Insights from this article are drawn from the Latest Household Income Survey (HIS) Report 2022 released by the Department of Statistics Malaysia (DOSM).

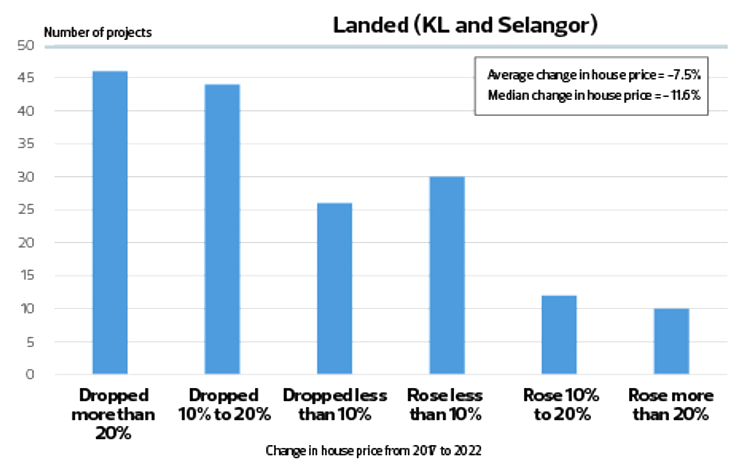

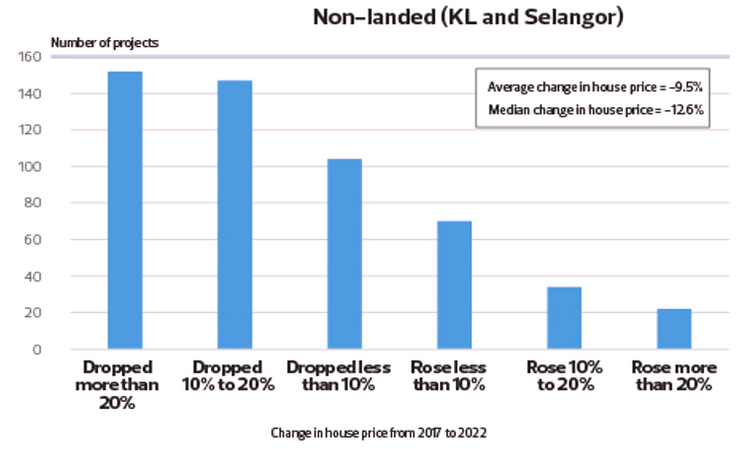

Earlier this year, an article published online demonstrated that house prices in Selangor and Kuala Lumpur are not always in a rising trend as one perceived. Instead, by comparing prices for the same property in 2017 and 2022, the article shows that houses have become more affordable today than they were 5 years ago. Also, many property projects were found experiencing a price drop of more than 10% and this number far exceeded those that have appreciated (Figure 1).

While this could be a fair point to counter the statement made by socialists saying that “house prices in good locations are always out of an ordinary household’s reach; it also indicates that houses located in prime real estate areas are not guaranteed to experience value appreciation.

Figure 1: Change in house price (landed and non-landed) from 2017 to 2022.

More importantly, falling house prices do not necessarily improve one’s housing affordability, because house prices are one of many economic indicators that investors use to keep a pulse on broader economic trends and potential shifts in the stock market. Due to the wealth effect (Figure 2), rising house prices could encourage consumer spending, which then leads to higher economic growth. In contrast, a sharp drop in house prices could adversely affect consumer confidence and the overall real estate ecosystem, thereby leading to slower economic growth or even contributing to economic recession. Hence, should the government aim to enhance people’s housing affordability, improving household income is another viable option.

With the release of the latest Household Income Survey (HIS) Report 2022 by the Department of Statistics Malaysia (DOSM), valuable insights can be drawn to assess the country’s current household income status. In general, states in the central region (Kuala Lumpur and Selangor) recorded the highest household income. The three states in the southern regions (Negeri Sembilan, Melaka, and Johor) fared better than those in the northern regions (Kedah, Perak, and Perlis) except for Penang; as well as the east coast region (Pahang, Kelantan, and Terengganu) and East Malaysia (Sabah and Sarawak).

This is due to the socioeconomic disparity in the level of urbanisation, population density, educational level, migration, employment structure, agglomeration of T20 households etc. By taking Kuala Lumpur and Kelantan as examples, the median household income gap between the richest and poorest areas in Malaysia is 2.8 times in 2022. However, by studying the time series of median household income for these two states since 1995, one can find that such an income gap has always been hovering around 3 times most of the time. The greatest disparity occurred in 1997 (3.5 times), while the smallest was in 2007 (2.4 times), (Table 1).

Not forgetting that the cost of living in Kuala Lumpur is much higher than the one in Kelantan, which could significantly affect one’s housing affordability. This is because the cost of living plays an important role in determining one’s financial eligibility for owning a house. Also acquiring a property requires most Malaysians to sign on a housing loan, but financing remains an issue for many as housing loan requirements are being tightened as a result of higher household debt. This is coupled with the growing construction cost faced by most developers, which could result in higher selling prices for houses; thus making housing affordability for KL-ites even more challenging.

