Learn how SJKP Madani 2026 helps Malaysians access government-backed home financing, including eligibility, application steps, and benefits.

Skim Jaminan Kredit Perumahan (SJKP) Madani is a Government-backed housing financing guarantee scheme in Malaysia designed to help citizens access home loans, particularly those without traditional income documentation.

The scheme is administered by Syarikat Jaminan Kredit Perumahan Berhad, which operates the Government guarantee framework that many banks use when evaluating applicants under SJKP Madani in 2026.

According to the SJKP scheme, it provides mortgage financing of up to RM360,000 to eligible buyers, covering the purchase price and certain associated costs, such as legal and valuation fees.

As of 2026, this scheme continues to support a wide range of buyers, including those with fixed and non-fixed income, self-employed individuals, and gig workers, by offering structured support that complements standard lending assessments by participating financial institutions.

What Is SJKP Madani And How Does It Work?

SJKP Madani operates by offering a Government guarantee on home financing applications, rather than providing loans directly. Participating banks use this guarantee to support eligible applicants, but final approval remains with the bank based on its credit and affordability criteria.

This means that while SJKP Madani can increase a buyer’s chance of obtaining financing, it does not automatically guarantee loan approval.

How The Guarantee Framework Works?

Under SJKP Madani, the guarantee framework outlines how the Government supports eligible home financing applications by sharing part of the lending risk with participating financial institutions, while banks continue to conduct their standard credit and affordability assessments.

- Participating financial institutions assess the applicant’s overall financial profile and credit history.

- If the basic eligibility criteria are met, the bank may include SJKP Madani in the loan application process.

- SJKP Madani provides a guarantee up to a defined limit to reduce the lender’s risk for eligible applicants.

- The bank then issues a financing offer based on its internal lending rules and the guarantee support.

This framework is intended to broaden access to housing loans, including for individuals who do not have traditional proof of income, such as salary slips.

Key Objectives Of SJKP Madani

The key objectives of SJKP Madani focus on improving access to home financing for eligible Malaysians, while ensuring that lending decisions remain guided by affordability, credit assessment, and responsible borrowing principles.

1. Primary Objectives Of The Scheme

SJKP Madani has several key objectives that align with the Government housing policy goals for 2026:

- To improve access to home financing for Malaysian citizens with fixed and non-fixed income, including self-employed and gig economy workers.

- To support sustainable homeownership by encouraging affordability assessments and responsible lending practices among participating banks.

- To provide a structured support mechanism that helps buyers overcome documentation challenges that might otherwise limit their ability to secure conventional loans.

According to the Government’s official benefits portal, SJKP Madani is part of a broader set of initiatives aimed at assisting those who find traditional proof-of-income requirements restrictive.

Who Qualifies For SJKP Madani In 2026?

Eligibility for SJKP Madani is defined by a combination of Government-set criteria and participating bank requirements, with the scheme itself outlining broad eligibility parameters that all banks must consider.

1. Basic Eligibility Requirements

To qualify for SJKP Madani in 2026, applicants typically must:

- be a Malaysian citizen aged 18 years or above at the time of application.

- be applying for housing financing for owner-occupation, not purely for investment.

- have all named parties in the Sale and Purchase Agreement as the intended occupiers of the property.

According to the official SJKP eligibility guidelines, joint financing is allowed, and both fixed- and non-fixed-income earners may apply.

Income And Employment Profiles Considered

SJKP Madani does not discriminate based on employment type, which is one of its core strengths for 2026 applicants:

- Fixed Income Earners: Individuals with formal employment and regular pay slips.

- Non-Fixed Income Earners: Individuals such as freelancers or workers without traditional pay documentation.

- Self-Employed Individuals: Small business owners, independent consultants, and gig workers whose income may be irregular.

- Gig Economy Workers: Riders, drivers, and others with variable or non-standard income patterns.

These broader categories underscore the scheme’s role in providing government support for a wider range of Malaysians who can demonstrate repayment ability, even without standard income proofs.

Property-Related Eligibility Considerations

The property being purchased under SJKP Madani in 2026 must meet specific owner-occupation criteria:

- Residential properties, including new, under-construction, or resale homes

- Property must be intended for owner-occupation and not solely for rental or commercial use

- Maximum financing limits (such as RM360,000 for SJKP Madani coverage) apply to the loan amount guaranteed

Participating banks may apply additional property value thresholds based on their internal risk policies.

Financing Scope And Limits Under SJKP Madani

The financing scope and limits under SJKP Madani outline the maximum loan coverage, tenure considerations, and cost components that may be supported under the scheme, subject to prevailing guidelines and bank assessment in 2026.

1. Loan Coverage And Maximum Financing

Under SJKP Madani in 2026, the Government guarantee can support financing of up to RM360,000, which includes:

- up to 100% of the purchase price of the house.

- up to 20% of the house purchase price for additional costs such as MRTA/MRTT, Long Term House Owner’s Takaful (LTHO), solicitor’s fees, valuation fees, renovation, and home furnishing costs.

This structure means that buyers may obtain financing that covers not just the property price, but also associated costs, subject to bank and scheme policies.

2. Financing Tenure

- The financing tenure under SJKP Madani may be up to 35 years, or until the loan maturity condition is met, whichever comes first.

- “Two-generation” financing, where a younger co-applicant helps extend the tenure, may be allowed at the bank’s discretion under its internal policy.

Although SJKP Madani provides structured support, final tenure and profit rates are still determined by the bank based on affordability and credit assessment.

