| Year | KLCI Property Index | Property Index relative to 2007 |

| 2007 | 954 | 954/954 = 1.00 |

| 2008 | 530 | 530/954 = 056 |

| 2009 | 781 | 781/954 = 0.82 |

Bursa REITs, property stocks, and property are all investments in real estate. This article looks at factors to consider when deciding which one (or ones) to choose.

A Real Estate Investment Trust (REIT) is a corporation that owns, operates, or finances income-producing real estate or real estate-related assets. REITs pool the capital of numerous investors.

According to Bursa Malaysia, real estate is a key asset class in an investment portfolio. Before REITs were introduced, investors had to choose between property stocks or actual property to get exposure in the real estate sector. With REITs, investors now have an alternative.

If you are a long-term investor in real estate, how do you choose between REITs, property stocks, and physical properties? I define a long-term investor as someone with at least 10 years of the investment horizon. This is to differentiate an investor from property “flippers” and stock traders.

I view investment from a retail investor perspective. In practice, this means limited capital for investing. I also view it from an investment perspective – In other words, I am buying a physical property not for my own use.

Evidence suggests that REITs provide the best returns among these three investment types in the Malaysian context. Should you go and buy the REITs then? Well, read my disclaimer.

Comparing the investments

While there are many articles that compare these three investments, very few look at them collectively. Most pit one against the other, such as:

- REITs vs property stocks

- REITs vs physical properties

- Property stocks vs physical properties

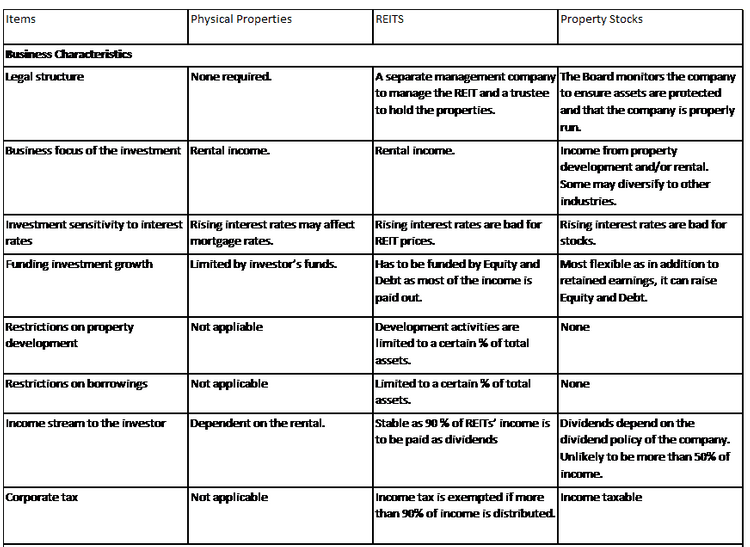

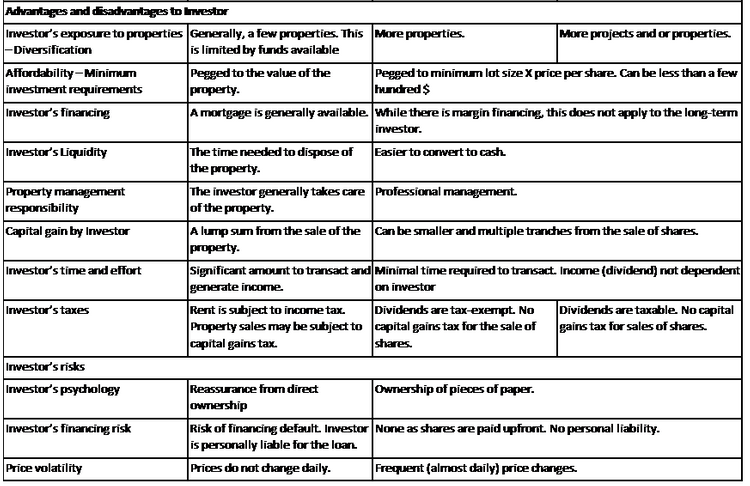

If you are going to choose, I think it is more appropriate to look at them collectively. In Table 1, I compare the three under the following characteristics:

- Business characteristics

- Advantages and disadvantages to the investor

- Risks to the investor

You can see that as a stock market instrument, a REIT shares many of the characteristics of a stock. Investing in physical properties is very different from investing in REITs or property stocks.

