| (Latest) Nov 2023 | 3.00% |

| May 2023 | 3.00% |

| March 2023 | 2.75% |

| January 2023 | 2.75% |

| November 2022 | 2.75% |

| September 2022 | 2.50% |

| July 2022 | 2.25% |

| May 2022 | 2.00% |

| July 2020 | 1.75% |

| May 2020 | 2.00% |

| March 2020 | 2.50% |

| January 2020 | 2.75% |

| November 2019 | 3.00% |

Bank Negara Malaysia (BNM) has increased the Overnight Policy Rate (OPR) by 25 basis points from 2.75% to 3% on 3 May 2023. As of November 2023, the OPR remains at 3.00%. Let’s take a look at how this will affect your home loan.

What is OPR Malaysia?

The Overnight Policy Rate (OPR) is set by our central bank, Bank Negara Malaysia (BNM). It is a rate a borrower bank has to pay to a lending bank for the funds borrowed.

A lower OPR creates the domino effect of lower interest rates – this is meant to encourage consumer spending and spur borrowing activities which in turn, will stimulate the domestic economy.

A higher OPR, on the other hand, will translate into a higher interest rate and make the borrowing cost expensive for borrowers such as home buyers and businesses.

Why did BNM reduce the OPR in 2020 and increase it in 2022, and maintained it in 2023?

Malaysia’s Overnight Policy Rate was maintained at a historical low of 1.75% since it was reduced from 3% in 2020 due to the Covid-19 outbreak, until BNM increase it to 2% on 11 May 2022, 2.25% on 6 July 2022, and 2.50% on 8 September 2022.

It was increased to 2.75% on 3 November 2022, and starting May 2023 it was increased to 3.0% and retained till now, November 2023.

The 1.75% was the lowest OPR on record, according to BNM data that dates back to 2004 on its website.

Changes In OPR Malaysia

- On 22 January 2020, the Monetary Policy Committee of BNM in a surprise move announced that it is slashing the OPR by 25 basis points (bps) to 2.75%, quoting that “the adjustment to the OPR is a pre-emptive measure to secure the improving economic growth trajectory amid price stability”.

- BNM announced yet another OPR cut on 3 March 2020 – by another 25 basis points to 2.5%

- On 5 May 2020 – just two months after the second reduction – the OPR was further reduced to 2% to encourage borrowing amid the Covid-19 pandemic.

- On 7 July 2020, the OPR cut was slashed by 25 basis points to 1.75% which goes to show how real the impact of Covid-19 is on the Malaysian economy.

- On 11 May 2022, BNM decided to increase the OPR by 25 bps to 2%, citing “the sustained reopening of the global economy and the improvement in labour market conditions continue to support the recovery of economic activity”.

- On 6 July 2022, the OPR was increased by 25 bps from 2% to 2.25% as the reopening of the global economy and the improvement in Malaysia’s labour market conditions continue to support the recovery of economic activity in the country, according to BNM.

- The OPR was increased by BNM for the third time in 2022, from 2.25% to 2.50% on 8 September 2022. According to BNM’s statement, the OPR hike was on the back of the stronger growth performance of the Malaysian economy in the second quarter of 2022.

- On 3 November 2022, the OPR was increased by BNM for the fourth time in the year, from 2.50% to 2.75%. According to BNM’s statement, the Monetary Policy Committee of the central bank has decided to further adjust the degree of monetary accommodation against the backdrop of continued positive growth prospects for the Malaysian economy.

Why Interest Rates Are Increasing When Cost Of Living Is Rising In Malaysia?

According to BNM, It is important to have the right policy at the right time.

- If BNM keep the OPR too low for too long when the economy is steadily recovering for example, it could cause too much spending and borrowing, which pushes prices up.

- Today, the economy is no longer in crisis. Hence, BNM started adjusting the OPR gradually since the health of the economy has improved. Just like doctors, BNM has to adjust the dosage of the medicine based on the condition of the patient.

