|

Lifestyle Trend |

Description |

| Clean Lifers | Clean lifers are consumers that adopt clean-living or minimalist lifestyles. Clean Lifers prefer to stay in and relax rather than hit a nightclub. Having been sheltered by the family unit, they enjoy spending time with them. They would rather spend their money on experiences – such as weekends away, festivals and restaurants – where they are able to chat with friends, or healthier social alternatives, such as hosting fitness class parties. |

| Borrowers | Borrowers are a new generation of community-minded sharers, renters or subscribers that reject material goods but in favour of experiences and a freer lifestyle. They want more flexibility and freedom in their lives, less baggage, and living for the moment. This means not being tied to possessions – Borrowers want access rather than ownership, whether through sharing, swapping, renting or streaming. |

| Adaptive Entrepreneurs | As consumers are increasingly seeking flexibility in their lifestyles, they tend to have an entrepreneurial nature, shifting away from the “traditional” 9-to-5 career towards one that affords more freedom. The birth of Adaptive Entrepreneurs is directly linked to a change in millennials’ values – They want a lifestyle they can build themselves, aligns with their personal interests and passions, and is not just for potential financial gain. It is also observed that there’s a marked delay in larger life goals, such as owning a home or having children. |

| i-Designers | The shift in focus from possessions to experiences is changing purchasing patterns and driving buyers to connect with the product creation process. For some, merely to own is unrefined, but i-Designers, participating in creation, design and build, are seen as sophisticated connoisseurs. i-Designers want to exhibit their creativity. Instead of choosing something that is the same but different, they want to create something for themselves with which they personally connect. |

| Co-living | The co-Living trend has blossomed amongst Millennials in the residential space. It is a form of housing where residents share living space and a set of interests and values. The trend stems from hyper-urban hubs that have embraced the sharing economy as a lifestyle choice and it is driven by the rising cost of real estate in urban centers. In its most basic form, co-living sees people sharing spaces and mutual facilities to save money and inspire collaborative ideas. Co-living communities typically provide short-term accommodation and host various events for their inhabitants. |

We review the effects of the COVID outbreak on Malaysia’s property landscape based on historical data, provide a market outlook and share emerging real estate trends in the next decade.

COVID-19 has gone worldwide, and that is an unavoidable fact. As the number of positive cases continues to increase to new heights, it is expected to have a profound impact not only on tourism, services, and manufacturing industry; but also on the property industry. Analysis and forecast previously done with regard to the country’s property outlook in the coming years are deemed to be obsolete, as they had foreseen neither the virus outbreak nor the movement control order (MCO) and their resulting effects on the economy.

SEE WHAT OTHERS ARE READING:

🏦 Effect of Covid-19 on home loans.

🤔 Is now a good time to sell or buy a property?

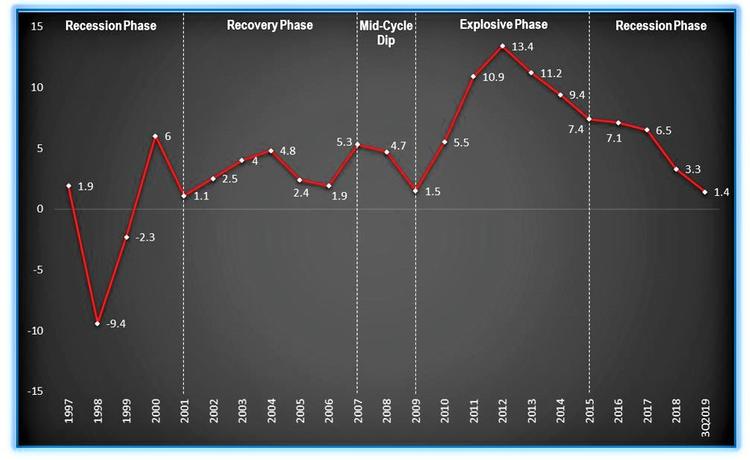

However, one should realise that the property market is cyclical in nature, with booms and bursts that follow the economic cycle: an “expansion” with upward pressure on house prices, followed by a downswing in house prices – “recession” – as the market hit the bottom of the cycle, and then with a “recovery” as the market builds towards the next boom. Against the backdrop of a cyclical scenario, economist Homer Hoyt first identified house prices crash for approximately every 18 years; and was then made famous by Fred Harrison, following the successful prediction of a house price crash between 2007 and 2008.

How was the property market supposed to fare without COVID-19?

By applying the 18-year property cycle principle in the Malaysian context (Figure 1), the country’s property market is found to enter into the recovery phase in 2001, after the 1997 Asian financial crisis. The mid-cycle dip took place during 2007-2009, in conjunction with the subprime mortgage crisis. Since then, the country’s property market embarked on the explosive phase. Prices started to escalate significantly from 2010 to 2015, with an increase as high as 13.4% per annum. The recession phase, then, kicked in after 2015, marked by the mismatch of house prices and affordability, overhang in properties, cautious consumer sentiment, difficult access to property financing, as well as the weakened ringgit against other major currencies.