Which property investments are right for you?

I am a firm believer that to make money from your investments, you need to develop the appropriate investing skills. The skills for investing in physical properties are different from those required for the stock market.

If you are going to invest directly in properties, you should develop the following traits and knowledge:

- Understand cash flow

- Understand property market conditions and risks as well as tenant behaviours and demands

- Patience and persistence

- Good negotiation skills

On the other hand, if you are going to invest in REITs or property stocks, I recommend that you approach it as a value investor. This requires you to be able to analyse and evaluate companies.

Assuming that you have the appropriate skills, how do you decide between REITs, property stocks, and physical properties? I recommend evaluating the following:

- Potential returns and risks

- Funding requirements

- Ease of investments

Leaving aside the returns, I have matched the three investments to the traits required of you as an investor:

Physical properties

- You can afford the upfront and ongoing costs.

- You don’t mind managing your property.

- You prefer direct control over your properties.

- You want to take advantage of leverage.

REITs

- You have limited capital.

- You don’t want the hassle of buying and managing a physical property and prefer the convenience of investments.

- You are looking for a steady income stream.

- You want to hold a diverse portfolio of real estate.

Property stocks

- You have limited capital.

- You prefer convenience when it comes to investments.

- You not only want to hold a diverse portfolio of real estate but also want exposure to property development activities.

- You are looking for total returns (capital gains + dividends).

In many cases, it is not an either/or choice. Many investors own a condo to rent out while also owning REITs. Personally, I own physical properties along with shares in REITs and property stocks. REITs and property stocks are more convenient. I do not like to deal with tenants; I have had a few tenants from hell who messed up the house, forcing me to evict them.

From an asset allocation perspective, I have an equal amount invested in each investment type.

I own REITs for the dividend income while focusing on capital gain from my property stocks.

While I have rental income from the physical properties, the Malaysian rental yields tend to be low. So, I focus on capital gains. Over the past few decades, I have sold some of the properties and reinvested in new ones. I do not consider myself a property flipper as I hold onto the properties for at least five to six years before selling them.

➡️Find out Which REIT to invest in on Bursa Malaysia?

1. Historical returns

According to private financial and investing advice company, The Motley Fool:

- Over the past 45 years, the FTSE Nareit Composite Index achieved a compounded annual average total return of 11.4%. That was only slightly less than the S&P 500’s return of 11.5% per year during the same period.

- One reason REITs have generated solid total returns over the long term is that most pay attractive dividends. For example, as of mid-2021, the average REIT dividend yield was more than double that of stocks in the S&P 500.

The view is supported by business magazine, Forbes:

From 1977 to 2010, REITs have returned more than 12% annually. This is in comparison to the roughly 10% return of the S&P 500 and the 6% to 8% return of private real estate funds during the same period. And over the past five years from 2017, REITs have had an average annual return of around 9% while the average annualised return of direct real estate investing is at or below 8%.

While the above views are true for the Western world, in my article Which has better returns; Stock market or Property? I argue that the conclusions for Malaysia are different. I wanted to compare the historical performances of Bursa REITs with those of Bursa property stocks and Malaysian physical properties. I considered two perspectives when looking at returns:

- Changes in market prices. These changes are due to a combination of market sentiments and business fundamentals.

- Changes in fundamentals. These ignore market sentiments.

To track the performance of the REITs, I looked at the market price and fundamental performance of a panel of 11 Bursa REITs. These were the ones that had both financial and pricing data from 2007 to 2021. Refer to Appendix 1 for the list of REITs.

To track the performance of the property stocks, I tracked changes in stock prices at the KLCI Property Index. To track the changes in fundamentals, I looked at the performances of Bursa Malaysia property companies with 2020 shareholders’ funds greater than RM1 billion. Refer to the Appendix for a list of these companies. To track the price performance of physical properties, I used the Housing Price Index (MHPI).

