the impact of these policies is rarely felt at a single moment. Instead, it unfolds before, during, and after a transaction, shaping decisions around timing, financing structure, and long-term commitment.

Budget 2026 will not be evaluated solely based on new announcements. What it retains, extends, or phases out may prove just as influential.

For buyers already planning a purchase, policy continuity can offer stability and clarity, while sudden shifts can meaningfully alter affordability and confidence.

Understanding the Position of the First Time Home Buyer

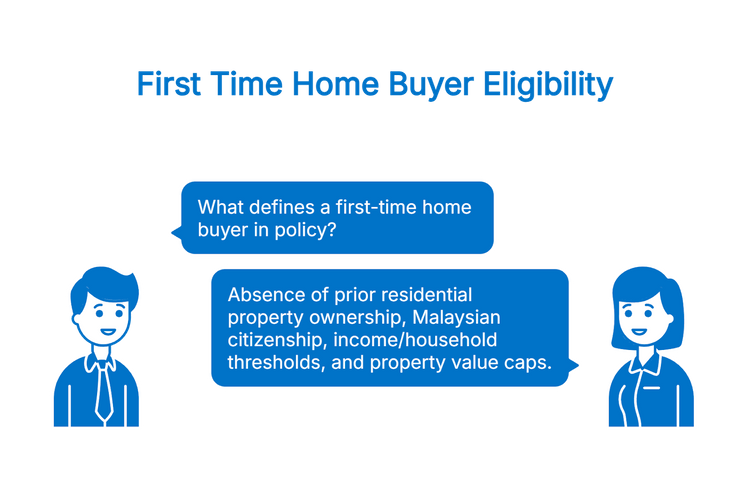

The term “first time home buyer” carries policy significance beyond its everyday meaning. In fiscal and housing frameworks, first-time buyers are often defined by:

- Absence of prior residential property ownership: Core eligibility for stamp duty exemption (100% on homes ≤RM500k until 31 Dec 2027).

- Citizenship status: Limited to Malaysian citizens (excludes non-citizens/foreigners).

- Income or household thresholds: Apply in financing schemes (e.g., Housing Credit Guarantee targets B40/M40, gig workers); not always direct for tax reliefs, but they influence broader programs.

- Property value caps: Standard (e.g., RM500k for full stamp duty exemption). Eligibility remains narrowly defined, prioritising structured criteria over broad announcements.

These definitions matter because eligibility for tax reliefs and exemptions is rarely universal. Even when incentives are announced, they typically apply to a narrowly defined buyer profile.

For Budget 2026, first time home buyer should therefore focus less on generic headlines and more on how eligibility is structured, as this determines whether a measure is actionable or merely symbolic.

Stamp Duty: The Most Immediate Tax Burden

Stamp duty is often the first significant financial hurdle buyers encounter when purchasing a home in Malaysia.

Unlike recurring ownership costs such as maintenance fees or property taxes, stamp duty is a front-loaded expense, payable early in the transaction process, typically before loan disbursement.

This timing makes it especially significant for buyers who are already stretching their cash reserves to secure a property.

For first-time homebuyers, stamp duty directly affects several practical aspects of the buying journey:

- Cash readiness means that funds must be available upfront rather than spread over time.

- Purchase timing, since insufficient liquidity can delay or derail otherwise viable transactions.

- Affordability for entry-level buyers, particularly those operating within tight price ceilings.

Because stamp duty is calculated on a tiered rate structure, even small changes to thresholds, exemptions, or reliefs can translate into noticeable differences in total transaction costs.

Policy adjustments in this area, therefore, tend to have an outsized impact on buyer sentiment and purchasing decisions.

At present, first time home buyer benefit from a 100% stamp duty exemption on homes priced at or below RM500k, a measure extended until 31 December 2027.

For eligible entry-level purchases, this effectively removes one of the most immediate and financially demanding barriers to homeownership.

Stamp Duty and Budget Cycles

Historically, stamp duty reliefs in Malaysia have been introduced during periods when policymakers seek to:

- Support housing demand

- Improve affordability for lower- and middle-income buyers

- Encourage formalisation of transactions

However, such reliefs have typically been temporary, with defined sunset clauses. Budget 2026 focused on extending the existing full stamp duty exemption for first time home buyer on homes less than RM500k until 31 Dec 2027, rather than new structures on whether existing reliefs are extended or allowed to lapse or introducing entirely new structures.

What First-Time Buyers Should Watch Closely

Rather than assuming new exemptions will appear, home seekers should examine Budget 2026 for:

- Adjustments to qualifying property price ceilings

- Clarification of joint-purchase eligibility

- Administrative simplifications affecting claim processes

These details often determine the real value of a policy, far more than its headline announcement.

Ultimately, stamp duty relief remains a policy lever that directly shapes entry affordability. Understanding its limits, timelines, and conditions is essential to making informed purchase decisions within an increasingly cash-sensitive housing market.

