This finding and more are revealed in The iProperty.com.my H1 2019 Portal Demand Analytics. Also, find out Malaysia’s most popular residential neighbourhoods among home seekers, ranked according to consumers’ visits data compiled from January to June 2019.

To ensure that the demand data is of the highest quality, proper due diligence was conducted. This is on top of the certain measures that were put in place during the preparation of The iProperty.com.my H1 2019 Portal Demand Analytics. Please refer to the Notes section at the end of this article for more details.

The iProperty.com.my H1 2019 Portal Demand Analytics provides a view of current demand trends in the Malaysian residential property market using the property portal’s user visits and property listings data. It is a demand-supply property report that’s compiled and published for the very first time in Malaysia.

As the number 1 property portal in Malaysia, iProperty.com.my garners millions of visits each month. These real-time behaviours indicate where the nation’s residential demand (unique visits to the site from consumers) in comparison to supply (property listings on iProperty.com) is leaning toward. The analysis aims to provide an insight for policymakers and property developers on Malaysian residential property preferences.

The demand data points, which pays a special focus on Kuala Lumpur, Selangor, Penang and Johor have never been available in the region before. These four areas contribute more than 60% of Malaysia’s residential market transaction share.

In this article, we will provide the following highlights from the report:

1. National Overview of the Malaysian Property Market

2. Change in Demand & Capital Growth for state capitals in Malaysia

3. 10 Most in Demand Areas in four major markets – Kuala Lumpur, Selangor, Johor & Penang.

National Overview: Serviced Residence gaining popularity

Overall, there is an increase in both unique user visits and property listings on a national level in H1 2019, as compared to H1 2018. However, the growth in user visits outpaced the increase in listings, resulting in the national property demand to increase by +4.1%.

In line with the overall market sentiment on the property market, the theme for 2019 is ‘affordability’. Hence why Serviced Residences is slowly gaining ground due to its affordable pricing and its location in strategic areas.

Serviced Residences experienced the most significant growth in demand at +14.7%, contributed by visits shifting over from Condominiums. However, Serviced Residences (with 11% of total visits) have some way to go before catching up to Condominiums (with 23% of total visits).

Nevertheless, the attraction of Serviced Residences goes beyond affordability. The appeal is also from having the right address, accessibility to public transportation and availability of commercial elements such as food and beverage outlets. Recent supply of this building type in the right locations have resulted in growing interests.

Terrace Houses, on the other hand, have seen robust growth in demand by +3.7% (with 32% of total visits). Terrace houses, which consists of more than half of the transaction market share in Malaysia, is still the more popular building type and have also maintained a positive capital growth of +6.7% with a +3.7% Y-O-Y growth in demand.

Drilling down into the top four housing markets in Malaysia, namely KL, Selangor, Penang and Johor, the report shows us that KL’s overall property demands increased by +3.8%, Selangor by +9.8%, while Penang and Johor both declined by -4.4% and -16.1% respectively.

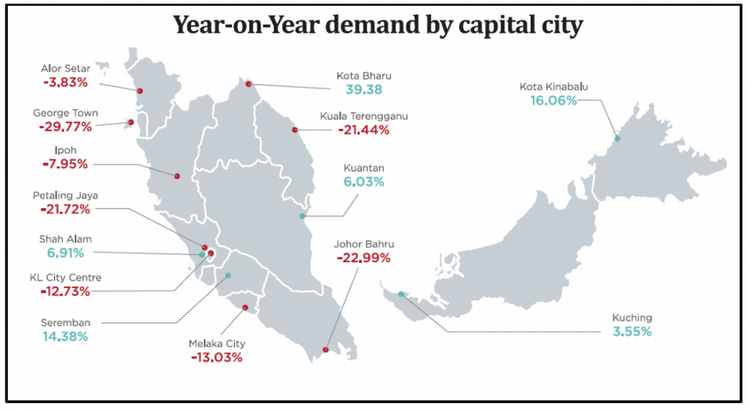

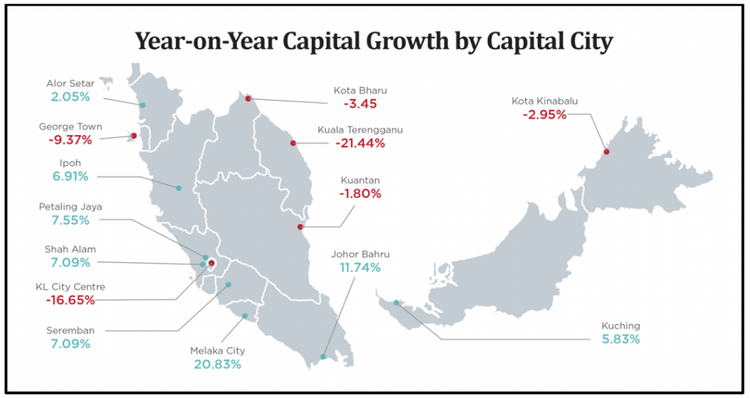

Kota Bharu experienced the highest growth in demand, Melaka city recorded biggest jump in capital growth

Below is a map showcasing the change in demand for each capital city in Malaysia, as compared to H1 2018.

