Purchasing a home also means applying for financing or mortgage. We all know that. However, for the more financially savvy, choosing the right home loan is also a crucial step. Below is how you can do the same!

Not all home financing are equal. They all have different benefits. Some may share the same features, but the best ones will suit your own unique financial needs. Buying property can potentially be your biggest investment, so you must select one that provides you with the most gains. Here’s what you need to consider.

→ Navigate Covid-19: Property knowledge, stay at home articles and tools. Get started now.

1. Types of loans you can apply for

Due to the Movement Control Order (MCO), Bank Negara Malaysia (BNM) has ordered all banks in Malaysia to grant an automatic six-month moratorium on loan and financing repayments effective April 1, 2020. New applications are still being carried out, albeit with slower processing time.

The first criteria for you to consider is whether to opt for conventional or Islamic financing. In a nutshell, here are the differences:

-

Conventional home loan

Lenders lend to borrowers to make a profit from the interest charged on the principal amount. Borrowers pay interest on the outstanding principal amount. This can be based on a fixed or floating rate.

Avoids interest-based transactions (riba). Instead, it introduces the concept of buying something on the borrower’s behalf and selling it back to the borrower at profit. In place of interest, a profit rate is defined in the contract which can be fixed or based on a floating rate.

Home loans or mortgage also can be divided into three main categories:

-

Fixed loan

Also known as a Term Loan or Basic Term Loan. It comes with a fixed repayment schedule. The monthly instalment you pay is the same throughout your entire loan period.

-

Semi- flexi loan

Enables borrowers to make advance payments. This is to lower their loan interest without the need to make any formal request to the bank.

Enables borrowers to make advance payments to lower their property loan interest and withdraw the additional payments they’ve made whenever they like.

There is also the Government Housing Loan for civil servants and some banks even offer renovation loans for the specific purpose of refurbishing a property.

READ: How many types of home loans are there in Malaysia?

2. How the latest OPR, BR, and moratorium affect your home loan?

An Overnight Policy Rate (OPR) is the interest rate at which a bank lends to another bank. It is set by BNM and is an indicator of the health of a country’s overall economy and banking system.

A Base Rate (BR) is an interest rate that the bank refers to before it decides on the interest rate to apply to your home loan. It is derived internally by the bank based on how much it will cost the bank to lend you the money. It also takes into account a minimum interest rate set by BNM.

With the economic impact of the COVID-19 pandemic and MCO, BNM announced the reduction of the OPR by 50 basis points to 2% on May 5. It was the third reduction this year and the lowest OPR since 2010. And the latest (July 7), BNM reduced the OPR by another 25 basis points to 1.75%, a record low since the floor was set in 2004.

In line with this cut, several banks have announced that their BRs will also be reduced. As a home buyer, this is good news. The reduction in OPR and BR will lead to a lower mortgage interest rate, and consequently lower monthly payments. Existing borrowers will also benefit from lower monthly payments and shorter loan tenures.

3. What are the new lending rates of Malaysian banks?

Effective May 13, CIMB Bank Bhd and CIMB Islamic Bank Bhd cut their BR by 0.5%. Similarly, all financing activities based on its BLR (Base Lending Rate) and BFR (Base Financing Rate) will also be reduced by 0.5%. According to CIMB’s website, its BR is currently 3.5% while its BLR and BFR are currently 6.35%.

Separately, Maybank announced that it will be reducing its BR and BLR by 50bps to 2%, from 2.50% per annum, while its BLR will also be lowered to 5.65% per annum from 6.15% per annum. This took effect on May 8.

4. Things you need to consider when applying for a home loan

As we mentioned earlier, the best home loan will need to suit your own unique financial needs. You need to consider the following:

-

Total cost

Calculate your monthly payments to see how the loan fits into your budget. Look at your savings and determine how much you can afford for a down payment. The bigger the down payment, the smaller your housing loan will be. This can save you a lot of money in interest charges. You will also need to look at the annual percentage rate (APR). This will be in the form of interest (for conventional loans) or profit rate (for Shariah-compliant financing). Some lenders might charge additional fees, so make sure you are aware of this.

-

The length of financing

A longer loan tenure will have lower monthly payments but a higher APR. If your housing loan tenure extends into your retirement age, you should have a plan on how to service your repayments after you retire.

-

When do you need it?

If you require fast approval, some lenders specialise in fast funding.

