Following numerous complaints from the rakyat about rising living costs, the Employees Provident Fund (EPF) has decided to restructure its members’ accounts to provide a certain level of flexibility to withdraw their savings at any time.

According to EPF, effective May 11, the restructuring seeks to enhance members’ income security after retirement while addressing their current life cycle needs.

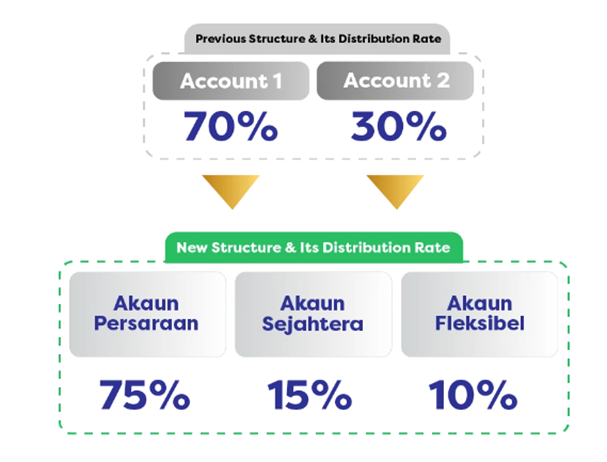

The move, which involved introducing three accounts, aimed to bolster income security post-retirement while addressing immediate needs. The three accounts announced are Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel.

Akaun Persaraan, previously known as Account 1, would serve as a repository for savings aimed at retirement; Akaun Sejahtera, previously known as Account 2, is designed to cater to various life cycle needs; and Akaun Fleksibel, as the name suggests, would provide flexibility for short-term financial needs, whereby savings in this account can be withdrawn at any time.

EPF Chief Executive Officer Ahmad Zulqarnain Onn said the EPF Account Restructuring initiative aims to empower members to make decisions about balancing their future needs for retirement between short-, medium—and long-term financial needs.

“This initiative will also help increase members’ retirement savings so that they will have sufficient retirement income to sustain their needs after retirement,” he said.

The restructuring will apply to all EPF members under the age of 55, including non-Malaysians, and once they reach 55 years old, any remaining savings across their three accounts will be transferred to Akaun 55, with any subsequent contributions credited to Akaun Emas.

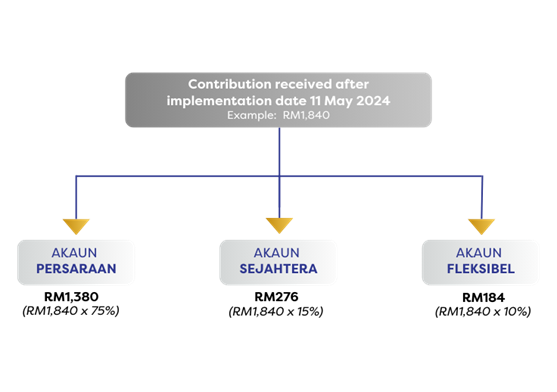

The allocation in the account will be 75%, 15% and 10% into Akaun Persaraan, Akaun Sejahtera and Akaun Fleksibel, respectively. New contributions will be credited into Akaun Fleksibel.

Members will have a one-time option to transfer part of the balance of their Akaun Sejahtera savings as an initial amount into Akaun Fleksibel from May 11 and August 31, and no transfer will be made if the member does not choose to opt-in for an initial amount.

Are There Any Differences Among the Accounts?

One of the most common initial concerns is the dividend rate that will be applied to all three accounts. EPF confirms that the account restructuring does not change the existing policy on establishing dividend rates.

The distribution rate for these three accounts will be 75% for Akaun Persaraan, 15% for Akaun Sejahtera and 10% for Akaun Fleksibel.

If members have not chosen to transfer part of their savings into Akaun Fleksibel, it starts from zero, and 10% of the contributions made after that will go into the account.

Members can also transfer from Akaun Fleksibel to Akaun Persaraan and Akaun Sejahtera. However, this decision can not be redone.

How Can I Contribute To Account 3?

The new contributions will be credited into the three accounts as it continues, as according to the distribution rate.

