We reassess the ‘3O’ issues of Oversupply, Overhang and Overpriced in the Malaysian housing market and provide some arguments as to whether property is still a good investment prospect in this post-pandemic era.

The Malaysian economy registered strong growth in Q2 2022 at 8.9%. Granted this could be attributed to the relatively lower GDP base in Q2 2021 when the country was under Full Movement Control Order or FMCO, growth in April and May 2022 was particularly robust, underpinned by a steady recovery in labour market conditions, ongoing policy support and normalisation of economic activities as the country transitioned to the endemic phase of Covid-19. On this basis, the country’s economy is projected to grow further for the remainder of the year.

The property market appears to be stabilising after a series of unforeseen global events since 2018. The supply side seems to be adjusting towards meeting the needs of home buyers in terms of volume, price and product type. However, many households are facing financial distress due to stagnating incomes. As people need to live frugally, they have limited discretionary cash to invest in property, resulting in a weak buying sentiment.

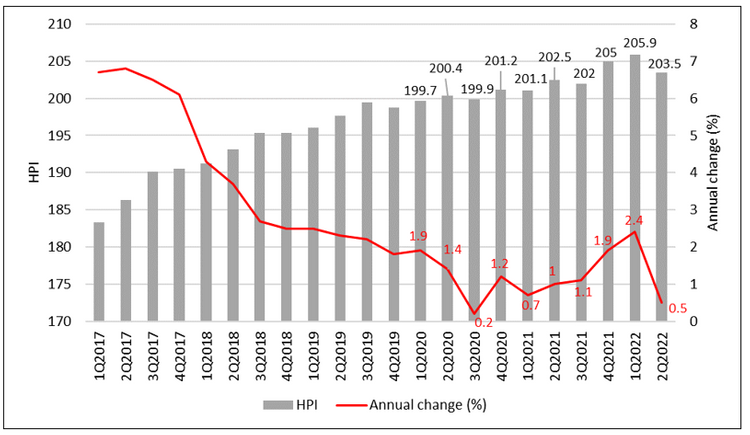

This is evident in a drop in the consumer sentiment index (CSI) from 108.9 in Q1 2022 to 86 in Q2 2022 despite robust GDP growth. Meanwhile, the Malaysia house price index (HPI) fell from 205.9 in Q1 2022 to 203.5 in Q2 2022. This not only marked the worst quarterly contraction of 1.2% since the start of the pandemic, but was also a continuation of sluggish annual growth at 0.5% (Figure 1). On top of that, rising interest rates have increased overall borrowing costs. With the ringgit weakening amid this high-cost environment, inflation is expected to trend higher, potentially leading to a softening market for the rest of the year.

Is there a housing bubble in Malaysia?

Consumer interest in property appears to fluctuate in the current economy, especially in terms of the housing credit dynamic in both internal aspects (i.e., household disposable income, financial capability, mortgage debt) and external aspects (i.e., interest rates, taxes). Nevertheless, it is important to note that a sustainable improvement in property consumer confidence continues to be linked to a good long-term prospect for capital appreciation. As long as the fundamentals of the market remain intact, the housing market outlook will eventually improve, stimulating the propensity of households to enter the property market even in an unfavourable financing climate.

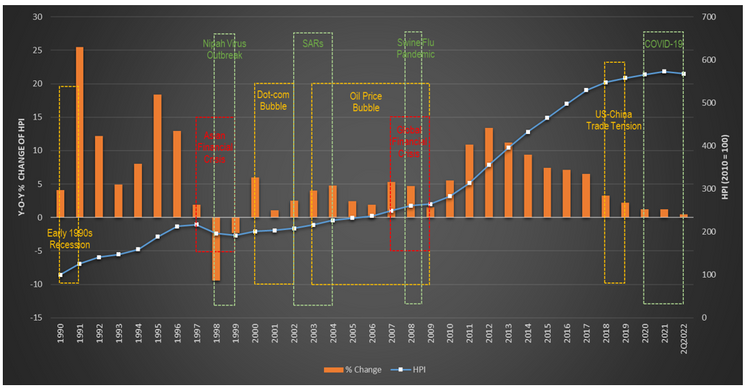

The fact of the matter is the Malaysian property market is not yet in a high-risk low-return proposition, much less a housing bubble. This is because, after the 1997 Asian Financial Crisis, the country’s property market has become less affected by unprecedented global crises. Malaysia’s house prices grew steadily from 2000 to 2010 with a compound annual growth rate (CAGR) of 3.47%, despite the 2000 Dot-com Bubble, the 2008 Subprime Global Financial Crisis and the 2009-2010 Swine Flu Pandemic (Figure 2).

The Malaysia house price growth from 2010 to 2015 was particularly steep with a CAGR of 7.63%, driven by a favourable lending policy – market optimism from buyers regarding future capital appreciation from property investment as well as the introduction of developer interest-bearing scheme (DIBS) helped drum up buying sentiment. However, a series of cooling measures put in place by Bank Negara Malaysia (BNM) since 2014 has prevented the property market from overheating. The country’s housing market is said to enter a period of adjustment. Coupled with limited financing availability due to tighter credit standards and limited income growth to support home price increases since 2018, the current property market appears to be in no danger of any impending bubble.