If the 18-year principle is followed, the recession phase is supposedly due in 2019; and the property market should then embrace a phase of recovery in 2020. However, in light of the current uncertainties in both the national and global economies, it is generally perceived that the property market would remain soft in 2020. As a consequence, the following recovery phase will only start in 2021. Assuming that the recovery will last for another 7 years, based on the 18-year principle as well as experiences from the previous property cycle, the next explosive phase would likely kickstart in 2028.

Ongoing property overhang has caused challenges in property market

One should realise that the main cause of today’s sluggish property market is attributed to the country’s imbalanced housing supply-demand system, as identified in a previous assessment.

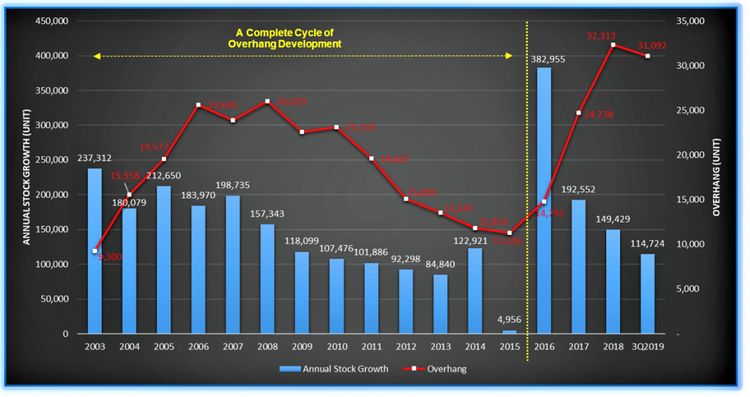

As shown in Figure 2, there are 382,955 units of houses added into the existing inventory stock in 2016, which is the highest since 2003 (237,312). Excessive supply of houses caused the drastic increase of overhangs in 2017 (24,738), and the residual impact is then carried forward to 2018. Further intensifying the housing market is the annual stock growth in 2017 and 2018, which is recorded as high as 192,552 units and 149,429 units, respectively.

Historical data suggests that whenever there is an excessive supply of houses in a particular year, the number of overhangs will surely increase in the following year (depicted in 2003-2008). Also, the number of overhangs will only come down if there is a reduction of supply in the consecutive years (depicted in 2010-2013). In this sense, a period of 12 years (2003-2015) is required in order to restore the number of overhangs back to its lowest level, which is from 9,300 units in 2003 to 11,316 units in 2015.

In view of the current rate of market absorption, one can expect that the housing market will remain challenging in the short- and medium-term, as the unprecedented large property overhang will take more time to be absorbed by the market before it could resume back to the level recorded in 2016 (14,792). It is likely that a complete overhang cycle will end in 2028, a twelve-year period from 2016. As such, either with or without the virus outbreak, lackluster years are ahead for the country’s property industry.

READ: BNM’s 6-month loan moratorium: What is it and how can it help you?

COVID-19 is amplifying existing issues in the housing market: Market sentiment will be low in the near to medium term

Even before the virus outbreak, developers have been sharing the same concern in regards to the mid-term market outlook: the market slowdown may prolong for another few more years due to the lack of incentives and stimulus packages for the property industry. This is reflected in the planned supply inventory.

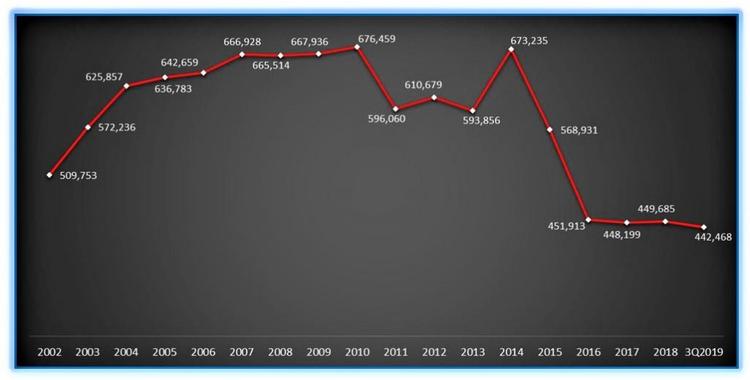

According to the National Property Information Centre (NAPIC), planned supply comprises units with building plan approvals received within the review quarter but have not started physical construction works. Since Malaysia is adopting the sell-then-build (STB) housing delivery system, where developers are able to lock in profits before the commencement of the projects, it is reasonable to assume that developers are more informed of future prospects in the market.