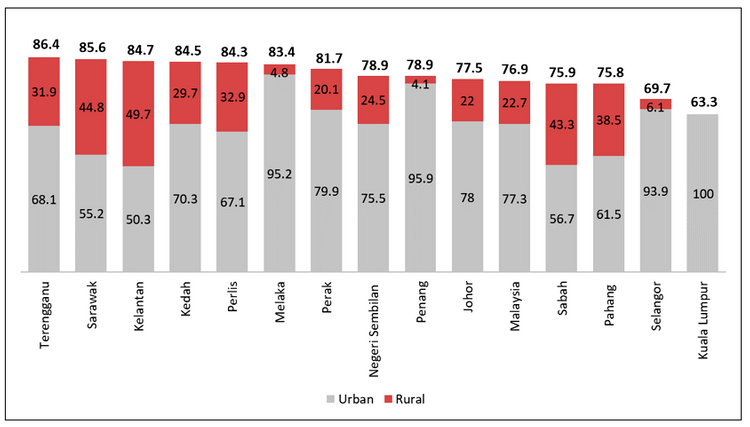

Check out properties for rentThis is indicated by a relatively lower homeownership rate in Kuala Lumpur (63.3%) as compared to other states (Figure 3). Though a higher homeownership rate in Kelantan could be due to the existence of informal housing in rural areas, it is also undeniable that a lower cost of living is somehow contributing to the state’s higher homeownership rate (84.7%). Unfortunately, the latest available data for homeownership rates is only up to 2019. The latest figure is not published in the HIS 2022 Report.

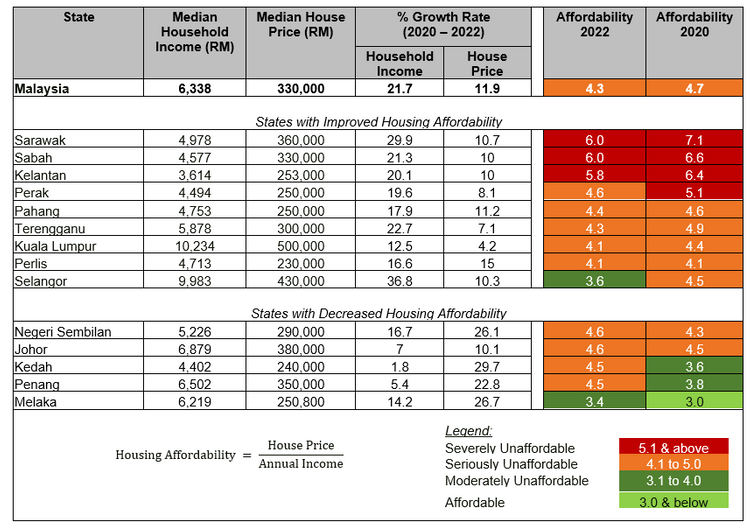

By using the median multiple (MM) approach, which is adopted by the National Affordable Housing Policy (DRMM) in assessing housing affordability in Malaysia – one can find that the country’s housing affordability improved from 4.7 in 2020 to 4.3 in 2022; due to the higher pace of income growth (21.7%) from RM5,209 in 2020 to RM6,338 in 2022, and the moderating house price growth (11.9%) from RM295,000 in 2020 to RM330,000 in 2022 (Table 2).

Most states have experienced improved housing affordability, with a higher income growth of at least 15% and a house price growth that capped around 10%. Some states like Sarawak, Sabah, Terengganu, and Kelantan have even recorded more than 20% growth in household income, compared to a slower increased house price; while states like Perlis and Pahang are experiencing a nearly in-tandem growth for both the household income and house prices. The best performers are Selangor and Perak, where the affordability level has improved from 4.5 (seriously unaffordable) and 5.1 (severely unaffordable), respectively, to 3.6 (moderately unaffordable) and 4.4 (seriously unaffordable).

Meanwhile, some states have recorded declining housing affordability. For example, both Penang and Kedah‘s housing affordability has decreased from “moderately unaffordable” to “seriously unaffordable” due mainly to slower household income growth less than 10%) and a higher pace of house price growth (more than 20%). In the case of Johor, Negeri Sembilan, and Melaka, the faster pace of house price growth compared to household income growth is resulting in a weaker housing affordability.

From here, one can see the weighty role played by income growth in influencing housing affordability. Since the supply side of our housing industry is still struggling with challenges that have yet to be addressed including material price hikes, cross-subsidisation, as well as high compliance and utility costs – there is little room for house prices to remain constant, much yet to decrease. However, it is also unlikely to see any house price boom in the near future, given that the country is still affected by the slowing global economy. As such, housing unaffordability is likely to continue for the B40 and M40 categories if wages and salaries do not catch up with the increasing prices of commodities.

To opt for a long-term solution to tackle housing unaffordability, the government should move away from an approach that simply aims to build more affordable houses. Instead, the emphasis must be on job creation, income growth, as well as helping industries and businesses to not only survive but to grow, and transform with changing times. These factors are all key drivers to spur the country’s economy. Besides, there is a need to have a more comprehensive wealth redistribution system with equal emphasis on initiatives aimed at enhancing income levels, particularly with regard to the disparity between the T20 and M40/B40 categories. Looking into the household income distribution, there were 1.58 million households (out of 7.2 million households) in the T20 income group that constituted 46.3% of total household income in Malaysia; while 3.16 million households in the B40 group constituted 16.1% of total household income (Figure 4).

Notably, the mean income of B40 households lies below its median income. This implies that income distribution within the B40 group was negatively skewed or skewed to the left of which a larger proportion of lower-income households had pulled down the mean income value. This situation was different for the M40 and T20 groups where the recorded mean income was above the median income – this indicates that income distribution was positively skewed or skewed to the right where households’ income mostly clustered towards the left side of the distribution and a small number of households have higher income resulting in the median income to be lower than the mean income.

As such, using finer classification bands could enable more accurate policy targeting within each income group. By targeting higher-income individuals and adopting a progressive income tax system, the government can ensure that those who have benefited disproportionately from economic growth contribute their fair share, thereby narrowing the income gap. This will not only help to improve people’s living as well as housing affordability but also foster social cohesion thereby providing a platform for sustained and inclusive development.

Read this article next: Homebuyers no longer have to pay loan documentation fees