-

Compare home refinance loans between banks

Further down the line, you may want to refinance your property. The benefits of doing so include lower interest rate/Effective Lending Rate (ELR), shortened mortgage tenure, cash out to finance a new purchase, debt consolidation, and changing to a different mortgage type.

-

Ask for a Product Disclosure Sheet (PDS)

Use the PDS to compare the effective lending rate, monthly instalment, total repayment amount, lock-in-period, early settlement penalty, and charges. It will also tell you how a rise in the interest rate affects your monthly instalments and the total repayment amount over the life of your loan.

-

The fine print in documents

There is always the risk of something getting lost in the fine print. Make sure you lookout for the introductory rates, lender mortgage insurance (LMI), restrictions on additional payments and other features.

READ: What is Real Property Gains Tax (RPGT) in Malaysia & How to calculate it?

5. What are my approval chances?

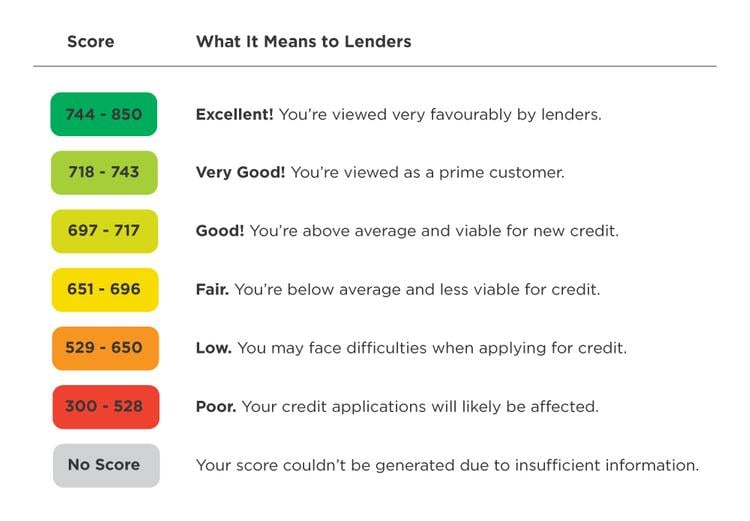

Approval of a financing application will mainly depend on your Credit Score and Debt Service Ratio (DSR). Financial institutions use the two to evaluate your creditworthiness. A credit score indicates a consumer’s credit risk. A good credit score can increase your chances of getting a loan, better interest rates and speedier loan approval, among other things.

In Malaysia, financial institutions may use internal methods to evaluate your credit score. However, to assist them in this evaluation, many will refer to two popular credit reports:

-

Central Credit Reference Information System (CCRIS)

CCRIS is managed by the Credit Bureau of BNM. It gathers credit information from multiple financial service providers in Malaysia. These include banks, insurance brokers and even private companies providing utility services such as Malaysian telecommunication companies.

-

Credit Tip-Off Service (CTOS)

The CTOS Data Systems Sdn Bhd (CTOS) is one of Malaysia’s leading Credit Reporting Agency (CRA). It is a privately owned agency that archives an individual or a company’s entire credit history. A CTOS score is calculated based on credit information from both CCRIS and CTOS’s database. It ranges from 300 to 850.

DSR is a calculation used by the bank to check whether you can repay the loan. Your DSR is usually compared against the bank’s maximum allowable DSR limit. In general, the formula used to calculate an individual’s DSR is the net income (after tax and EPF deduction, etc.) divided by the total monthly commitments including the home loan you’re applying for.

6. Will the moratorium affect my credit score?

Payments deferred under the moratorium will not affect your credit score or ability to borrow loans at a later stage. Deferred payments will not be reflected as defaulted payments.

7. The danger of multiple submissions

Most banks and financial institutions keep track of the number of times you apply for financing, and more importantly, the number of rejected applications. Applying for several financing packages is often perceived as desperation, which doesn’t bode well for your loan approval.

Find out more about the dangers of multiple loan submissions for property financing here.

8. If my loan is rejected by a financial institution, will others do the same?

Each bank or lender has its risk appetite, business policies and strategies. Therefore, an application rejected by one may be accepted by another. However, undischarged bankrupts and wound-up companies will unlikely get loan approval regardless of which financial institutions they approach.

READ: What can you do after your home loan gets rejected?

Buying a home is a long-term commitment and potentially one of the biggest investments of our lives. Therefore, selecting the best home financing that suits your financial capabilities and needs is a major decision. The right planning and considerations will help you arrive at the best decision.

Edited by Rebecca Hani Romeli