As of 3Q2019, residential housing across the country is set to see a planned supply of 442,468 units – which is the lowest recorded number since 2002 (509,753). In fact, planned supply has been reducing greatly since 2016 – as compared to 673,235 units in 2014 – and remained at the same level consecutively for the past four years, signalling a cautionable and conservative view on market sentiment among developers (Figure 3). In other words, regardless of the virus outbreak or not, market sentiment is deemed to be low in the near to medium term, especially after the expiry of the Home Ownership Campaign (HOC).

What is the short-term effect of COVID-19?

COVID-19 tends to worsen the market as people will temporarily move away from buying luxury and big-ticket items during tough times. Due to the lack of confidence about the near future, coupled with the uncertainty upon the duration of the business shutdown; potential buyers are likely to wait-and-see, leading to the reduction of average sales in the first half of 2020.

MORE: 9 Highlights from NAPIC’s Property Market Report 2019

What are the long-term effects of COVID-19?

While the short-term effect is immediately reflected in the drop of sales; the long-term impact of the COVID-19 outbreak is more profound, as it will affect consumers’ lifestyle, leading to the transformation of how they work, shop, and live; thereby changing the associated real estate requirements. For example, office-based businesses are expected to downsize, due to the emergence of flexible and remote working culture incubated during the period of movement restriction.

At the same time, the square footage of the retail sector, especially shopping malls will decrease accordingly due to the ever-changing buying patterns of consumers. With more and more consumers relying on smart devices within their daily lives, the demand for seamless and responsive services and products is rising. As a result, e-commerce offerings and home delivery services that function with lesser human contact will flourish in the future.

What will the future of Malaysia’s housing landscape look like?

It is worth noting that the epidemic is just an accelerator to the changes that have already kickstarted in the consumers’ lifestyle. A closer look at the last decade reveals that portability and connectivity of technology via smart devices have played a significant role in shaping and shifting consumers’ attitudes, values and buying behaviours.

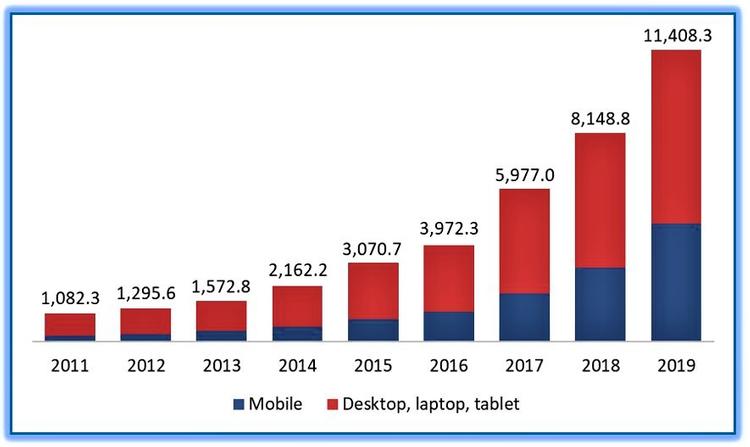

A typical example is the growth in internet retailing, where the total sales surged to RM11.4 billion in 2019 as compared to RM1.1 billion in 2011- an astounding quadraple growth in numbers (Figure 4).

The housing industry in the coming decade is sure to differ significantly from decades before, as consumers are rethinking how they live, how they spend their money, how they allocate their time, what importance they place on their immediate surroundings, as well as their engagement in issues that matter to them. There are, at least, five key consumers’ lifestyle trends at play in the present society that deemed to have potential impact on the country’s property landscape (Table 1): (i) clean lifers; (ii) borrowers; (iii) adaptive entrepreneurs; (iv) i-designers; and (v) co-living.

Table 1: Emerging consumers’ lifestyle trends that deemed to impact our housing industry. As depicted by Euromonitor International – the world’s leading provider for global business intelligence and strategic market analysis.

The emerging lifestyle trends point to the fact that consumers want and need less (Clean lifers). Ownership is under question as flexible and minimalist living is gaining popularity, with consumers sharing everything from clothing, household items, and even cars and living spaces (Borrowers & Co-living). Rejecting commitment also plays out in the workplace, as consumers say no to corporate 9-5 jobs; but preferring entrepreneurial lifestyles (Adaptive entrepreneurs). The desire for uniqueness is driving customisation to a new level, with consumers becoming the creators feeding into the design of products and becoming involved in the production process (i-Designers).

In this sense, future housing development should be tailored towards development that enables consumers to engage in experiences and share exciting stories and spaces with others. These types of development should be located strategically in areas where consumers are able to move conveniently from one place to another without hindrances, or interconnected with a public transportation network.

If you enjoyed this guide, check out this article next: Should you buy or rent a home?

TOP ARTICLES JUST FOR YOU:

🏗️ Property market lessons Malaysians can learn from Covid-19.

💵 What is refinancing and should I refinance?

💰 Flipping a house for profit in Malaysia: How to do it?

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.