READ THE LATEST VERSION HERE: How to sell a house in Malaysia: A 14-step guide

Selling your home or any other property – especially if it’s your first time, can be a time consuming and exhausting affair. Here’s a quick start guide to getting the most profits out of your investment.

If purchasing a property or a house is the first big step in a person’s life, then selling it would be the second biggest. Thinking of upgrading or just looking to cash out? Whatever your reason for selling is, everyone in the property arena is looking at the same ultimate goal – reaping the benefits of capital appreciation on their property.

READ THE LATEST VERSION: How to sell a property fast in 14 steps?

It’s a very big decision to make and therefore, it is prudent to know the proper steps to take in order to reap the rewards you deserve. To sell off your first residential or commercial in Malaysia, there are certain processes and guidelines to be followed. Let us walk you through it.

1. Value your property

Before you are able to start selling, you must first appoint a certified appraiser to value your property. By identifying your property’s current market value through valuation, you will know how much your property is worth. However, take note that certain charges will apply for a home valuation, which is borne by the seller.

- First RM100,000 = 0.25%

- Next residue up to RM2 million = 0.2%

- Next residue up to RM7 million = 0.167%

- Next residue up to RM15 million = 0.125%

Thus, if your home is valued at RM800,000; you will have to fork out RM1,650 (0.25% X RM100k + 0.2% X RM700k).

READ: What is property valuation & the 4 factors which influence a home’s value?

2. Beautify your property

First impressions count, whether in a photo or a house visit. When taking photos to post in property advertising websites, ensure that the rooms and living areas are well lit. If possible, take the photos during the noon as that is when the lighting is best. Open all the curtains for better lighting.

Make sure that there is no clutter, and that your house is clean. Make sure you touch-up on damages and remove worn out articles such as dirty carpets, faulty doorknobs or falling wallpapers. Giving a fresh coat of paint and throwing away unnecessary items can help refresh a space almost immediately. All of these will count towards getting a higher selling price at the end of the day, so don’t underestimate the value of a good spruce-up.

3. Advertise your property

There are several ways to advertise your property for sale. You may do it traditionally by using the newspaper’s classifieds section, or the more tech-savvy method of employing property portals like iproperty.com.my. If listing on a property portal, do ensure that you have all the important and accurate details included in your listing.

You will want to include the property type, built-up, land area, number of bedrooms and bathrooms, store room if available, land title and tenure among others. If you are living in a high rise, make sure to include the number of parking lots you have, the facilities available, and the maintenance fees.

Those who prefer a hassle-free process can opt to employ real estate agents to do the job, but take note that agents normally charge a commission of 2-3% on the selling price.

4. Check for outstanding bills & prepare the related documents

Make sure to clear all outstanding fees applicable to the property, otherwise, there will be a delay in completing the sale. These include the quit rent (also commonly known as cukai pintu) or parcel rent (for strata buildings) – a form of land tax paid annually to the state, and the assessment tax – a local property tax for services provided by the local council.

The seller must also prepare a set of documents comprising of their IC, latest mortgage statement, a copy of the title to the property, copies of quit rent, assessment tax and renovation details (receipt, if any). Having all these ready would greatly ease the selling process.

5. Appoint a lawyer

Getting legal help is important in drafting your Sales & Purchase Agreement (SPA) and other legal matters. Having a lawyer on hand is definitely more assuring if anything that requires legal advice happens to crop up. For example, a lawyer can help in flagging any discrepancies in your SPA and bank loan agreement, in ways which only a legal professional can.

In the case of any dispute between you and the developer – for example in cases related to timing of documents submissions, delays, the accuracy of documents – a legal professional is a good resource to have. You will definitely need to fork out some legal fees here, but it’s always better to be safe than sorry.

6. Acceptance of offer

Let the viewings begin! You will soon get phone calls from prospective buyers to view your property. With any luck, you will be able to lock-in a serious buyer after a few rounds.

Once you and your buyer have agreed to a price, you will need to ask your buyer to pay an earnest deposit of 2-3% and sign the Letter of Offer. Your lawyer will then proceed to prepare the SPA for your buyer to sign. This is usually done within 2-3 weeks after the Letter of Offer is signed.

When the buyer signs the SPA, they will need to pay the remaining 10% amount of the deposit to you. The remaining 90% will be paid to you through bank when the buyer settles their financing, normally within 3 months.

7. Finalisation & Taxation

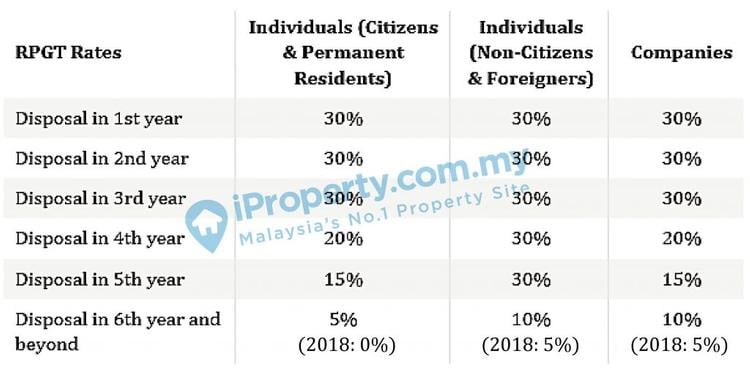

Once everything has been finalised, the house will be fully transferred to the new buyer and you will be disposed of your property. If you are disposing off your first private residential property, you will be given a once-in-a-lifetime exemption of paying Real Property Gains Tax (RPGT).

If this is not your first property, you will have to pay RPGT as per the tax bracket below – these new rates are as announced during Budget 2019. Previously, Malaysian homeowners who sell off their properties after the 5th year of ownership are not required to pay any RPGT on the profits earned from the sale:

However, during the recent Budget 2020, an RPGT amendment was made to provide some relief to property sellers. It was announced that for the calculation of property gain tax of units purchased before 2013, the Government will use the market price on 1st January 2013 as the initial point of valuation. Previously, the base year was set at 1 January 2000. As RPGT is charged on the profit made from the sale, a later base year would mean a lower calculated profit, automatically reducing the amount of property tax the seller has to pay.

MORE: What is RPGT in Malaysia & How to calculate it?

8. Loan Disbursement

The buyer’s bank will disburse loan money in 2 stages. The first stage is the redemption stage where the buyer’s bank will disburse money to the seller’s bank to redeem the property from the seller’s bank. This is sometimes referred to as the redemption amount.

After that, the seller’s bank will release all documents such as the original title and original purchase agreement to the buyer’s lawyer. The buyer’s lawyer can now register the title under the new buyer’s name and create the mortgage over the property. The second stage of loan disbursement will happen after the documents are released to the buyer’s side.

Now that you know what the process of selling off your first property is like, you can look forward to unloading it with minimal fuss. Just remember that this is a basic guide and always be prepared for any unforeseen circumstances and always do your due diligence before selling. Most importantly, set aside some budget for an agent and lawyer to guide you through, especially if it’s your first time.

If you enjoyed this guide, read My tenant is not paying rent. What can I do as a landlord?

Edited by Reena Kaur Bhatt