Kelantan’s capital Kota Bharu came out on top as the capital city with the highest year-on-year (YoY) growth demand of 39.38%. Kota Bharu garnered a lot of interest for Apartments that are priced between RM300,000 and RM400,000.

Georgetown, on the other hand, had the biggest setback in demand with a 29.8% drop in visits.

Meanwhile, in terms of capital growth, Melaka City emerged as the champion with a YoY jump of 20.83%. This figure is pulled up mainly by Serviced Residences. The median per square foot (PSF) for Serviced Residences in Melaka City is at RM573 PSF, which is double that of other residential building types. Many of these are located near popular tourist areas and are rented out for short term stays.

10 Most in Demand Areas in H1 2019 – KL, Selangor, Penang & Johor

The areas below were ranked according to the area/property listings which garnered the highest number of unique visits from 1 January to 30 June 2019.

KUALA LUMPUR

1. *Batu Caves

2. Keramat

3. Sentul

4. Taman Tun Dr Ismail

5. Wangsa Maju

6. Damansara Heights

7. Pantai

8. Bandar Tasik Selatan

9. Kepong

10. Cheras

*Though Batu Caves is officially a town within the Gombak district in Selangor, there are parts of it which intersects and fall in Kuala Lumpur.

Batu Caves did especially well in H1 2019, recording a 73.8% YoY growth in demand, as compared to the year before. This growth was due to an increase in the supply of Serviced Residences that were completed in 2018. This attracted significant visits for Batu Caves, pushing it to the top of the list.

SELANGOR

1. Dengkil

2. Gombak

3. Semenyih

4. Cyberjaya

5. Sepang

6. Sunway

7. Bangi

8. Petaling Jaya

9. Klang

10. Bandar Utama

New listings of Serviced Residences in Dengkil have gained a lot of interest, thus bumping it up to the top spot on the top 10 in-demand areas in Selangor. Considering Dengkil had low listings to begin with, a slight increase in visits was enough to push up the demand figure in this area.

PENANG

1. Batu Kawan

2. Nibong Tebal

3. Balik Pulau

4. Kepala Batas

5. Seberang Jaya

6. Simpang Ampat

7. Teluk Kumbar

8. Bukit Mertajam

9. Bukit Minyak

10. Sungai Ara

Batu Kawan is an up and coming area on many homebuyers’ wish list as this township has been the recipient of numerous exciting mixed developments in the past few years. Other catalysts for its growth include the Penang Designer Village and the IKEA shopping centre which opened its doors in mid-March 2019. There will also be a few renowned universities and colleges, namely Hull University as well as a new branch of Kolej Damansara Utama (KDU).

Nibong Tebal, the southernmost major town in Penang is also an emerging hot spot. It spans across three Malaysian states, with parts of it cutting into Perak and Kedah. Moreover, the highly regarded USM engineering campus is located here. A 5,000-acre industrial park and mixed development in Byram is also another project to look forward to.

JOHOR

1. Batu Pahat

2. Senai

3. Kulai

4. Pasir Gudang

5. Gelang Patah

6. Johor Bahru

7. Skudai

8. Permas Jaya

9. Ulu Tiram

10. Masai

Batu Pahat has been on the radar since 2017 when the High-Speed Rail (HSR) project was announced, with the idea that this area was to house a HSR station and act as a dormitory town between KL and Singapore. However, in May 2018 after the 14th General Election, a few mega projects, including the HSR, were cancelled – leading to a decline in market interest and this was evident in visits to Batu Pahat listings on iProperty.com.my. After the HSR was postponed to May 2020 instead, visits stabilised.

iProperty.com.my has dedicated almost one year of research, planning and information gathering to produce these exclusive analytics. Subsequent editions will be made available in the future to provide relevant stakeholders with comprehensive information about existing demand for certain projects, as well as certain forecasts and recommendations.

NOTES

1) Considerations and measures put in place:

• Only areas that have more than 200 listings were selected to negate the effect of any spikes/big increases.

• Unique visits were used to prevent a single user from distorting the demand figures through multiple visits.

• In the case where a single user visits multiple areas, the visit is equally weighted across the multiple areas and building types to maintain the uniqueness of the user.

• All visits used in this report are based on organic and direct traffic only.

• Pricing is calculated for areas that have had at least 10 property transactions within one year.

• Median PSF is used to calculate capital growth due to various built-up sizes being transacted.

2) Definitions

• Unique Visit: Based on google analytics tracking of unique visitors, where multiple visits on the same listing by one visitor is counted as one.

• Active Property Listing: Property listings in iProperty that were active for at least one day and has a minimum of 1 view

• Property Demand: The number of unique user visits over the number of active property listing with views

• Organic / Direct Traffic: Based on google analytics tracking, organic and direct traffic are not obtained through paid services or other sites.