Premendran Pathmanathan, General Manager – Customer Data Solutions, REA Group Asia, shares some updates on the land market in Malaysia and explains how iPropertyiQ.com, a big data solution can help create demand-driven properties.

The property development business is a multi-layered one, which involves land buying, project planning, selling and the building phase. Accounting for roughly 20-25% of development costs, land acquisition is a crucial component in real estate development.

THE LOWDOWN ON LAND BANKING

Local developers usually purchase greenbelt or agricultural land as a land banking exercise for future projects. Meanwhile, those looking to build now will secure development land, which are areas designated by the respective local councils as per their town planning plan.

This is further broken down into residential, commercial, industrial or mix-development. As the land is ready for development, designated plots bear much higher price tags as compared to agricultural land.

Even then, values vary greatly between the subcategories of designated land. For instance, according to iPropertyiQ.com, which compiles and analyses data from the Valuation and Property Services Department (JPPH) and iProperty.com; Johor’s median price per acre for residential land in 2016 was RM586,000, while commercial land was 40% more expensive at RM821,000 per acre. Comparatively, the median price per acre for Johor’s agricultural land was only RM69,000!

Though designated, development land still bear agricultural titles and could either be orchards or plantations at the moment. Developers will have to pay a conversion fee to the local authority to convert the status of the land once they have gotten their building plans approved.

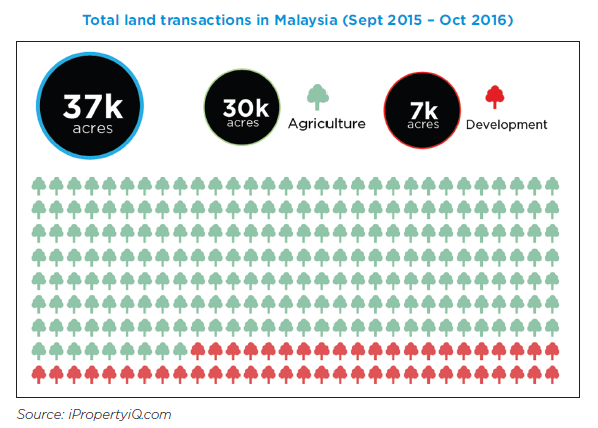

LAND MARKET ACTIVITY REPORT

Latest data from iPropertyiQ.com showed that a total of 37,000 acres or 1.612 billion sq ft of land was purchased from September 2015 to October 2016. Approximately 18.9% or 7,000 acres consisted of development land.

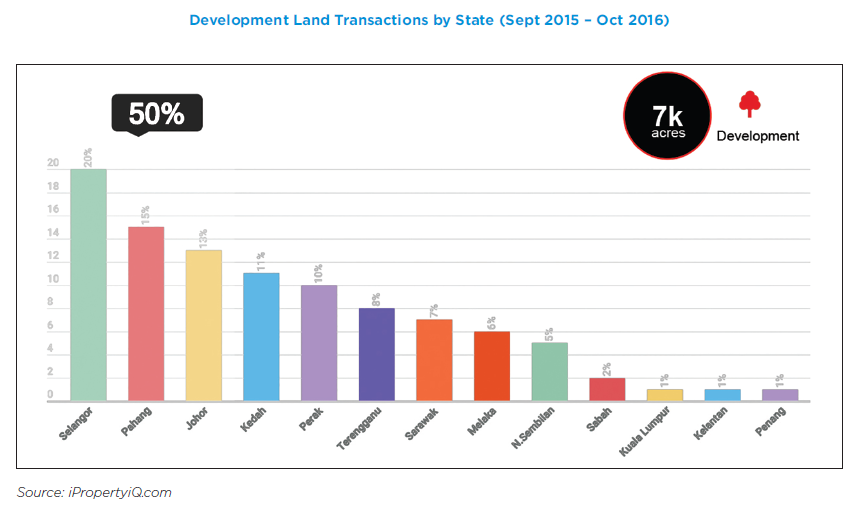

Half of the transactions were garnered by three states – Selangor, Pahang and Johor. This shows there is a great demand for properties now in these three states and developers are looking to fill the demand-supply gap.

