The iProperty.com.my 2019 Portal Demand Analytics, a demand-supply property report compiled and published for the very first time in Malaysia, shows that the top four housing markets of Kuala Lumpur, Selangor, Penang and Johor experienced growth in demand (user visits) in 2019.

This analytics is an initiative by iProperty.com.my to provide the latest insights into subsale residential property demand by analysing consumer behaviour during their property survey on our website. Subsale residential demand is represented by site visits and compared against supply (site listings). As the number 1 property portal in Malaysia, iProperty.com.my garners millions of visits by property seekers each month. These real-time behaviours indicate where the nation’s residential subsale demand is in comparison to supply. The data points in the analytics which showcases what property types and which areas homebuyers are interested in would prove valuable to policymakers and property developers.

Do note that all visits used in this report are based on organic and direct traffic (non-paid) only. To ensure that the demand data is of the highest quality, proper due diligence was conducted. This is on top of certain measures put in place during the preparation of the iProperty.com.my 2019 Portal Demand Analytics. Please refer to the Notes section at the end of this article for more details.

Key Findings

Here are some key takeaways from the 2019 Portal Demand Analytics:

- Overall increase in demand for subsale residential properties at the national level by 13.3% compared to 2018

- Condominiums recorded a turnaround with a 14.2% growth in 2019 compared to -5.9% in H1 2019 Portal Demand Analytics. However, the demand growth is affected by a reduction in Condominium listings due to new Real Property Gain Tax policy in 2019, especially for Klang Valley areas.

- The Penang Transport Master Plan and Penang South Reclamation projects have contributed to an increase in demand for subsale houses in Penang’s strategic areas.

- An influx of new properties which have just received vacant possessions in Johor have dampened demand for subsale residential properties in the state.

- Property prices in major states throughout the country are slowly converging, with more affordable cities (second-tier) seeing their property values increase over time.

In this article, we will share the following highlights from the report:

1. National Overview of the Malaysian Property Market

2. Brief Summary of the four major housing markets – Kuala Lumpur, Selangor, Johor & Penang.

3. 10 Most in Demand Areas for Kuala Lumpur, Selangor, Johor & Penang.

National Overview: Service residences & condominiums go head-to-head in demand growth

As 2019 came to an end, the growth in user visits continued to outpace the growth in listings, resulting in an overall increase in demand for subsale properties at a national level by 13.3% year-on-year. This was mainly driven by condominiums and serviced residences which saw the largest growth in demand at 14.2% and 17. 3%, respectively, possibly due to a modest drop in capital growth.

While terrace houses exhibited a lower increase in demand at 9.0%, it is still the most popular property type among buyers, representing over 50% of subsale

residential transactions in the market.

Zooming into the top four housing markets in Malaysia, namely Kuala Lumpur, Selangor, Penang and Johor, we can see that all experienced growth in user visits in 2019. All states also experienced growth in listings except for Kuala Lumpur. Johor is the only state where the listing growth outpaced user visit growth.

Among the three property types, terrace houses emerged top in 2019 in capital appreciation with a 3.16% capital growth compared to 2018. Serviced residences, which recorded the highest growth in the iProperty.com.my H1 2019 Portal Demand Analytics, maintained its top position among the three property types, ending the year with a demand growth of 17.3% year-on-year (YoY).

Condominiums recorded a turnaround with a 14.2% growth compared to -5.9% in H1 2019 Portal Demand Analytics. This can be partly attributed to a drop in the number of listings. However, this property type registered the lowest capital growth percentage in 2019 at -2.02%.

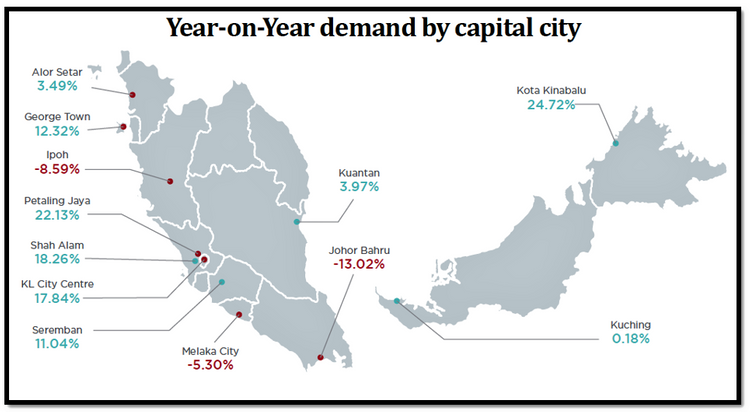

On the demand front, Kota Kinabalu sits pretty at the top with an impressive 24.72% YoY growth. The number of users looking at Kota Kinabalu grew at a much faster pace this year compared to its number of listings. Meanwhile, Petaling Jaya trails in a close second at 22.13%.

Another notable mention is Melaka City which saw its number of listings double in 2019, pulling down its demand figure to -5.3%. Based on our online research, the surge in listings was contributed by condominium projects being utilised as short-term rental units.

How did KL, Selangor, Penang & Johor fare?

