Despite a global recession that has disrupted businesses and livelihoods, many countries in an IMF Global Real House Price Index study have seen their property prices continue to climb. Is the Malaysian property market expected to follow the same trend?

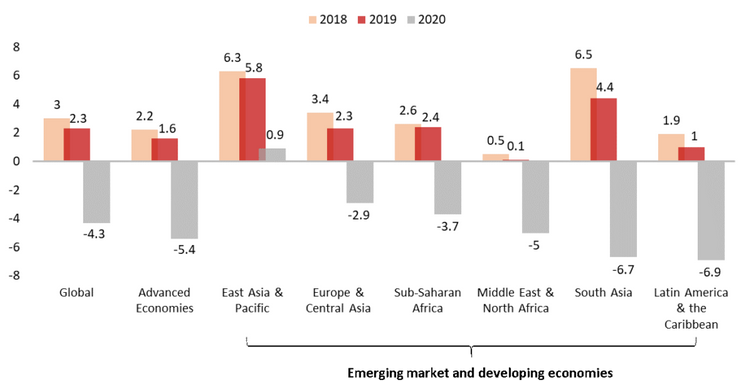

The outbreak of COVID-19 has plunged countries into the worst economic recession since World War II. According to the World Bank, global GDP in 2020 contracted by 4.3% compared to the previous year. The advanced economies of the US, Europe and Japan shrank 5.2% in GDP as they coped with their domestic outbreaks of the virus, while emerging market and developing economies in general, saw a 2.6% growth downgrades, with 0.9% in East Asia and the Pacific, -2.9% in Europe and Central Asia, -3.7% in Sub-Saharan Africa, -5% in the Middle East & North Africa, -6.7% in South Asia and -6.9% in Latin America and the Caribbean (Figure 1). These downturns are expected to undo years of progress achieved by the countries.

Malaysia’s economic performance in 2020

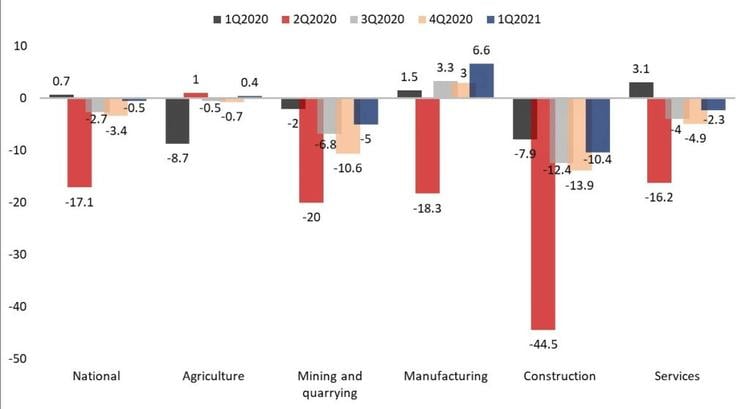

Malaysia’s GDP contracted 5.6% overall in 2020, the second-worst performance after 1998 (-7.4%). Although various economic activities have gradually resumed since Q2 2020, a full recovery to pre-pandemic levels seems unlikely, at least in the first half of 2021 in the wake of a recent new wave of infections and the reimposition of a full lockdown. Malaysia continues to record a negative GDP growth of -0.5% in Q1 2021 after three consecutive quarters of decline since Q2 2020 (-17.1%, -2.7% and -3.4%), owing to the slow performance of most major economic sectors in the country (Figure 2). Exceptions were manufacturing at 6.6% and agriculture at 0.4%.

What happened to house prices all around the world?

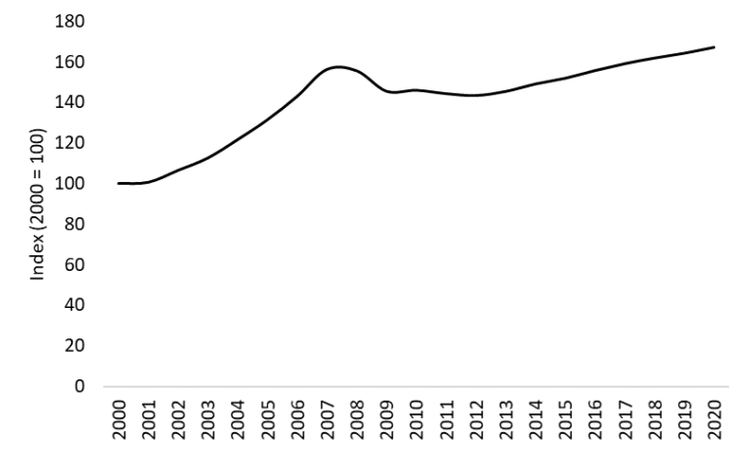

Despite the global recession that has severely disrupted business operations, reduced investments, broken supply chains, lowered consumption and caused unprecedented unemployment rates and reduced personal incomes, the pandemic has had no bearing on major housing markets worldwide. Of the 63 countries studied under the IMF’s Global Real House Price Index, 78% saw property prices continue to rise throughout 2020. The index has seen a steady climb from 100 in 2000 to 167.3 in 2020, representing a 63% growth in prices since 2000 (Figure 3).