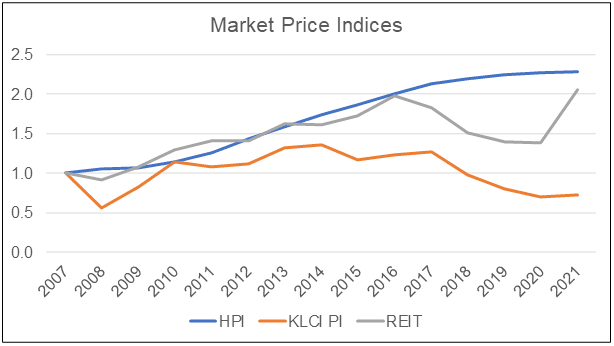

2. Market prices

Chart 1 shows the comparative gains for the REIT Index, KLCI Property Index, and HPI. Refer to the Method section for the details of these indices. As can be seen, from 2007 to 2021:

- The gain from REITs at a 5.3% CAGR was comparable to that for physical properties. However, it was more volatile.

- The worst gain was from investing in property stocks with a compounded annual loss of 2.3%.

- You are better off investing in physical properties. The HPI had a 6.1% CAGR over the past 15 years.

Note that the changes in the indices represented capital gains. In other words, we ignored the rental income in the case of physical properties and the dividends in the case of REITs and property stocks.

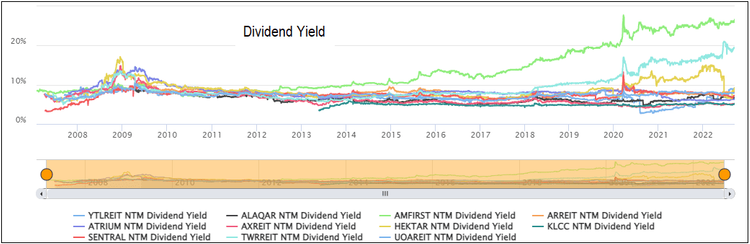

From a total return perspective (capital gain + rental or dividends), I would rate REITs better than physical properties for the following reasons:

- The average dividend yields for REITs tend to range from 6% to 8% as can be seen in Chart 2.

- According to a media report in August 2020, Savills Malaysia managing director Datuk Paul Khong, Malaysian residential…rental yields are usually low at about 4% per annum, which could hardly cover housing loan repayments.

You may argue that we are not comparing apple to apple as the REITs mostly represented offices and commercial properties (refer to Appendix 1) while the HPI, residential properties. But I would argue that a retail investor would be more likely to invest in residential properties than say a shopping mall or an office complex. So, the HPI is an appropriate metric.

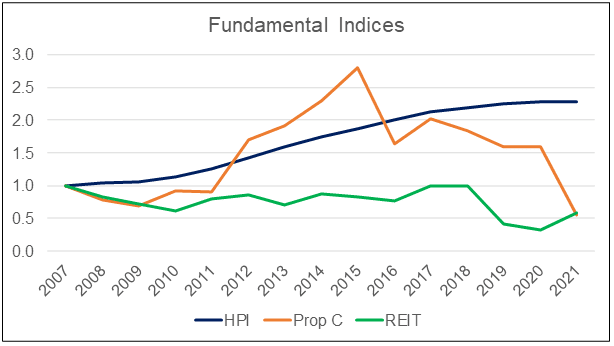

3. Fundamentals

Fundamentals refer to the basic factors that contribute to the financial performance of an asset. The three investments represent different types of businesses. You would expect them to have different fundamental drivers. As such, I have compared them based on the following metrics:

- REITs: The most critical measure of performance is Free Funds from Operations (FFO). This is calculated by adding depreciation, amortisation, and losses on sales of assets to earnings, and then subtracting any gains on sales of assets. I used the median FFO of the panel REITs here.

- Property stocks: I used the median profit after tax (PAT) of the panel as the key performance metric.

- Physical properties: The HPI not only reflects the changes in the value of the properties but is also a proxy for rental income.

Chart 3 shows the results of the analysis. You can see that:

- The REITs had a compounded annual decline of 3.8% for the past 15 years.

- The property stocks had a compounded annual decline of 4.1% from 2007 to 2015. It was the most volatile among the three.

- The HPI has the best performance with compounded annual growth of 6.1%

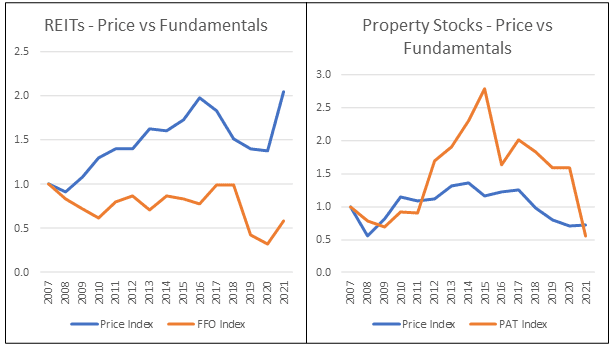

The results of the fundamental analysis differ from those from price changes. You can see the differences clearly in Chart 4. REITs have performed better than property stocks even within the same economic environment.