<a href=”https://www.iproperty.com.my/property-for-rent”>Compare rental units across locations view listings.</a>Real Property Gains Tax (RPGT): A Buyer-Relevant Seller Tax

Real Property Gains Tax is levied on property disposals and varies based on holding period and seller classification. While buyers do not pay RPGT directly, its influence on market behaviour is substantial.

Higher RPGT rates for short-term disposals tend to:

- Reduce speculative flipping

- Encourage longer holding periods

- Affect resale supply, particularly for newer homes

This, in turn, shapes price stability and resale availability.

Why RPGT Still Matters?

For buyers, RPGT affects:

- The number of resale units available within the budget

- Seller pricing strategies

- Competition between owner-occupiers and investors

Any RPGT-related adjustment in Budget 2026 would likely aim at market balance, not buyer subsidies, but the downstream effects remain relevant.

Income Tax Reliefs Linked to Home Ownership

In addition to transaction-based taxes, government budgets often address housing affordability through income tax reliefs that shape long-term ownership costs.

How Income Tax Reliefs Typically Work

Income tax reliefs related to housing are usually structured as:

- Deductions on specific qualifying expenses.

- Capped reliefs spread over assessment years.

- Measures tied to broader household or lifestyle categories.

These reliefs rarely provide immediate cash-flow relief but can reduce the long-term cost of ownership.

Implications for First Time Home Buyer

For first time home buyer, income tax reliefs:

- Do not replace upfront capital requirements.

- Offer greater value to stable, salaried households.

- Require consistent documentation and compliance.

Budget 2026 may revisit such reliefs, but buyers should evaluate them as supplementary benefits, not primary affordability tools.

Indirect Taxes and Household Affordability

Before examining the direct impact on housing, it is equally important to consider the broader cost environment in which households operate, as changes to everyday expenses often have a more subtle yet lasting influence on affordability than property-specific taxes alone.

Beyond Property-Specific Taxes

Housing affordability is shaped not only by property taxes, but also by indirect taxes and living costs, including:

- Consumption-based taxes

- Transport and fuel-related costs

- Utility pricing frameworks

These factors affect net disposable income, which, in turn, directly influences borrowing capacity.

Why This Matters in Budget 2026?

Even without housing-specific announcements, Budget 2026 could alter:

- Monthly expenditure patterns

- Debt service ratios used by lenders

- Household savings potential

These changes can quietly affect loan eligibility and comfort levels.

Taken together, indirect taxes and cost-of-living adjustments serve as silent determinants of housing affordability, reinforcing the need for buyers to assess Budget 2026 not only through property incentives but through its broader impact on everyday household finances and long-term borrowing resilience.

Financing, Tax Policy, and Buyer Expectations

To place Budget 2026 measures in the proper context, it is essential to examine how financing realities intersect with tax policy and where buyer expectations often diverge from lending outcomes.

The Limits of Tax Incentives

A common misconception among first-time home buyers is that tax incentives improve their chances of loan approval. In reality:

- Banks assess affordability independently of tax reliefs

- Incentives do not increase income figures used in assessments

- Temporary reliefs are often excluded from long-term calculations

Understanding this distinction prevents overestimation of purchasing power.

Reading Budget 2026 Responsibly

Financing-related announcements should be assessed based on:

- Actual eligibility criteria

- Duration and certainty of support

- Interaction with existing lending rules

Headline generosity does not always translate into practical accessibility.

Ultimately, informed buyers approach Budget 2026 not as a shortcut to loan approval but as a framework to be read alongside bank lending criteria, personal cash flow strength, and long-term financial discipline.

Estimate monthly loan commitments with the calculator.Preparing for Budget 2026 as a First Time Home Buyer

Rather than trying to anticipate specific policy changes, first-time home buyers are generally better served by focusing on financial readiness.

Government budgets can adjust incentives and reliefs, but they rarely alter affordability fundamentals overnight.

Buyers who are prepared tend to benefit more consistently, regardless of whether new measures are introduced.

From a practical standpoint, preparation typically involves:

- Calculating total transaction costs under existing tax and fee structures, including stamp duty, legal fees, and incidental charges, to understand the actual cash outlay required.

- Reviewing eligibility criteria for current reliefs and exemptions, ensuring alignment with income levels, property price thresholds, and first-time buyer definitions.

- Organising documentation early, such as income records and financing approvals, to reduce delays or timing risks when market opportunities arise.

- Resisting purchase decisions driven solely by expected incentives, as policy changes may be limited, temporary, or subject to conditions.

In practice, budget measures tend to reward buyers who are already financially organised, rather than those waiting for policy shifts to create affordability.

Budget 2026 as a Framework, Not a Promise

For home seekers, especially for a first time home buyer, Budget 2026 should be viewed as a policy framework rather than a guarantee of affordability.

Tax measures can reduce friction, but they cannot substitute for disciplined financial planning, realistic expectations, and market awareness.

Those who benefit most from budget-related policies are not speculative buyers but informed, prepared purchasers who understand how tax structures interact with real-world affordability.

As Budget 2026 approaches, clarity, preparation, and restraint remain the most reliable advantages any first-time home buyer can possess.

Explore new launches to compare value, assess financing options, and identify long-term potential before the market shifts.