The iProperty.com.my 2020 Portal Demand Analytics revealed its demand-supply subsale residential property publication in Malaysia for 2020. The findings revealed the demand for the top four residential property markets – KL, Selangor, Penang, and Johor. Also, find out the migration trend among home seekers and the most in-demand areas for the major areas that are ranked according to consumers’ visits data compiled from January to December 2020.

Note: To ensure that the demand data is of the highest quality, proper due diligence was conducted. This is on top of the certain measures that were put in place during the preparation of the iProperty.com.my 2020 Portal Demand Analytics. Please refer to the Notes section at the end of this article for more details.

The 2020 Portal Demand Analytics by iProperty.com.my provides the latest overview of the demand trends in the Malaysian subsale residential property market using the property portal’s user visits and property listings data.

As Malaysia’s No.1 Property Site, iProperty.com.my garners millions of visits each month. These real-time behaviours indicate where the nation’s residential demand (unique visits to the site from consumers) in comparison to supply (property listings on iProperty.com.my) is leaning toward. The analysis aims to provide an insight for policymakers and property developers on Malaysian residential property preferences.

Check out the H1 2020 Portal Demand Analytics here.

Malaysia Property Market 2020 Key Takeaways

As the COVID-19 pandemic hit the real estate market across Malaysia in 2020, many states recorded a decline in property demand. The state of Selangor was however an exception, recording a positive demand for properties in 2020. Here are some key takeaways from the 2020 Portal Demand Analytics:

- In H1 2020, the national demand for subsale homes experienced only a slight decrease of -2.5%. This has since improved further to -1.3% by the end of 2020.

- The demand for terrace houses remained positive with capital growth of +2.6%. In H1 2020, it was also the only sub-category where the capital growth figure is in the positive territory, at +2.21%.

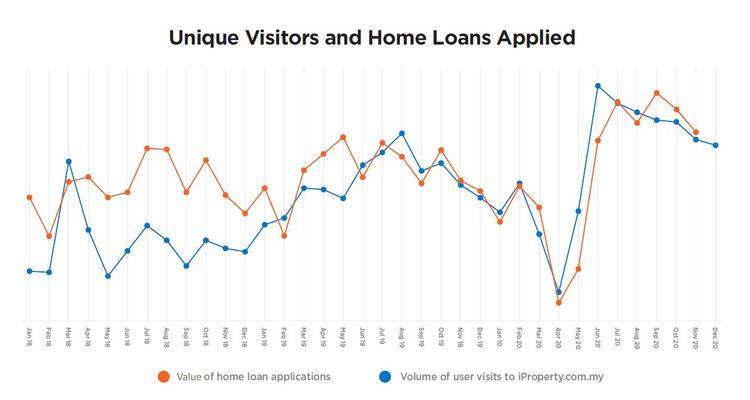

- User visits recovered by +85% since its lowest point in April 2020 due to pent-up consumer demand pushing more buying interest. The increase in property demand is aligned to the increase in the value of loan applications in Malaysia.

- Among the cities in Malaysia, only Shah Alam and Seremban recorded positive demands in 2020.

- Kuala Lumpur (KL) continues to record negative demand due to outward migration.

- Selangor benefited from the internal migration and continues to be the only major state in Malaysia to record a positive demand of +3.2%.

- The subsale housing market in Penang remained subdued in 2020. Penang’s overall subsale residential property demand has contracted by -9.5%.

- The Johor subsale residential property demand remained gloomy in 2020. However, the incoming Johor Bahru–Singapore Rapid Transit System (RTS) is set to boost Johor’s property market.

The publication focuses on four main regions; Kuala Lumpur, Selangor, Penang, and Johor. In this article, we will share the following highlights from the report:

- National Overview of the 2020 Malaysian Housing Market (subsale only)

- Change in Demand and Capital Growth for states and capital cities in Malaysia

- 20 Most in Demand Areas in Kuala Lumpur, Selangor, and Penang

- 15 Most in Demand Areas in Johor

National Overview: National Demand for Subsale Homes in 2020 improves to -1.3% from -2.5% in H1 2020

The property demand is recovering towards the second half (H2) of 2020 as the government relaxed the movement restrictions. Thus, by the end of June, the national demand for subsale homes experienced only a slight decrease of -2.5%. This has since improved further to -1.3% by the end of 2020. Also, by December 2020, unique visits for subsale property listings on iProperty.com.my saw an upward recovery of +85%.

In 2020, the national demand for subsale properties fell by -1.3% YoY. The demand for high-rise properties is down in tandem with prices while the demand for terrace houses remained positive with capital growth of +2.6%.

Although the current property market outlook is somewhat bleak in line with the ongoing economic slump, we have not seen a huge crash in the market. This is mainly due to the support provided by the government in the form of easy financing – the Overnight Policy Rate (OPR) rate was progressively reduced four times in 2020 to its current 1.75%, which is the lowest value in over 15 years. Aside from helping to ease loan repayment, this has sparked interest in property purchases, especially among middle- and upper-class households.