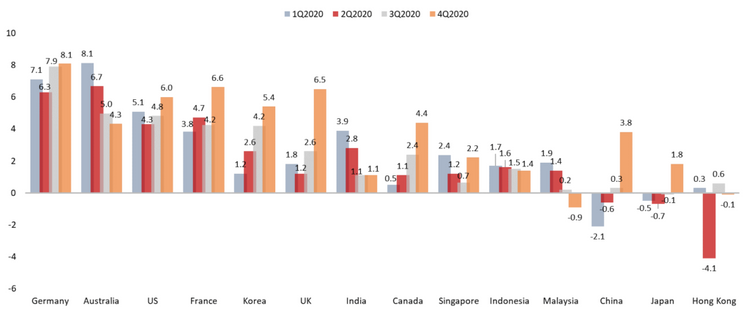

Many developed countries such as Germany, the US, France, the UK and Korea saw a rise in house prices, even at the peak of the outbreak in Q2 2020. House prices in these markets climbed even higher in Q4 2020 when restrictions were relaxed and a more pronounced recovery was seen in economic activities (Figure 4). House prices in Germany increased by 7.4% on average in 2020, followed by Australia (6%), the US (5.1%), France (4.9%), Korea (3.4%) and the UK (3%).

House price performance in Asia post-COVID-19

However, the impact of the pandemic has been uneven in markets throughout Asia Pacific as concerns continue to linger around the transmission of the virus. Japan, China, Hong Kong SAR and Malaysia saw price growths slide into negative territory in Q2 2020. Although house prices in China and Japan rebounded in Q4 2020, the growths were less than 1%. Singapore, Indonesia and India witnessed consecutive growths in prices for all quarters just like Europe and the US, but the overall growth rate was around 2%.

Why do house prices continue to increase in some countries amid the pandemic?

Apparently, strong house price appreciation amid the crisis is buoyed by ultra-low interest rates and governments’ fiscal stimulus packages. This is because when cheap money is pumped into the economies to underpin homeowners’ borrowing power and sustain banks’ balance sheets, monthly mortgage payments become more affordable and houses become more attractive. This leads to people having higher credit ratings and taking on more debt to buy a house. Consequently, property prices spiral upward. Coupled with rising unemployment, stagnating wages and high inflation – the typical signs of a crisis – housing inequality widens and many prospective first-time buyers are excluded from the property ladder.

Concerned about skyrocketing property prices and market overheat, policymakers in the developed world have tried enforcing stricter mortgage lending rules and lowering tax rates on non-property investments but to little avail, as these cooling measures are either not effective or postponed to keep the broader economic growth on track during this recovery period.

Most importantly, the property markets in the developed world are turbocharged by a stronger real demand rather than speculation, along with a shift in family spending towards housing instead of travel and vacation, concerts and shows, dining out, entertaining and commuting. In fact, the current housing boom in the developed world is an extension of what has been happening decades ago: an increase in urban populations, growing wealth inequality in real terms and a demand for housing that exceeds supply, owing to tight building restrictions that have created a housing production shortfall.

These fundamental trends do not change significantly even in the face of the COVID-19 crisis but are exacerbating as people reassess their lifestyles and contemplate larger properties in suburban areas as they now work primarily from home. Additionally, the pandemic has accelerated several years’ worth of anticipated second-home purchases by wealthier households, thereby creating a bulge in demand. These factors, when combined with fewer houses for sale during the lockdown – as the impact of the crisis on sellers are cushioned by housing loan moratorium facilities – inevitably lead to a bias towards higher house prices.

READ: Housing loan checklist: 4 documents you need to prepare if you’re an employed person

Will house prices increase in 2021 in Malaysia?

In Malaysia, there has been concern that house prices will also climb, fuelled by rock-bottom interest rates, government subsidies for homeownership and pent-up housing demand during the lockdowns. However, one should realise that there is limited credit availability to support home price increases, as borrowers are constrained by tighter credit standards and limited income growth. In fact, the country’s housing market was facing a double whammy just before the pandemic in the forms of property overhang and a weak housing demand attributed to low wage growth. These problems have worsened during the pandemic.

