Let’s take a look at the reasons why the more affluent are opting for rental properties instead of buying their own home and what we can learn from them.

Once upon a time, only the less affluent rented houses. They rented because they could not afford the down payment for a property, or they couldn’t secure loans, or that houses were simply priced out of the market.

Then home ownership became easier. During the late 2000s, buyers could purchase homes with “no-money-down”. Banks had lending policies that were extremely favourable to borrowers. Then came the subprime mortgage crisis in 2008. Globally, people started looking at home ownership differently since the great housing recession in the US. One segment that has been rethinking home ownership is the rich.

From the outset, it doesn’t make sense. Why rent when clearly you can afford to buy? If you’re Malaysian, you probably find this to be an act most foul. How can you not aspire to own a home? Whatever your thoughts on this, a wind of change is blowing – and with more force in developed countries. Let’s take a deeper look.

Why do people rent today?

The answer would seem obvious – the primary reason most people rent is lack of financial resources to buy. Home prices in most major cities are just too high. Even for those who can get financing, the deposits required and closing costs are quite restrictive.

If you want to buy a RM450,000 house, you will need to fork out RM45,000 for the down payment and about RMRM22,000 in closing costs. You’ll also have to cough up at least RM30,000 for renovations. In total, this is RM97,000 or 21% of the price of the house. Few people have this amount saved up in cash. So yes, the primary reason most people rent is they lack the financial resources to buy.

But then, why is the fastest-growing segment of renters the affluent?

Wealthy renters, i.e those with an income bracket of RM645,000 annually or just over RM50,000 per month grew by 175% between 2007 to 2017 according to a survey by RENTCafe.com.

It gets more interesting. In the same period, the increase in homeowners for this segment was only 67%. The verdict is clear: rich households are overwhelmingly choosing to rent. This begs a more specific question…

Why do rich people rent instead of buying a home?

One explanation is even the rich are finding it increasingly unaffordable to buy. In the RENTCafe.com survey, cities such as New York, San Francisco and Los Angeles had the highest number of high income renters. Home prices in these cities are among the highest in all of the US. But, in terms of property price growth, Seattle, Charlotte, Baltimore, Fort Worth and San Jose fared better.

These cities are not the least affordable housing markets, so there must be other reasons for the rich to rent. One possibility: the 2008 housing market crash or the great recession. This event wiped out the property values of many homes. Defaults rose and large financial institutions such as Bear Stearns and Lehman Brothers collapsed. Everyone in the economy learnt a bitter lesson and home owners realised that real estate was not necessarily the safest asset class.

So home ownership ceased to become the bedrock of financial security post-2008. A second reason is that the rich are more sophisticated investors. They have access to a variety of investment options that they can understand and utilise. For the general masses, however, home ownership is easy to understand – buy a house, the price appreciates over time and equity is gained. It’s easier to understand relative to the stock market, bond market and ETFs for example.

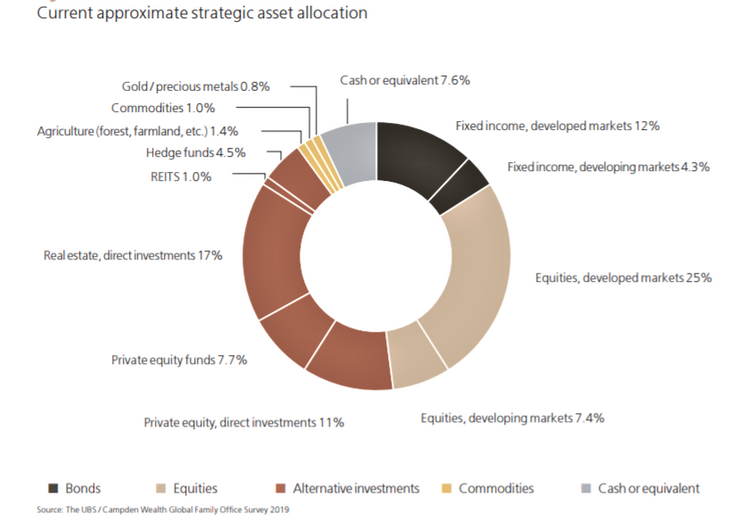

A 2019 survey by UBS reported that the asset allocation of the super-rich was unlike the average household. 32.4% of the super-rich’s asset allocation was in the equities markets. Direct investments in real estate comprised only 17% of their asset allocation.