- BNM also want to avoid the case where prices keep rising at a fast pace for many items. This is worse when higher prices lead to higher wages, which then lead to higher prices again.

- Higher interest rates help to break this cycle. If BNM waits until high inflation becomes out of control before they act, it would lead to worse outcomes. By then, BNM would need to increase the OPR faster and by much more. This would harm households and businesses more, especially when it goes hand in hand with high inflation which would hurt everyone’s purchasing power and plunge the economy into a recession. So, it is important for Malaysia’s monetary policy to act early to prevent this from happening in the future.

How does the OPR affect home loans?

When it comes to home loan products, the OPR has a direct influence on a bank’s Base Rate (BR) and Base Lending Rate (BLR) as well as the Standardised Base Rate (SBR), where the BR, BLR and SBR usually reduces or increases in tandem to an OPR cut/hike.

What happened if BNM reduces OPR?

With the OPR cut, it will be cheaper for new property purchasers to take up a home loan product as they could leverage on the lower initial interest rate.

When the OPR was reduced by 25 basis points to 3% in May 2019, it had an immediate effect – According to the Ministry of Finance, loan approvals in May 2019 soared by 13%.

This is because, with a lower OPR, there is a reduction in the effective lending rate (ELR) of existing home loans which are using a variable or floating rate.

In other words, existing borrowers will benefit from either:

1) Lower monthly instalment payments. Banks are required to send out a notification letter on the revised instalment amount when there is a BR/BLR revision – this must be done at least 7 calendar days prior to the date the revised monthly instalment comes into effect.

2) A shorter loan tenure (if the old monthly instalment sum is maintained). Even though by default, banks are required to lower the monthly instalment of variable home loans accordingly, they will still provide consumers with the option to shorten their loan tenure instead.

Do note that current borrowers who have taken up a fixed deposit rate home loan will not see any changes in their monthly instalment payments.

What happens when OPR increases?

When BNM raises OPR, however, banks’ interest rates will be revised upward accordingly and thus making it expensive for consumers to get a loan.

In a nutshell, a higher OPR will:

1) Increase monthly instalment payments. Whenever the OPR goes up, banks will pass on the higher borrowing cost in the form of a higher interest rate to consumers, which in turn increases the amount of your monthly instalment payments.

A 0.25% increase in OPR for a RM500,000 home loan with a 30-year tenure is likely to increase the monthly instalment payment by RM71.

This means that the borrower will have to pay an additional RM25,560 in total for interest payments in that 30-year period.

2) Loan tenure will increase if the monthly instalment amount is maintained. If the old monthly instalment sum is maintained, the repayment period will become longer due to the increase in interest rate.

For example, if you have a 30-year housing loan of RM500,000 at an interest rate of 3.83%, the monthly instalment will be RM2367.

When the OPR is increased by 0.25% and as soon as the bank’s interest rate is increased to 4.18%, the repayment period of your home loan will increase by 2 years to 32 years if you choose to keep the monthly instalment amount at RM2,367.

What are the latest lending rates of Malaysian banks?

Most of the major banks in Malaysia have reduced their Base Lending Rate (BLR) and Base Rate (BR) in tandem with the OPR reduction to 1.75% in 2020. These include Maybank, Alliance Bank, RHB Bank Bhd, CIMB Bank Bhd and OCBC Bank, as shown below.

But in view of the recent OPR hike, it is anticipated that banks will be increasing their Standardised Base Rate (SBR), BLR and BR by 25 bps in the next few weeks.

The SBR is a new Reference Rate Framework that was introduced by BNM to replace the BR for new retail floating-rate loans in Malaysia, such as housing loans and personal loans, starting 1 August 2022.

Housing loans and personal loans approved before 1 August 2022 and after 2 January 2015 will still be priced against the BR, while loans approved before 2 January 2015 will be priced against the BLR.

