The Malaysian property market may be cyclical but the long term direction is up. Here we share several strategies you can apply to help weather market fluctuations.

One of my close friends, who is a real estate speaker and author, taught me that the property market always trails the economy. If you know your Economics 101, the economy is cyclical – there’s usually a boom followed by a bust. Specifically, there are 4 stages:

1. Expansion – the period of growth

2. Peak – the stage where the economy cannot grow any further

3. Contraction – the bust

4. Trough – the bottoming out of the market

The property market also goes through this cycle. The good news is that these cycles are predictable to some degree, but we need to bear in mind that it is near impossible to know exactly when the market will progress to the next stage.

Understanding this is important. If you do, you will not panic every time the property market goes down and likewise, be overly excited when it swings up. You will need to anticipate such things as the normal motions of an economic cycle. You may now be wondering if property investment is a zero-sum game since it is cyclical.

The answer is no, it isn’t. This is because the highs in each cycle is usually higher than the last; therefore the general trend is upward.

As long as land is scarce, the trend will be up. The human population is increasing, and at a faster rate than before. In the last century, between 1900 and 2000, the world’s population grew 3 times faster than the entire preceding history of man – there are currently over 7 billion people on Earth.

This is a situation where demand is increasing for a commodity that is finite. The laws of demand and supply unequivocally state that prices will always go up when demand exceeds supply.

So the only way for property is… yes, you guessed right, UP! Nevertheless, this would hold true for the next 40-80 years before world population starts declining. When this happens, demand will drop or plateau and prices may naturally contract.

READ: Setting up an Investment Holding Company (IHC) – What property investors need to know

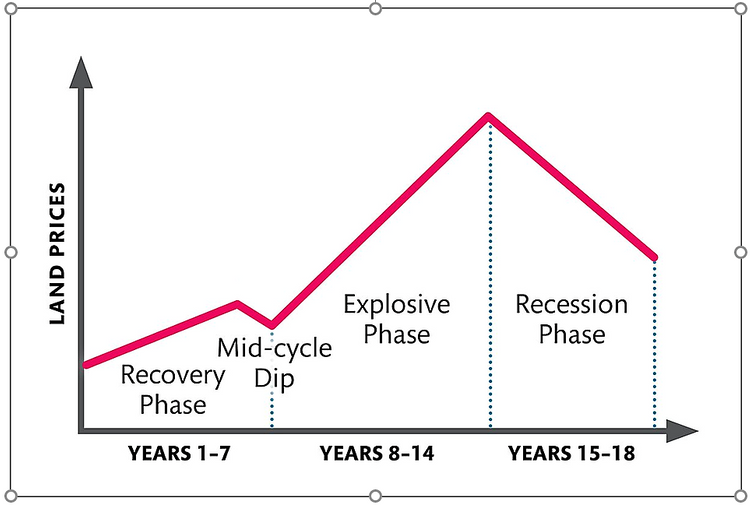

What is the 18-year property cycle?

Sometime in the early 20th century, Homer Hoyt, a real estate professional discovered that property prices are cyclical. He also realized that these cycles happened in almost perfect 18-year cycles.

Hoyt’s research was popularised by economist, Fred Harrison, in his book “Boom Bust.” Interestingly, this book which was written in 2005, predicted the 2008 housing crash in the USA.

Harrison has been quite accurate in his predictions on the housing market on more than one occasion. He predicted that Britain’s housing market would plateau when the ratio of house prices to earnings hit 6:5 – this happened in 2007.

The illustration below illustrates this 18-year cycle, which consists of 3 phases and a sub-phase within the first phase.

Recovery phase

The first phase takes place after a crash and continues on for 7 years. During this time, smart investors begin to see opportunities in the market after a crash and are willing to risk capital in the property market.

What’s happening is that the market is now a buyer’s market. There are many good deals. Prices would not have appreciated much in the last 4 years or may have contracted – therefore, buyers are able to source properties at what they perceive as attractive prices.

Many developers have adjusted their products to meet current demand pressures and may be offering great incentives, slowly driving more people into the market. During the recovery phase, property appreciation of 5-6% is normal.

Along the way, somewhere between the 5th and 7th years of the recovery phase, there is a mid-cycle dip. Perhaps, investors who got in early have now started divesting to realise profits as there is more supply in the market.

A majority of investors, having only recently witnessed a crash, may predict another meltdown in the mid-cycle dip. But this does not happen. Instead, after this short dip, the market goes into the explosive phase.

Explosive phase

This phase lasts another 7 years. During this good time, appreciation can be in double digits. Sentiment is running high and many young investors entering the market now may not have recollection of the last crash.

The last 2 years of the explosive phase is known as the “Winner’s Curse.” If there is a bad time to buy properties, this is it.

This is when the market is at its peak. Investors who enter the market here would almost immediately see a drop in value and it would take a considerable amount of time to recover. This happened in Malaysia circa 2013. A large number of people who bought during this period have not seen an increase in capital.