Other surveys consistently support this finding; the rich favour a diversified portfolio and real estate is not their top investment instrument. Rich households today also comprise millennials who have a different perspective on life. The old “get a good job, get married, have children and buy a house” formula does not stick with millennials. And they’re a big group; roughly 22% of the US population are millennials, making them the second largest group after Generation Z.

Globally, millennials will soon make up 75% of the workforce. Previous generations may have favoured the security of home ownership but a house anchors you to a single place in an era where mobility has never been easier. People like FIREcracker and the Wanderer, founders of the Millennial Revolution and a couple who gained financial independence in their early 30s are leading this generation’s revolt against the traditional idea of security. This form of lifestyle of gaining traction and in fact, studies show that the rate of home ownership among millennials is lower than in previous generations.

Another reason I believe the rich are the fastest-growing segment of renters has to do with financial mathematics. A buy-to-stay house is more of a liability than an asset. When you add the mortgage interest rate, inflation rate and running costs of maintaining a house, the capital appreciation doesn’t necessarily give you a substantial increase in wealth. In addition, the monthly mortgage payments are often higher than rental income in affluent areas. This creates an opportunity cost for buyers.

Combine all the factors above and you can understand why wealthy renters are the fastest-growing segment in the US and why this trend will probably spread to other countries.

CHECK OUT: Top 5 most searched properties for rent in Mont Kiara

Why do celebrities rent houses?

Would you be surprised if I told you that some of the richest celebrities rent their mansions? These are individuals with net worths that exceed RM200 million. How about I give you some names? According to TheRichest.com, these are some celebrities who rent their mansions:

• Justin Bieber

• Lady Gaga

• Paris Hilton

• Rihanna

• Katy Perry

• Mariah Carey

Most of them pay exorbitant amounts in rent. So why wouldn’t they buy a home? Mobility comes to mind almost immediately. Celebrities are jet-setters and love being in vogue. Renting gives them the freedom to move to the latest and newest or whatever catches their fancy at any given time.

Do rich people buy homes? Of course they do, but…

Despite all the reasons for the rich to rent, many do buy their own homes. In fact, many celebrities own houses but also rent. Conor McGregor for example, owns a house in Ireland but rents his “Mac Mansion” in Las Vegas. Buying-to-rent is a great investment option – the returns are better than buying-to-stay and it’s an attractive option for the rich.

But, the rich don’t necessarily view the purchase of their house as an investment. In my experience, rich people aren’t thinking primarily about resale values and appreciation when they buy a house to stay in. They buy because they love the house or the neighbourhood. Perhaps for convenience. Perhaps to elevate their social status. Perhaps a combination of all these reasons.

These are appropriate reasons. A house doesn’t have to be an investment every time. Sometimes (if you can afford it), there’s nothing wrong with doing things that make you happy. If owning your dream house gives you such happiness and fulfilment, then why not? The rich often spend extensively on renovations and furnishing even though the value of a house does not commensurate with how much the owner has spent on prepping it up.

The satisfaction of living in a dream house is more important. So, yes, the rich do buy homes to live in but many do so with little consideration for investment returns.

But still…

Why rent when you can own your own house?

People in the business of selling homes will give you plenty of reasons to buy a house. Often, you’ll hear this phrase, “why rent when you can own?” You will then be provided with information such as potential capital appreciation and rental returns. If you’re buying-to-stay, the rent that the property can fetch is of little consequence to your investment. At least not while you live in it.

In fact, when you buy-to-stay, your house is anything but an attractive investment deal. Marketers will try to convince you otherwise but don’t be fooled. Even marketers sometimes understand the futility of speaking about financial returns with buy-to-stay properties. Have you noticed how marketers of ultra-luxurious projects rarely talk about investment returns? Experience is emphasised – usually a combination of a pampered lifestyle, social elevation, beauty and scarcity.

The joy that comes from owning the house you live in and being able to customise every inch of it to your liking is the true reason for buying a house. The financial arguments for owning-to-stay are weak, except when the monthly mortgage payment is significantly lower than the potential rent.

For example, if the rent you can fetch from owning a house is RM20,000 whereas the monthly mortgage payments to your bank is only RM12,000, the financial case for owning is good. With high-end properties, this isn’t usually the case. Let’s take a closer look.

MORE: Malaysia’s Top 7 High-Rise Properties with the Highest Rental Yield in 2019

Why should you rent instead of buy?