The SBR is meant to replace the BR, a reference rate that was introduced on 2 January 2015. The BR itself was introduced to replace another reference rate, the BLR.

Under the previous reference rate framework, each bank is allowed to set its own BR. This means that every bank has a different BR.

When the new SBR framework kicks in, however, the banks will all use a single rate – the SBR. As the SBR will be the same for each bank, it will be easier for consumers to compare the different loan packages offered by banks.

| BANK | SBR | BR | BLR | Indicative Effective Lending Rate |

| Affin Bank | 2.50% | 3.45% | 6.31% | 4.05% |

| Alliance Bank | 2.50% | 3.32% | 6.17% | 3.86% |

| CIMB | 2.50% | 3.50% | 6.35% | 4.25% |

| Maybank | 2.50% | 2.50% | 6.15% | 3.75% |

| Public Bank | 2.50% | 3.02% | 6.22% | TBC |

| RHB Bank | 2.50% | 3.25% | 6.20% | TBC |

*As of 12 September 2022. For the latest SBR, please refer to this article.

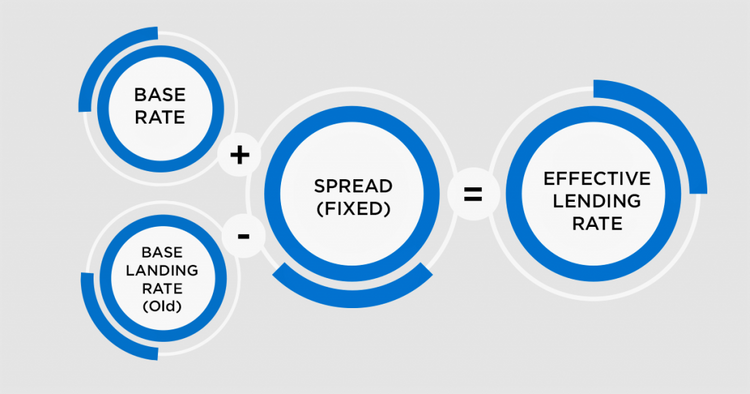

What is equally important, aside from the SBR, BR and BLR, is the spread that the bank charges. This spread here would be the bank’s profit margin. Spread as the banks call it, is always fixed.

Take BR as an example, by adding the BR with the individual bank’s spread (profit margin), you will get the effective lending rate (ELR).

For instance: 3.5% (BR) + 1.3% (Spread) = 4.8% (Effective Lending Rate)

*Effective 2 January 2015, the Base Rate (BR) replaced the Base Lending Rate (BLR). This change was made for several reasons – The BLR lacks transparency, which makes it difficult for consumers to make an informed decision. Comparatively, the BR system forces banks to disclose their profits margin (spread rate) while encouraging healthy competition between the banks. Ultimately, it benefits consumers as banks will now have to set their BR based on their individual efficiencies.

You cannot negotiate with the bank on the interest rates (BR or BLR) but you can negotiate on the spread. Getting the best possible rate depends on your negotiation power. However, your negotiation power depends on your risk level.

If the bank determines you as a high-risk individual (bad credit, low income or poor employment histories), it may be more difficult for you to negotiate. You will be considered lucky to even have the bank approve your loan.

A medium-risk individual may have a fighting chance, but the outcome is 50-50.

On the other hand, if you are a very low-risk individual (meaning you have a very good credit rating), you can appeal for a lower spread. Why? Because the bank would rather give you a lower interest rate than to lose you to other competitor banks.

MORE: What is the impact of COVID-19 on Malaysia’s property market?

Whether you are low, medium or high-risk individual, it really depends on whether you do any financial planning. Proper planning will be able to lower your risk level, thus giving you more negotiating power.

If you are thinking about buying a home, do ensure that you are ready for such a purchase. Use our home loan eligibility tool, LoanCare to find out if you will be able to secure a home loan for that property you have your eye on.

Edited by Reena Kaur Bhatt

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.