With the reduction in the Overnight Policy Rate (OPR) by Bank Negara Malaysia (BNM) in July 2016, a growing number of local property purchasers are considering to take advantage of the consequent lower interest rates being offered by banks.

What is refinancing?

A mortgage is a unique financial product where the collateral (property) value appreciates over time, while your loan depreciates over time. In that vein, a property can then be used to generate additional cash flow for its owner, through mortgage refinancing. The process involves paying off an existing loan and replacing it with a new one.

Why do home buyers/property investors refinance?

Common reasons include:

(1) The opportunity to leverage on a current lower interest rate (IR) or effective lending rate (ELR) in order to reduce your remaining monthly instalments. As illustrated below:

(2) The chance to shorten the loan tenure down the road as the borrower gets more financially stable. Slashing down your tenure can result in significant savings:

(3) To leverage on a property’s capital appreciation by cashing out the amount of increase in property value after a few years. This gains can be used to finance other investments, fund your child’s education, pay off other debts or even serve as savings.

What are the costs involved?

a) MORTGAGE LOCK-IN PERIOD

Before you decide to pay off your existing loan early (before the tenure expires), make sure to check whether your existing loan has a lock-in period and if you are still bounded by it. Banks normally charge a penalty of 2-5% on your original loan amount if you fully pay off your mortgage within the first two to five years. This period is essentially known as the lock in period.

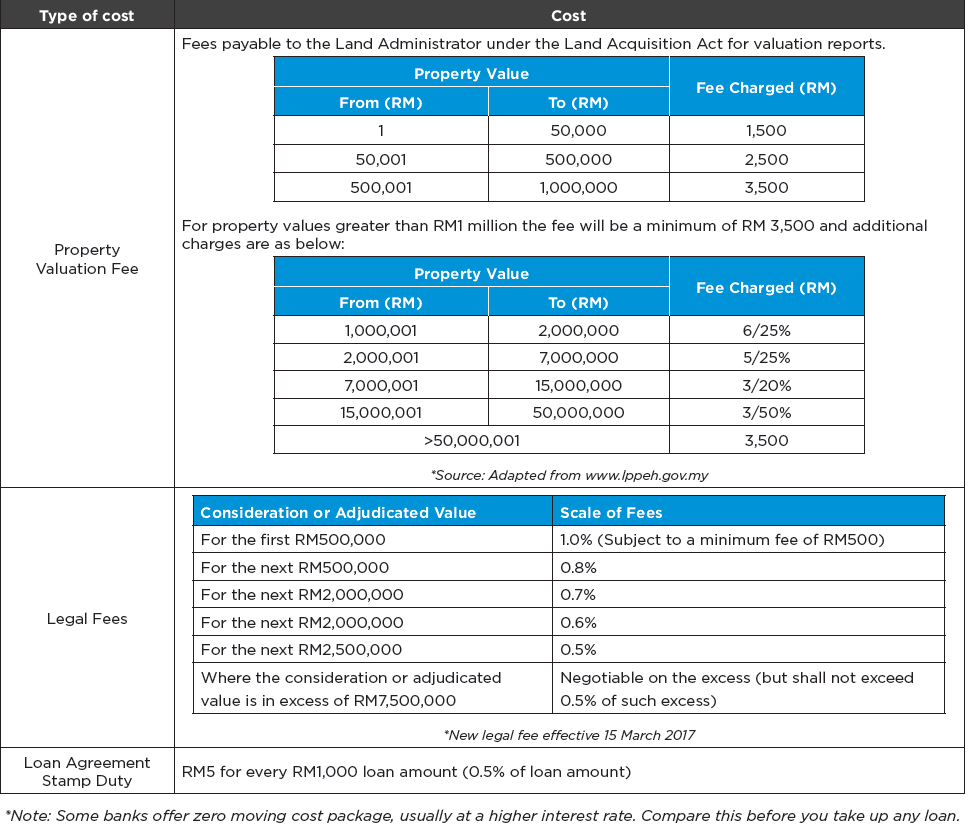

b) MOVING COST

This refers to the expenditures involved when signing up for a new loan, namely valuation fees, legal fees, disbursement and stamp duty. For those refinancing to save on interest rates, take note of the expenses involved and compare it against the total savings obtained through refinancing. If the figure obtained is positive, only then should you proceed to refinance.

What Are The Steps Involved?

The process is quite similar to applying for a brand new mortgage. The procedure includes:

(1) Go through your current mortgage agreement. Determine whether it is still within the lock-in period.

(2) Contact a few banks to find out more about the deals they are offering. Factors that have to be considered include the ELR, moving cost; whether there is zero moving cost or partial moving cost are absorbed, and if there is a lock-in period. Evaluate all these deals and determine which one best aligns with your objective for refinancing.

(3) Always negotiate for a better ELR if you are not in a hurry to cash out.

What are the other alternatives?

In lieu of refinancing, purchasers could opt for a top-up loan instead. It is an additional loan on top of the current mortgage’s outstanding amount. The loan will be calculated based on the property’s current market value.

Some banks may open a new account for the additional top-up while some banks may just top it up in the same account, which means there will only be one account to be serviced. Top-up loans can only be applied at the same bank from which you took your original loan from. Most banks will reapply similar terms and conditions of the existing mortgage.

PROS

• No need to redo the loan agreement.

• Minimal Fees.

• Shorter processing time as compared to refinancing.

CONS

• Unable to alter the details like ELR and loan tenure of the existing mortgage.

• May need to service or pay into two different accounts if the existing bank opens up a new account for top-up loan.

• The top-up amount might be limited because other banks may offer a higher bank valuation of the property