Major development land transactions within The Greater Klang Valley Conurbation (including Negeri Sembilan) were recorded in the areas below:

THE DEMAND-SUPPLY DISPARITY

Mark Twain’s famous quote, “Buy land, they are not making it anymore” rings true. Nevertheless, the oldage practice of land banking has gone beyond shoring up supply. Developers are not just in the business to build, they must make sure that their units sell as well. This has proven to be especially challenging in the past two years, with the rising cost of living and affordability issue plaguing Malaysian consumers.

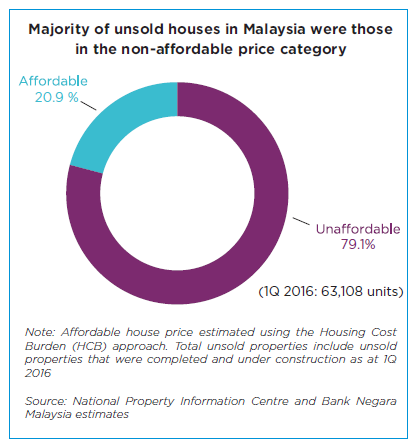

A major concern is the demand-supply gap facing the local housing industry, where properties in the market do not match the masses’ affordability level. Many new launches, especially those in the more urbanised states, consist of properties that are catered for foreign investors and wealthy individuals.

Bank Negara Malaysia’s 2016 Annual Report highlights this demand-supply gap as well:

Hence, a developer’s biggest concerns for land acquisition today are:

• Which property type is doing well now?

• What are the popular home sizes & prices of properties that people are buying in a specific area?

• How much does it cost to purchase development land in a specific area?

TURNING DATA INTO BUSINESS VALUE

In deciding what type of land and where to buy, most developers resort to feasibility studies. The thing is data collection and analysis is a time-consuming affair, a bane in this day and age where consumers trends fluctuate rapidly. However, with big data sourced from JPPH and iProperty.com, decisions can be made less complicated as it is based on real-time information.

Big data analytics has been touted as the next big thing, but many are still wondering about its effectiveness as there is uncertainty over the data source. Good analytics depends on clean data, which is not easy to obtain. Data from iPropertyiQ.com however, is nothing if not top-notch – data sourced from JPPH officially records property transactions once the stamp duty for the sales and purchase agreement is paid. Thus, it provides the most up-to-date, relevant information on sub-sale property transaction prices.

SELLING PRODUCTS THAT BETTER FIT CONSUMERS’ REQUIREMENTS

In addition, users are given simplified access to trends and consumer behaviour in relation to the property market through the analysing of For Sale/Rent listings from iProperty Group’s websites.

While this certainly is an added edge, the hero here is that the data tabs/breakdown into SEARCH, VISIT and LEADS and this provide a clear picture of consumers’ demands. The first section showcases which areas property purchasers are interested in; the second displays which property type and size that consumers are looking for in that area and the last section which is a record of genuine interest, reveals which price range is deemed affordable as consumers send enquiries to real estate agents for a specific property.

By filtering through each of these sections and then comparing them with actual transactions by JPPH, developers can determine where the demand-supply gap is and look to cater to the property buyers’ needs.

GET HELP WITH FINANCING

Home buyers are not the only one facing financing issues. The increase in construction costs and the property market slowdown has made banks more cautious in assessing a project’s feasibility, thus presenting developers with the challenge to obtain funding support for land acquisitions.

Key data from iPropertyiQ.com can help assist and hasten the financing process. The website provides developers with various indicators which showcase both an area’s and product’s performance. These indicators include latest transaction volumes, median price PSF, y-o-y capital growth, rental yield and even asking median rent. These figures will enable a developer to prove his case that his planned product will do well in the current market and cater to purchasers’ demands, thus generating sufficient sales. After all, what matters to a bank when it comes to assessing a loan’s risk is hard facts and figures.

Are you looking for data insights for better business decisions? Drop an email to [email protected] and let us help you.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.