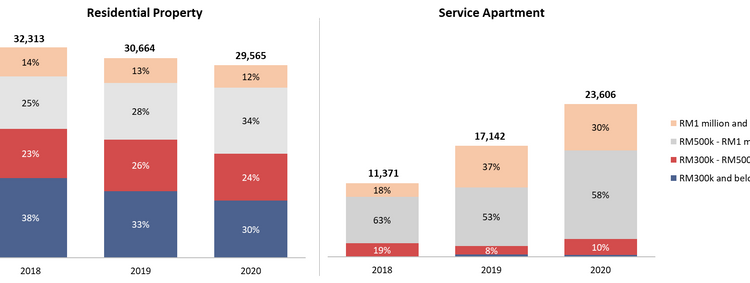

The problem is evident in high-end residential properties (RM500k and above) that make up a significant portion of the overhang inventory. The number of such properties has been increasing over the past three years (Figure 5). A similar problem is observed in service apartments. It is even more severe, where high-end units account for as much as 88% of the overhang with a drastic increase in volume from 11,371 units in 2018 to 23,606 units.

Note that affordability plays a significant role in sustaining housing demand. A drop in demand and an increase in overhang units, be it the overall number or products of a certain price range, signify that the market needs to undergo price correction. Under such circumstances, it is unlikely that house prices in Malaysia will experience a surge as what has happened in other countries.

Moreover, a rather weak market sentiment is likely to be observed in the Malaysian property market following the implementation of the current FMCO. The country has experienced this before when MCO 1.0 was first implemented in March 2020. Consumers were clearly more cautious and worried around this time. They tended to rein in their spending in the coming months as the prolonged movement restrictions have zapped consumers’ confidence and cut into their buying power, amid challenging labour market conditions. As job security has become a bigger worry now than before, it is likely that low-interest rates no longer spur their buying mood.

In a survey by the Real Estate and Housing Developers’ Association, REHDA Malaysia to assess the impact of MCO on the property industry, 75% of the respondents reported having been severely affected in Q3 2020, while 87% reported a severe impact on their sales in Q4 2020 even after movement restrictions were lifted in May 2020. On top of that, 51% of developers who launched their projects after the MCO reported sales of less than 20% in the first three months, suggesting that the MCO had a lingering effect on housing market sentiments.

As such, the reimposition of lockdown in June 2021 is expected to inhibit most economic activities. Coupled with the general perception of uncertainties, consumers and investors are likely to delay purchases of big-ticket items and banks, worried about borrowers’ creditworthiness, may not be so keen on lending. This will further challenge the recovery of the property industry.

CHECK OUT: MCO 3.0 Malaysia: Things you can and cannot do in a strata property

What property market outlook can we expect for H2 2021?

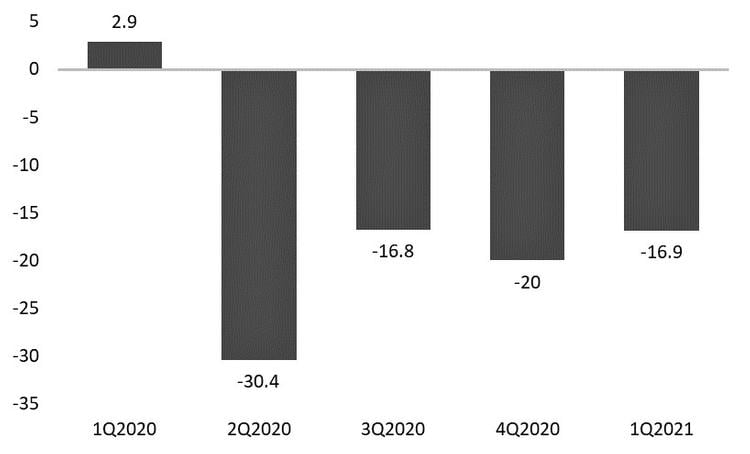

Being a sector that is highly sensitive to consumer confidence and adverse events, the real estate market has yet to return to its pre-pandemic level of performance. As shown in Figure 6, the real estate sub-sector recorded the lowest GDP growth (-30.4%) in Q2 2020, behind the services sub-sectors of accommodation (-78.7%) and transportation & storage (-43.8%).

After three quarters, the sub-sector has seen no significant improvement. On this basis, the property market is expected to experience another round of lacklustre performance in the second half of 2021; and hence, a house price surge is not likely to happen in the Malaysian property market.

If you enjoyed this article read this next: When is the best time to buy a house in Malaysia?