In the H1 2020 Portal Demand Analytics, we observed that user visits improved during the Recovery Movement Control Order (RMCO) phase and that could be due to the pent-up demand because of restrictions during the March to May 2020 stricter Movement Control Order (MCO). This growth appears to have carried its momentum in H2 2020, albeit with several small dips.

The chart below compares user visits to iProperty.com.my with the value of home loans applied by Malaysian consumers (as provided by Bank Negara Malaysia’s (BNM) Monthly Highlights and Statistics in November 2020).

As we can see, the increase in property demand as indicated by iProperty.com.my visits and its subsequent trendline is somewhat aligned to the follow-through action of these visitors indicated by home loan applications. This indicates a genuine interest in property purchase by those hunting for properties online.

Even though home loan applications have spiked, we do not see many of them being approved. The home loan approval rate in Malaysia reached its lowest point in May at 25% and as of November, it stood at 39%. Comparatively, the approval rate was at 44% in January 2020.

A lower OPR may have given access to cheaper financing, but on the flip side, bank margins are also being squeezed. Coupled with the weak employment landscape, banks have adopted a more cautious lending attitude, leading them to be pickier with loan applicants.

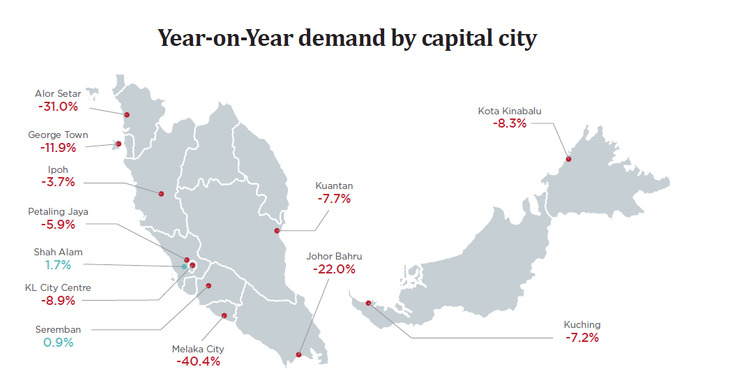

Shah Alam and Seremban are the only cities with a positive subsale residential property demand. Capital growth in major cities remained negative in 2020

The capital state of Selangor, Shah Alam and the capital state of Negeri Sembilan, Seremban have come out of 2020 as the cities to record a positive residential property demand where the figure stood at +1.7% and +0.9% respectively. In H1 2020, Shah Alam was the only major city in Malaysia to record a positive residential property demand and it continued to record a positive property demand throughout 2020. Not just that, the subsale residential property market in Seremban has improved in 2020 to +0.9% from -0.44% in HI 2020. On top of that, capital growth also improved where the figure stood at +10.6%.

The subsale residential property demand is Shah Alam and Seremban was the only one to record a positive demand due to urban-suburban migration caused by the shifts in the local subsale property market and search trends following the COVID-19 outbreak. People are looking for homes in suburban areas that are more affordable and bigger built-up sizes. This is also due to remote office working trends or work from home (WFH) which started because of the MCO.

The data shows a decline in capital growth figures in the major cities for 2020. Johor Bahru (JB) recorded the biggest decline at -22.0%, followed by Georgetown at -11.09% and KL City Centre at -8.9%. This trend was predictable as housing prices in these areas are exorbitant and would be the most affected as the pandemic has caused a great economic downfall.

Selangor continues to be the only major state in Malaysia to record a positive housing demand in 2020

Drilling down into the top four residential property markets in Malaysia – KL, Selangor, Penang, and Johor, the 2020 Portal Demand Analytics revealed that Selangor is the only major state in Malaysia to record a positive housing demand in 2020. As with H1 2020, Selangor continues to be the only major state to record a positive demand of +3.2% while capital growth dropped marginally by -0.2%.

KL continues to record negative demand at -1.3% due to outward migration. Penang’s subsale residential property demand has contracted by -9.5 while Johor, on the other hand, recorded a double-digit drop across all property categories in 2020. The property market in this southern part of Malaysia has remained sluggish throughout 2020.

Selangor, particularly its suburban areas have benefited the most from the population outflow brought about by the pandemic. These residential suburbs offer larger properties with better value for money and have seen some of the fastest growth in demand. As KL loses out on migration, there is a trend of moving to Selangor that has been taking place for years. Interest in suburban areas has been growing steadily as people seek space and solitude.

Later, we will dive into the top 20 most in-demand areas in Selangor, and the suburban areas that dominated the residential property market.

20 Most in Demand Areas in 2020 – KL, Selangor, and Penang

The areas below are ranked according to the area/property listings which garnered the highest number of unique visits from January to December 2020.