While the “Winner’s Curse” is taking place, it’s not uncommon to hear grandiose construction projects in the making – like the tallest skyscraper, largest shopping mall and so forth. Think of the Petronas Twin Towers, KLIA Airport, and Putrajaya in 1995-98 or the plans for TRX, PNB118 and 8 Conlay in 2012-2014.

Recession phase

The next phase lasts about 4 years. This is the crash and recovery period of the property market. Banks will tighten credit, interest rates go up and a new equilibrium is reached.

In this phase, sentiment is low and the majority of people will be expecting ‘things to get worse’ almost perpetually. If you look at the available data, you will know that these stages do not last forever.

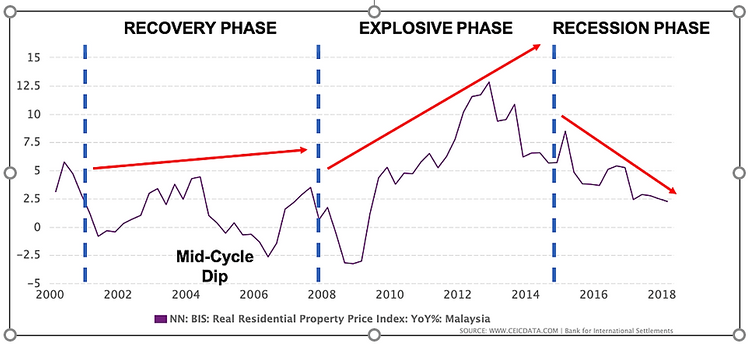

What is the property cycle like in Malaysia?

Applying this cycle in the context of Malaysia, we can see a pattern that closely follows Fred Harrison’s model.

Below is a chart sourced from CEICData.com on Malaysia’s housing price index from 2000 to 2018.

The recovery phase takes place between 2001 to 2008 with a mid-cycle dip happening somewhere in 2004. In 2008 where the explosive phase is supposed to take place, there is another dip before a real good run, hitting double-digit growth in 2013.

The recession phase in reality, kicks in by 2014 although I have marked the commencement at 2015 following Fred Harrison’s convention. If the cycle follows the 18-year model, a recovery is due in 2019 or 2020.

The Winner’s Curse took place in

Note that the first 2 phases did not happen in exactly 7-year intervals, but that is besides the point. The most important demonstration here is that there is a cyclical pattern. As long as you are aware of this, you will be able to make better decisions.

Detractors of the 18-year cycle mostly argue that the cycle does not happen in exactly 18-year intervals. I acknowledge this but it cannot be denied that the cycle exists even if not in perfect intervals.

MORE: 5 Important property market lessons Malaysians can learn from Covid-19

What can investors learn from this cycle?

Lesson 1: The recovery phase in every cycle usually starts higher than the last recovery phase. Typically, the highs of the current cycle is higher than the previous cycle’s. This has a significant implication. It indicates that it’s almost always a good time to be buying property with the exception of the “Winner’s Curse” period.

Lesson 2: The 18-year cycle prepares you for ups and downs in the market. It is normal for the property market to have booms and busts. It doesn’t work to your advantage to panic and make decisions you normally wouldn’t as a bust is most likely going to be followed by a boom.

One interesting thing to note – research suggests that recoveries are always higher and faster than expected. After the 1997 Asian Financial Crisis that hit Malaysia’s property market hard, the subsequent rebound was faster than everyone expected. With such a good run from 2009, the vast majority of buyers and developers completely forgot that a contraction would come again. Similarly, the rebound after the 2008 housing market crash in the US was fast and high.

Lesson 3: Never over-leverage. Leverage is highly risky. This means borrowing from the banks. Many property investors love to take 90% or 100% loans. This maximises your returns from appreciation. However, high-leverage usually means poor cash flow.

At a time where rental yields are 4% and below, borrowing up to 90% to finance your property purchase could mean you are negatively geared or bleeding money. This is not a good situation, unless you have enough income to cover the shortfall. If you can afford the outflow of cash and you have bought a property on good fundamentals, the combination of leverage and appreciation can net you phenomenal returns.

As long as you are able to hold a property indefinitely, boom or bust has no bearing on you. You can pick the most advantageous time to sell. However, if you are unable to hold on to a property due to cash flow constraints, you may be forced into a sale which may not benefit you.

Lesson 4: Most of the time, it is good to be doing the opposite of what the majority are doing. For example, in the recovery phase, most people will be staying out of the property market except for savvy investors. When everyone else is selling, they start buying.

In this context, as the cycle is approaching the “Winner’s Curse”, everyone will be buying but smart investors will be holding or selling off their least attractive portfolios.

Earl Nightingale, one of the best motivational speakers I know, had this to say, “Look at what the majority of people are doing, and do the exact opposite, and you’ll probably never go wrong for as long as you live.”

*This article was repurposed from “Why Understanding The 18-Year Property Cycle Will Make You A Better Investor“, first published on LivingSpace| Edited by Reena Kaur Bhatt