- The correlation between prices and FFO for the REITs was – 0.04

- The correlation between prices and PAT for the property stocks was 0.61

From a price return perspective, I would choose REITs over property stocks. This is because REITs prices in 2021 were higher than in 2007. The market seemed to have ignored the changes in the fundamentals. This could be because of the high dividend payment nature of REITs.

The fundamental analysis here is a simple one as I have only considered one metric to represent the fundamental performance. However, the FFO and PAT are key performance metrics and as such is indicative of the general direction.

SEE WHAT OTHERS ARE READING:

➡️ Top 10 most searched areas by homebuyers in Malaysia in 2022

➡️ Land title transfer in Malaysia: Procedures, documents and costs involved

Conclusions

While I have presented the financial returns of the three investments, they were based on an aggregated picture.

- The REIT panel represented different types of non-residential properties such as offices and shopping malls.

- The KLCI Property Index covered all property companies. My property stocks fundamental index focused on large companies, many of which had businesses not related to property.

- The HPI represented the performance of various types of residential properties in different parts of the country.

The returns for each of them represented investments in diversified assets.

As a retail investor, you are probably only able to invest in a few physical properties. In the Malaysian context, there are no funds or ETFs that can enable you to invest in all the REITs or property stocks.

You can then argue that as a retail investor, the results presented may not be applicable since you cannot hold similarly diversified assets. If you are going to stock pick or property pick, your returns would also be influenced by your investment-picking ability.

At the same time, with a more concentrated investment vis-a-vis investment picking, the risk to the retail investor would also be much higher.

Given the above, I would advise that a retail investor should give equal weight to the qualitative and return factors when deciding which to choose.

My advice is to invest in REITs because:

- Most retail investors would have limited financial resources.

- There would be lower financing and location risks. With REITs, it is easier to have a diversified property compared to investing in physical properties.

- It is more convenient to manage your investments compared to investing in properties.

- REITs provide better total returns (capital gain + dividends) than property stocks or properties.

However, REITs are stock market instruments. You do not simply buy REITs as and when you like. You have to learn to invest in REITs. If you are a value investor, you will look for under-priced opportunities. You should also invest in several REITs to cover all the various types of properties.

Notes on Method

REITs, property stocks, and properties are different instruments with different scales of operations. To ensure that we compare apples to apples, I establish indices for each of them.

These were obtained by dividing the values for each year by the respective 2007 values. In other words, 2007 was taken as the base of 1.0. Table 2 is an illustration of how the Property Index was computed for three years.

A. Sources of information

I extracted data from the following sources to compare market prices.

- REIT Index – This was based on the median market cap for each year for the panel of 11 REITs. These were the REITs that had data from 2007 to 2021. The market cap was derived by taking the year-end prices multiplied by the number of shares (units) at the end of the year. Data for both were extracted from TIKR.com.

- KLCI Property Index – The value for each year was the Jan 1 data for the following year. Data was extracted from Tradingview.com.

- Housing Price Index – Data were from the Valuation and Property Services Department of Malaysia.

Data for the fundamental comparisons were sourced from the following:

- REIT Index – This was the median FFO for each year for the panel of 11 REITs. Data to compute the FFO were extracted from TIKR.com.

- KLCI Property Stocks – These were the median PAT for the large companies. Large companies are defined as those with RM1 billion of shareholder funds as of 2020. The values were extracted from TIKR.com.

B. Measures of central tendency

There are two common measures of central tendency: the mean and the median.

- The mean is the simple average value of the panel. The advantage is that it makes use of every data to compute the central tendency. However, if there are outliers, the average would be skewed.

- The median. This is the mid-point value of the data that were sorted in descending order. The median then provides a better picture of the central tendency if there are outliers.

For my analysis, I used the median to represent the central tendency as there were outliers in both the REITs and property stocks.

This article was originally published as Bursa REITs, Property Stocks, or Properties – how to choose by i4value.asia and is written by Dato Eu Hong Chew.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.