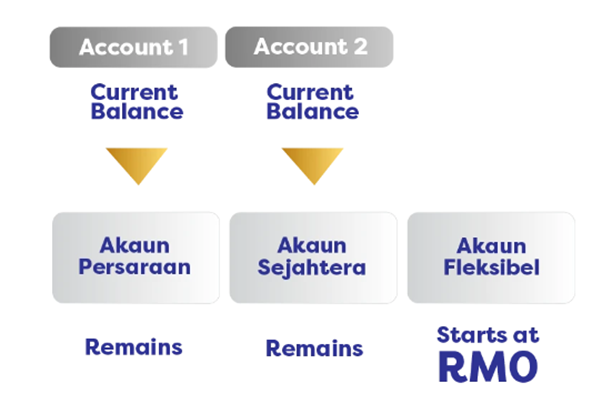

Since the implementation on May 11, members can log in to their EPF account and see that the balances in Account 1 and Account 2 would have remained in Akaun Persaraan and Akaun Sejahtera, respectively, while Akaun Fleksibel started with a zero balance.

Contributions made after the implementation would be distributed accordingly.

Can I Withdraw From Akaun Fleksibel?

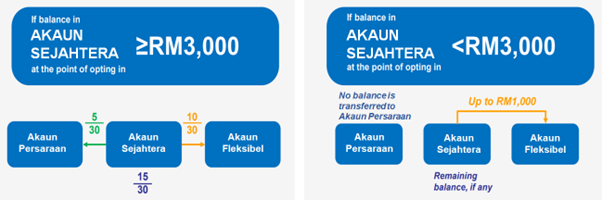

The one-time option to transfer part of the savings into Akaun Fleksibel could not be cancelled after application. The initial amount credited to Akaun Fleksibel would have depended on whether the balance in Akaun Sejahtera is below or above RM3,000.

If the balance in Akaun Sejahtera is RM3,000 and above, transfers would be:

- Ten out of thirty (10/30) of the balance in Akaun Sejahtera transferred to Akaun Fleksibel;

- Five out of thirty (5/30) of the balance in Akaun Sejahtera transferred to Akaun Persaraan; and

- Fifteen out of thirty (15/30) retained in Akaun Sejahtera

If the balance in Akaun Sejahtera is below RM3,000:

- All amount transferred to Akaun Fleksibel if the balance is RM1,000 and below.

- RM1,000 transferred to Akaun Fleksibel if the balance is more than RM1,000 and less than RM3,000.

- No distribution will be made to Akaun Persaraan for savings balance below RM3,000.

To initiate this one-off transfer, members can apply through the KWSP i-Akaun app, or may visit any EPF offices to apply through the Self-Service Terminals (SST) starting from May 12.

Once processed, the funds will be disbursed directly into the registered bank account. The minimum withdrawal amount is RM50. No documents are required for submission.

Investing From Akaun Fleksibel Withdrawal

As the initiative is still in its initial stage, there are no specific investment schemes, such as the Members Investment Scheme (MIS), for balance or withdrawals from Akaun Fleksibel.

The MIS allow eligible members to transfer part of their funds from Akaun Persaraan to EPF-approved unit trust funds for investment purposes. It can be done online via the EPF i-Invest option in the i-Akaun platform.

In terms of other types of investments, experts opine that the impact of the withdrawal would be minimal as it is only expected to boost domestic consumption.

According to Dr Paul Anthony Mariadas and Dr Uma Murthy from the Faculty of Business and Law of Taylor’s University, there is a potential for some members to consider alternative investment options instead of keeping their funds within the EPF.

They were reported saying that this perspective implies that withdrawing funds and investing them elsewhere may offer the potential for higher returns.

However, they said, it is important to note that opting for alternative investments may expose individuals to elevated levels of risk, potentially endangering their retirement savings if these investments fail to meet expectations or suffer losses.

What Happens To Akaun Fleksibel Savings After Retirement?

It has been established that restructuring EPF accounts does not impact EPF members above the age of 55.

For other members, once they reach the age of 55, the practice would be similar, where all savings in Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel will be merged into Akaun 55. Any subsequent contributions would be credited to Akaun Emas.

Zulqarnain said that the initiative is not just EPF’s response to current needs, but is a proactive step to help members facing the changing job landscape and demographics of the population and the needs of EPF members.

“With these enhancements, the EPF strives to ensure that every EPF members can manage their finances with confidence and resilience in this dynamic and challenging environment.”