KUALA LUMPUR

- Batu Caves

- Damansara Heights

- Taman Tun Dr Ismail (TTDI)

- Taman Desa

- Setiawangsa

- Bangsar

- Pantai

- Seputeh

- Titiwangsa

- Sri Hartamas

- Sungai Besi

- Puchong

- Sentul

- Sunway SPK

- Desa ParkCity

- Brickfields

- Jinjang

- Wangsa Maju

- Bukit Jalil

- Kuchai Lama

As with H1 2020, Batu Caves remained in the first position and tops the chart as the most in-demand area in Kuala Lumpur. User visits increased to more than double in 2020 for the flat segment. Many of these users viewed properties priced at around RM150k.

Setiawangsa is another notable area on the list at fifth place. Many of its visitors were looking at properties priced between RM200k to RM300k.

SELANGOR

- Puncak Alam

- Dengkil

- Semenyih

- Cyberjaya

- Kuala Selangor

- Gombak

- Glenmarie

- Ulu Langat

- Setia Alam

- Teluk Panglima Garang

- Serendah

- Damansara Perdana

- Sepang

- Mutiara Damansara

- Bangi

- Banting

- Sunway

- Ara Damansara

- Petaling Jaya

- Sungai Buloh

Puncak Alam retained its No.1 spot since H1 2020, with a huge chunk of its audience looking for a family-sized terrace home between 1,250 sq ft to 2,000 sq ft in size and carrying RM300k to RM400k price tags.

For Ulu Kelang, visits across all building types saw an increase. The number of visits for the apartment segment nearly doubled. Most of the visitors for Ulu Kelang were interested in condominiums.

Serendah recorded the biggest growth in demand in 2020. Visitors were mostly interested in apartments and flats priced below RM100k with built-up sizes of 750 sq ft or smaller.

PENANG

- Kepala Batas

- Balik Pulau

- Seberang Jaya

- Nibong Tebal

- Simpang Ampat

- Bukit Mertajam

- Teluk Kumbar

- Bukit Minyak

- Batu Maung

- Butterworth

- Bukit Jambul

- Juru

- Gurney

- Gelugor

- Perai

- Sungai Ara

- Bayan Lepas

- Batu Feringghi

- Ayer Itam

- Bayan Baru

Kepala Batas retained its crown for the most in-demand area in Penang. The number of visits for Kepala Batas doubled in 2020, bolstered by several large-scale mixed development projects in the pipeline.

Balik Pulau also saw a significant increase in the number of visits. Both its apartments and flats segments doubled their visits figures in 2020. Third, on the list is Seberang Jaya. This area’s appeal lies in its strategic location – Seberang Jaya is sandwiched between Butterworth, Bukit Mertajam, and the Penang bridge. Its median price of RM135k is also very affordable.

Similarly, Simpang Ampat enjoys a geographical advantage. Located between the two Penang bridges, this area is set to benefit from the traffic flow in the years to come. There is also plenty of lands still within the area. The market is currently dominated by landed properties with spacious living areas priced below RM300k.

15 Most in Demand Areas in 2020 – Johor

JOHOR

- Muar

- Batu Pahat

- Kluang

- Kota Tinggi

- Pasir Gudang

- Senai

- Kulai

- Permas Jaya

- Iskandar Puteri (Nusajaya)

- Masai

- Gelang Patah

- Johor Bahru

- Tampoi

- Skudai

- Perling

Muar took the crown for the most in-demand area in Johor. Muar and Batu Pahat made it to the top of the list with several upcoming residential projects. There was a steady uptrend in property prices in these areas in 2020. By the end of the year, median prices in Muar and Batu Pahat were on par with areas within the Iskandar Region.

Meanwhile, Kluang recorded the second-highest growth in property demand. The fastest-growing prices here are for properties between RM100k to RM150k and RM300k to RM400k.

NOTES

1) Considerations and measures put in place:

• Only areas that have more than 350 listings were selected to negate the effect of any spikes/big increases.

• Unique visits were used to prevent a single user from distorting the demand figures through multiple visits.

• In the case where a single user visits multiple areas, the visit is equally weighted across the multiple areas and building types to maintain the uniqueness of the user.

• All visits used in this report are based on organic and direct traffic only.

• Pricing is calculated for areas that have had at least 10 property transactions within one year.

• Median PSF is used to calculate capital growth due to various built-up sizes being transacted.

2) Definitions

• Unique Visit: Based on google analytics tracking of unique visitors, where multiple visits on the same listing by one visitor are counted as one.

• Active Property Listing: Property listings in iProperty that were active for at least one day and has a minimum of 1 view

• Property Demand: The number of unique user visits over the number of active property listing with views

• Organic / Direct Traffic: Based on google analytics tracking, organic and direct traffic is not obtained through paid services or other sites.

For more insights, download a copy of the iProperty.com.my 2020 Portal Demand Analytics here.