Kuala Lumpur’s subsale market improved in terms of demand and recorded a 19.8% growth. Its median pricing is still the highest in the country at RM516,000 in 2019, although this figure had dipped from the H1 2019 Portal Demand Analytics median price of RM540,000. KL experienced a capital depreciation by -1.61% in 2019.

Some notable trends spotted in KL: Regardless of the mixed sentiments among the people regarding Bandar Malaysia, mega projects are always a market catalyst. With the recent reinstatement of the project in December 2019, neighbouring areas such as Salak South, Seputeh, Cheras and Taman Desa saw higher residential demand with growths exceeding 20% in 2019 compared to 2018.

Bangsar South which reverted to its original Kampung Kerinchi moniker in January 2019 has seen a huge drop in visits by more than 80%, bringing down its YoY demand to 56.81%. Capital values in Kampung Kerinchi also experienced a drop by -2.82%.

Benefiting from an overflow of population away from the city of KL, Selangor’s residential demand grew 22.4% in 2019. While the number of listings remained constant, the growth was brought about by a higher number of visits especially by users checking out the terrace home category.

Penang experienced a turnaround with demand figures jumping to 10.6% in 2019 from a disappointing -4.4% in H1 2019 Portal Demand Analytics. This positive shift can be attributed to the Penang South Reclamation (PSR) project recently approved by the state government to be part of its multi-billion ringgit Penang Master Transport Plan (PTMP). The government also announced that several PTMP projects including the PSR will be tendered out in the second half of 2020.

As for Johor, the residential property landscape remains sluggish toward the end of the year. Johor is the only major state to register a negative growth in demand in 2019. Demand figures continue their downward trend at -12.2%. However, things are slowly turning around for the better as the demand figure for the first six months of 2019 was even lower at -16.6%. The poor performance can be attributed to a property oversupply. There has been an influx of property listings in the review period as a result of owners of numerous newly built properties having received their vacant possessions.

10 Most in Demand Areas in 2019 – KL, Selangor, Penang & Johor

The areas below were ranked according to the area/property listings which garnered the highest number of unique visits from 1 January to 30 June 2019.

KUALA LUMPUR

1. Taman Tun Dr Ismail

2. Damansara Heights

3. Taman Desa

4. Desa Parkcity

5. Batu Caves

6. Pantai

7. Keramat

8. Sentul

9. Titiwangsa

10. Bangsar

Taman Tun Dr Ismail which previously occupied the No.4 position ended the year strong with growth in number of visits and drop in number of listings.

READ: (Updated) How much should the average Malaysian household income be to afford a home in KV?

1. Dengkil

2. Semenyih

3. Glenmarie

4. Gombak

5. Cyberjaya

6. Sepang

7. Sunway

8. Damansara Perdana

9. Petaling Jaya

10. Ara Damansara

Dengkil remains the most popular residential area in Selangor. In H1 2019 Portal Demand Analytics, this neighbourhood clinched the top spot, aided by an increase in visits to listings for serviced residences.

PENANG

1. Batu Kawan

2. Balik Pulau

3. Seberang Jaya

4. Kepala Batas

5. Simpang Ampat

6. Teluk Kumbar

7. Bukit Mertajam

8. Bukit Minyak

9. Juru

10. Sungai Ara

The 10 most in-demand areas in Penang remained the same as in H1 2019 Portal Demand Analytics except for the addition of Juru. Nibong Tebal dropped off the list from second position earlier this year due to a decrease in number of listings.

Teluk Kumbar is an emerging hotspot. This neighbourhood is set to be the entry point to Island B of the Penang South Reclamation (PSR) project via

the Pan Island Link 2 (PIL2).

JOHOR

1. Batu Pahat

2. Senai

3. Pasir Gudang

4. Kulai

5. Gelang Patah

6. Masai

7. Permas Jaya

8. Johor Bahru

9. Skudai

10. Tampoi

As with Penang, the list of 10 most in-demand neighbourhoods in Johor has remained the same except for one new entry: Tampoi, which replaced Ulu Tiram. With the exception of Batu Pahat, all the areas covered in this report are within the Iskandar Malaysia region.

For more subsale property data and insights, you can download the full report here.

NOTES

1) Considerations and measures put in place:

• All visits used in this report are based on organic and direct traffic only.

• Only areas that have more than 350 listings were selected to negate the effect of any spikes/big increases.

• Unique visits were used to prevent a single user from distorting the demand figures through multiple visits.

• In cases where a single user visits multiple areas, the visit is equally weighted across the multiple areas and building types to maintain the uniqueness of the user.

• Pricing is calculated for areas that have had at least 10 property transactions within one year.

• Median PSF is used to calculate capital growth due to various built-up sizes being transacted.

2) Definitions

• Unique Visit: Based on Google Analytics tracking of unique visitors, where multiple visits on the same listing by one visitor is counted as one.

• Active Property Listing: Property listings in iProperty that were active for at least one day and has a minimum of 1 view

• Property Demand: The number of unique user visits over the number of active property listing with views

• Organic / Direct Traffic: Based on Google Analytics tracking. Organic and direct traffic are not obtained through paid services or other sites