What are the property investment opportunities we can expect during and after this virus outbreak? Is it a good time to buy or sell a property? All your burning real estate questions answered below.

Covid-19 has significantly weakened global growth prospects. Not only because it is a communicable disease that spreads quickly across countries, but also because a majority of businesses are forced to shut down due to imposed containment measures. Following the uncertainties exacerbated by the Movement Control Order (MCO), the Malaysian property market is expected to face contraction in the next few months in terms of transaction volume and value. House prices are likely to see a decline accordingly, signalling an opportunity to buy or invest in the housing market.

LESSON 1: Falling house prices does NOT make housing more affordable

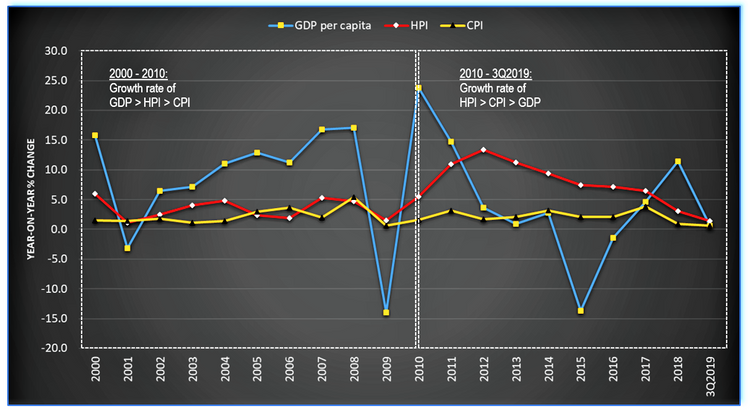

In theory, falling house prices do help to make owning a house more realistic, especially for the first-time homebuyers. This is because in the past decade (since 2010) have seen a rapid house prices growth without the support of a fast-growing economy, leading to the decreased housing affordability nationwide (Figure 1). Meanwhile, the country’s housing market is also marked by other challenges such as a mismatch in supply-demand (in terms of product, pricing, and location) and other factors which have further decreased the consumers’ purchasing power. Hence, a fall in house prices during Covid-19 could be a “price adjustment” in the market that helps lower down the “entry-level” price for homebuyers.

However, in reality, falling house prices may not necessarily be making houses more affordable. This is because the housing market is not the only sector that goes through an adjustment because of Covid-19. Other sectors are adjusting as well – for example, wages growth could be lower or zero during the crisis, and the unemployment rate could hit the highest level yet; leading to the negative household debt-servicing capacity.

Also, banks are likely to tighten their lending conditions in order to reduce their exposures to a higher risk of possible default from mortgage payments. Hence, making it just harder for first-time homebuyers to enter the market. Times like these tend to favour cash buyers rather than those who need to scrape together a deposit and secure a home loan.

MORE: What is the impact of COVID-19 on Malaysia’s property market?

LESSON 2: Majority of property owners prefer to hold rather than sell, right now

Although the pandemic has opened up good investment opportunities with motivated sellers looking to cash out their properties during tough times, only those who are in very secure jobs and are financially “liquid” will benefit from it. Those that are facing uncertainty about how COVID-19 will affect their pay are generally not in the mood to spend or invest.

Furthermore, not all investors and property owners are willing to sell during the crisis, as a fall in prices is associated with a decline in wealth. To note, the housing market tends to operate in periods of “frenzy” alternating with periods of “inactivity”. People will try to capitalise and trade up in a hot market, but to stay where they are and wait for prices to improve when the market cools. Also, due to the 6-month loan moratorium by Bank Negara Malaysia, people will hold on their selling and will only cash out when the market has recovered.

This awareness of negative equity will further encourage people to hold on selling, leading to the reduction of supply of lower-priced houses in the market.