The case for renting can be demonstrated using a real-life example. Let’s assume you work in KL Sentral. You’re rich. Your job pays you RM40,000 per month. Your partner rakes in another RM40,000 from her job. She works in KL city. You have three children who go to school about 5km from KL Sentral. The ideal place for you to stay would be KL Sentral but because of the children, you prefer the nearby suburbs of Bangsar, Damansara Heights or Taman Seputeh.

The four-bedroom houses you like in these neighbourhoods cost RM5 million. Your monthly mortgage payments would be RM21,000 at least. Renting a similar type of house instead would cost you RM15,000 a month. You save RM6,100 if you rent.

Let’s say you buy the house and spend RM300,000 on renovations and furnishing. After 15 years and with a 4% average yearly appreciation on the property, your total equity built would be in the region of RM500,000. This is your gross profit if you sold.

After deducting RPGT and agent fees, you may net RM310,000. Your annualised rate of return in this case is 1.69%. You’d have fared better keeping your money in a bank which pays you 3% p.a in interest.

Now, let’s assume you rent instead. You’re saving RM6,100 every month as a result. You also save about RM1,000,000 in deposit, renovations and closing costs. You then open an account in StashAway (an ETF platform) with the RM1,000,000 and deposit the savings of RM6,100 every month into this account. You choose an average annual interest of 7% net. At the end of year 15, you would have RM4.8 million in your account. Your net profit after deducting the initial capital and monthly deposits would be RM2.7 million.

Relative to owning, that’s a difference of nearly RM2.4 million in equity! As you can see, the financial argument for renting is rock-solid. And then you have that other reason that has attracted many millennials – mobility. Want to upgrade to a larger home? Easy. Want to downsize? No problem. Want to move to a different country? Anytime. This freedom is absolute gold for the rich and for many millennials.

READ: The Complete Guide to Gated & Guarded Communities in Malaysia

Should you sell and rent instead? (Hold on to your horses, pal.)

We’ve looked at the maths for buying-to-stay. What about buying-to-rent? Let’s go back to the example we just used. If you buy the four-bedroom house to rent, you would be collecting RM15,000 in rent. From the outset, it looks like a loss-making proposition. Your monthly home loan repayment to the bank is RM21,000, so you’re short by RM6,100 every month on that count alone. You also have other costs such as vacancy, insurance, taxes, annual repairs, maintenance and real estate agent fees. Your total outgoings will be about RM12,000.

But, if the house appreciates by 4% every year and the rent increases by 10% every 5 years, at the end of 15 years, you’d net nearly RM2.5 million. The gain is 800% more than if you buy-to-stay! So don’t sell your house yet. You can rent it out. If you’re wondering why the huge difference between buy-to-own and buy-to-rent despite low rental yields, let me explain.

Even though the rental income does not fully cover your monthly payment, it does cover the interest. That means, your mortgage is actually interest-free. And the interest cost is significant. Over 15 years, it amounts to RM2,271,490.

Therefore, buying-to-rent can be profitable. Do the maths. If you’re not sure, hold on. Make a thorough inquiry into the financials. Watch your cash flow. Remember, in the example above, you have to fork out about RM12,000 every year. In addition to that, you also have the cost of the house you live in.

Note that the gains I have demonstrated with renting only works if you have strong financial discipline. If you’re not in the habit of saving diligently, you will not gain from the savings in opportunity cost. In this case, you will be better off buying a house to live in.

Remember the non-financial considerations too. Do you want the freedom of mobility? You can’t easily get up and leave if you own the house you stay in. Whereas if you rent, you have more freedom to relocate or upgrade. If this freedom doesn’t excite you, renting the house you live in may not give much satisfaction.

Forget the rich and famous. What do YOU want?

Forget the fact that the fastest-growing segment of renters in the US are the rich. Forget that many celebrities rent. Forget the investment calculations.

What is it that YOU want?

Do you want the joy, satisfaction and pride of owning the house you live in? Do you imagine yourself raising children and growing old with your partner in a house of your own? A house that you’ll renovate and beautify over time in the way that you want?

Or…

Do you hate being tethered to any single place? Do you love keeping up with the trendiest neighbourhoods? Are you a digital nomad? Are you driven by the highest investment returns? Knowing your aspirations and what resonates with you is important. Whether you’re affluent or not, you don’t have to parrot the rich. Instead, remain true to yourself.

*This article was repurposed from “Why Rich People Would Rather Rent (+ What You Can Learn From Them)” first published on LivingSpace.