Housing supply-demand ratio shows improvement in 2022

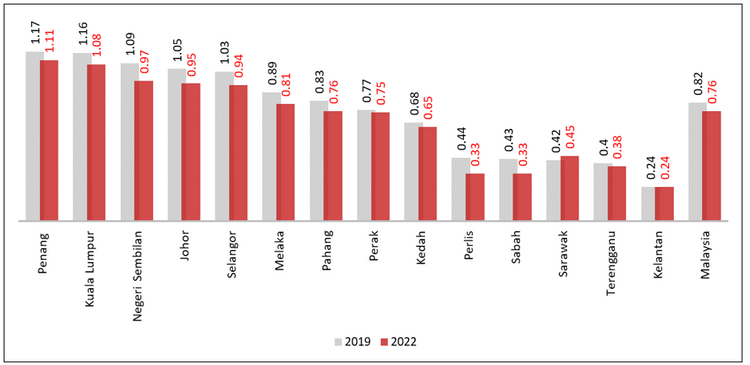

Another indicator that the country’s property market is stabilising after the disruption of the pandemic is the low supply-demand ratio. This ratio of existing housing stocks to the number of households exposes any imbalance between the supply and demand of housing in a country or state. Prime property markets that were considered “oversupply” in 2019 (with a ratio of more than 1.1) and “near-to-saturation” (approaching a ratio of 1.1) are seeing improvements in 2022 (Figure 3). This is mainly due to the supply side of the market which is seen to be more responsive and sensitive to the current housing demand. Also, helping matters is the increase in the number of households with the formation of many smaller households, thus pushing the ratio down.

With the exception of Penang where the supply-demand ratio is still above 1.1, other prime markets such as Kuala Lumpur, Negeri Sembilan, Johor, Selangor and Melaka are seeing relatively low ratios in 2022. This should signify a balanced supply and demand and healthier growth prospects. The downsides are few. The current property market is still a good prospect for long-term investments.

However, the high capital growth phase led by speculation herd instinct and rapid expansions in property investment volume is becoming less prevalent in these prime markets. Rather, the prime housing markets in Malaysia are now guided by rational demands that emphasize buying for own stay, lifestyle living and upgrading, and higher quality consumption. As for the rest of the market with ratios of lower than 1.0, expansion in volume is expected to continue with intensifying urban agglomeration processes, increases in household income and decreases in household size.

SEE WHAT OTHERS ARE READING:

🤫 Buying a house with cash vs taking on a loan

😊 2022 Top condos for sale in KL

Some adjustment in house prices

There were pricing mismatch issues in the housing market before the pandemic, where many houses were priced out of the market. Now, overpricing has become less apparent in the residential housing segment. This is in contrast to other countries that are going through a house price surge since the outbreak of the pandemic due to increasing demands – which are pushed up by factors such as ultra-low interest rates, government stimulus, savings accrued during lockdowns and shortage in housing supply.

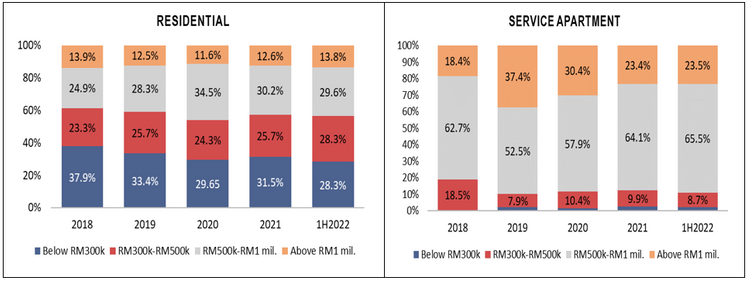

The breakdown of residential housing overhangs by price range for the past five years reveals that overhang happens across all residential property categories, with most of them coming from products priced at RM500k and below (Figure 4). This indicates that pricing mismatch has contributed less to the problem of residential housing overhang. Instead, it is likely caused by reduced housing affordability due to depleting household incomes. However, overpricing is still the major cause of service apartment overhangs as a majority of them are priced at RM500k and above. In Johor, for example, high-end serviced apartment launches appear to be an anomaly since 2016, with both property prices and volume several folds higher than the national average.

Property developers must focus on value creation

Since the current property market is generally perceived as undergoing a transition towards a less attractive investment with low rental yields and sluggish house price growth, a significant drop in the overhang of serviced apartments and smaller units such as studio apartments, SOHOs and one-bedroom units is unlikely to happen in the near future, despite a steady decline in supply.

Overall, although the pandemic has brought challenges along with an economic downturn, it has also brought opportunities and changes. A significant reset can be seen in both the supply and demand sides of the property market. Property developers need to adapt their strategies to the new business environment and go back to the fundamental principles of property development when determining the types of products to be released to their target buyers. They should not rely heavily on market-spurring initiatives.

People in a developing country like Malaysia still aspire to own homes. It is just that potential buyers have become more realistic and cautious. Many are adopting a wait-and-see approach in anticipation of economic and political uncertainties in the near future. In response, property developers should highlight value creation when positioning their products. The old price war strategy to boost a company’s sales and revenue in the short term is unlikely to resonate with today’s home buyers. This is because in pursuit of competitive pricing, property developers tend to cut costs and downsize units, resulting in an overall drop in quality of design, aesthetics and landscapes. Instead of competing on prices, products that deliver practical, humanised and value-added living are more likely to attract buyers in the post-pandemic era.

If you enjoyed this article, read this next: Titiwangsa Station: Convergence of 5 Rail Lines And Its Impact on Properties