CHECK OUT: Top 10 most viewed properties by Malaysian home buyers during MCO

LESSON 3: House prices will not decline rapidly, but rebound quickly from the temporary drop

It is worth pointing out that the country’s housing market is quite resistant to price drops. Often, fast recovery is observed in the market after a crisis, owing to the favourable lending policy, market optimism from the buyers upon future capital appreciation from property investment, as well as the drumming-up market sentiment from the developers.

On this basis, though house prices may drop slightly during Covid-19, the market will soon return to its long-running trajectory of rising prices and declining housing affordability. This is not only due to the pent-up demand coming from those who are unable to fulfil their buying obligation during the crisis, but also attributed to various financing schemes and rebates offered by developers.

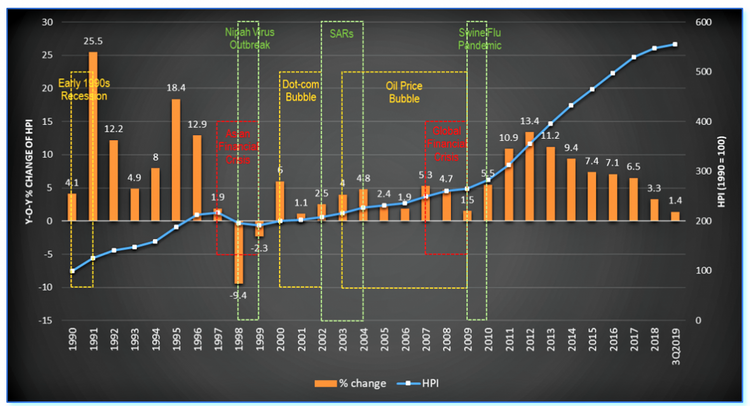

Historically speaking, the periods recorded for falling house prices in the country are less frequent than periods of rising prices. Malaysia has experienced 5 economic crises: Early 1990s Recession, Asian Financial Crisis, Dot-com Bubble, Oil Price Bubble, and Global Financial Crisis; along with 3 epidemic outbreaks: Nipah Virus Outbreak, Severe Acute Respiratory Syndrome (SARs), and Swine Flu Pandemic throughout the period of 1990 – 2018 (Figure 2). Interestingly, Malaysian house prices only suffered a decline in 1998 and 1999 which was considered a direct lingering effect of the 1997 Asian Financial Crisis. Other crises seem to have a lesser impact on the country’s house prices.

LESSON 4: Most property types are resistant to short-term fluctuations

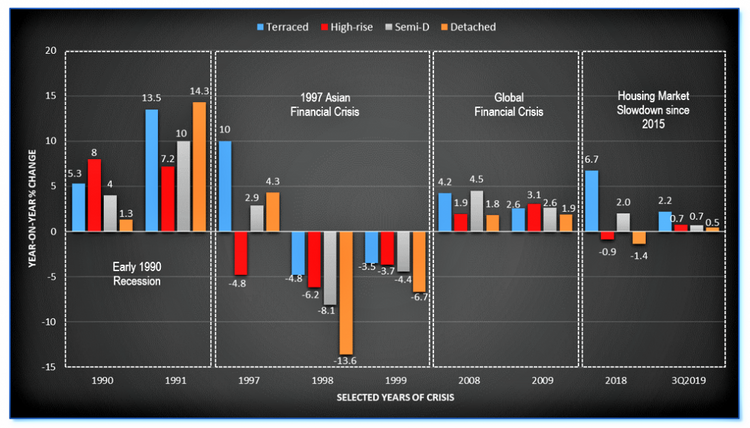

Even if we were to look closer at each property type (i.e. terraced, high-rise, semi-D, detached), these economic crises appeared to have less influence on house prices (Figure 3). The country’s house prices only fell significantly in conjunction with the 1997 Asian Financial Crisis, with the most decline recorded by detached houses at 13.6%; while other properties suffered a dip less than 10%.

Prices for high-rise properties, on the other hand, are more sensitive to economic crises. Any slowdown in economic growth can cause a rapid erosion of investors’ confidence, which then reflected in the fall of property prices.

Based on the above, prices for high-rise and high-end properties are likely to experience a decline in the first half of 2020, and the overhang units of these types of property will surely increase to a new high, offsetting any improvement that have been achieved through the Home Ownership Campaign (HOC) in 2019. In the case of terraced houses, a more moderate price growth is expected, due to the strong confidence on its profitable return among investors. This is well reflected in 2018, where terraced house prices still achieve a 6.7% growth as compared to those in high-rise (-0.9%) and detached houses (-1.4%), despite the serious supply-demand mismatch and increasing overhang units in that particular year.

LESSON 5: The Covid-19 impact on property developers is not so severe

While it is still too early to conclude the quantum and economic costs brought on by Covid-19, one should realise that the property market crash which occurred during the Asian Financial Crisis is not likely to happen again, as the root cause of the crises are totally different from each other. Back then in 1997, the financial sector had to be bailed out by the government as they were short of liquidity due to weaknesses in the system. But the economic costs that we are facing today are almost certainly related to weak economy activities, poor property market sentiment, and tightening guidelines for banks, which have significantly contributed to the reduction of seller and buyer traffic in the market.

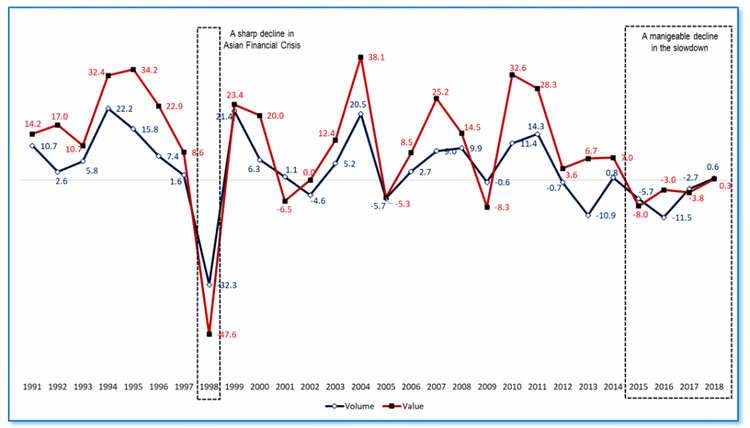

Also, the market contractions caused by Covid-19 are unlikely as severe as those experienced in the Asian Financial Crisis – a plunge of 47.6% and 32.3% for both the value and volume of transactions. Rather, it is more like a manageable decline signalling a healthy price correction in the market. This is because, prior to the pandemic (since 2015), the country’s housing market has seen a declining trend for a consecutive 4-year period (Figure 4).

Throughout this period, slow growth in revenue and dwindling profit margin are a norm to most property developers. In order to stay competitive in the market, developers have adjusted their business strategies so as to suit the market recession phase. In this sense, it is believed that most of the developers have well-prepared to cope with the impact of Covid-19, and have even adapted themselves to the new norm in the post Covid-19 era.

This is evidenced by studying the statement to shareholders of each property development company’s annual report (downloadable from Bursa Malaysia website); where different responses and operating strategies have been undertaken by developers in order to stay competitive in the dampened market, including (i) focus on reducing existing inventories; (ii) delay the launch of new projects; (iii) focus on new phases of existing projects; (iv) focus on the right products to cater for the affordability; (v) actively pursue land acquisition opportunities; (vi) explore potential joint ventures with landowners or government agencies; and (vii) tailoring new launches towards Transit–Oriented Developments (TOD).

Besides, it is mostly thanks to the HOC in 2019 which has successfully helped in strengthening today’s cash flow situation for a majority of developers. Exposure to gearing is expected to be more manageable as developers have strong unbilled sales to tide them over for at least another year or two. On this basis, the possibility that Covid-19 could trigger a corporate debt crisis amid the period of falling property prices is deemed lesser.