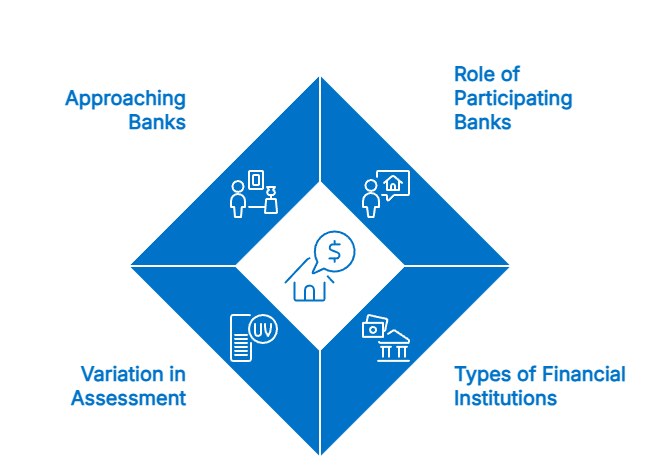

Participating Banks And Financial Institutions

SJKP Madani is implemented through a network of participating banks and financial institutions that work with Syarikat Jaminan Kredit Perumahan Berhad (SJKP) to offer Government-backed home financing to eligible applicants.

Under this framework, SJKP provides a guarantee to participating lenders. At the same time, banks remain responsible for conducting credit assessments, determining financing terms, and approving applications in line with their internal policies and regulatory requirements.

1. Role Of Participating Banks

Participating financial institutions act as the primary point of application for buyers seeking financing under SJKP Madani. According to official scheme guidance, banks continue to assess applicants based on affordability, repayment capacity, credit behaviour, and documentation, even when a government guarantee is involved.

The presence of the SJKP Madani guarantee does not replace bank due diligence; rather, it supports the assessment of eligible applicants who may not meet conventional documentation requirements.

2. Types Of Financial Institutions Involved

SJKP Madani financing is generally offered through a combination of:

- Commercial banks

- Islamic banks

- Development financial institutions

These institutions may offer either conventional or Shariah-compliant home financing products, depending on the bank’s portfolio. The availability of SJKP Madani financing products may therefore differ between institutions.

3. Variation In Assessment And Financing Terms

While SJKP Madani provides a common guarantee framework, financing outcomes may vary between participating banks. Factors that can differ include:

- Documentation requirements for fixed and non-fixed income earners

- Financing tenure offered

- Profit or interest rates

- Treatment of additional costs, such as insurance or legal fees

As highlighted by SJKP, approval decisions remain subject to each bank’s internal credit policies and Bank Negara Malaysia’s responsible lending guidelines.

4. Approaching Banks For SJKP Madani Financing

Official guidance from SJKP encourages applicants to approach participating banks directly to confirm eligibility criteria, documentation requirements, and financing structures before applying. Buyers may also compare offerings across multiple banks to better understand available options and assess suitability based on their individual financial circumstances.

As participating banks apply their own assessment frameworks and financing terms under SJKP Madani, applicants are advised to seek clarification directly from financial institutions and review multiple options to make informed home financing decisions.

<strong>Estimate monthly instalments with the Home Loan Calculator.</strong>How To Apply For SJKP Madani: Step-By-Step Guide

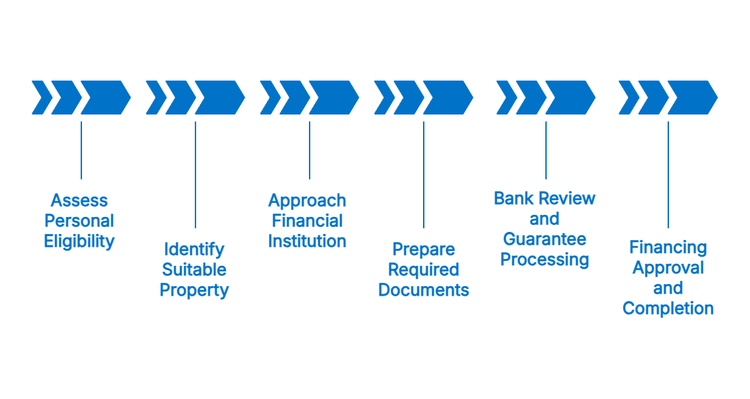

Applying for SJKP Madani involves a structured process carried out through participating banks, beginning with an assessment of personal eligibility and affordability, and concluding with bank-led financing approval supported by the Government guarantee.

While the scheme provides additional support for eligible applicants, all applications remain subject to standard credit evaluation, documentation checks, and repayment capacity assessment by the financial institution.

- Assess Personal Eligibility And Affordability

Before applying, potential applicants should review their income, repayment capacity, and credit history to ensure they are ready to submit a complete application to the bank.

- Identify A Suitable Property

Choose a residential property intended for owner-occupation that meets both your needs and the financing criteria set by the bank.

- Approach A Participating Financial Institution

Visit a bank branch or contact the bank’s home loan officer to express interest in leveraging SJKP Madani for your loan application.

- Prepare And Submit Required Documents

Banks typically require personal, income, and property documents as part of the loan application. Although requirements vary, standard documents include proof of identity, income verification forms, and the sales agreement.

- Bank Review And SJKP Guarantee Processing

The bank will assess the application on its credit and affordability criteria and, if eligible, submit the guarantee request under SJKP Madani to the SJKP operator.

- Financing Approval And Completion

Once approved, the bank issues a loan offer outlining the terms, which the applicant can sign to proceed with the home purchase.

This typical process aligns with general guidance on housing loan applications under SJKP schemes.

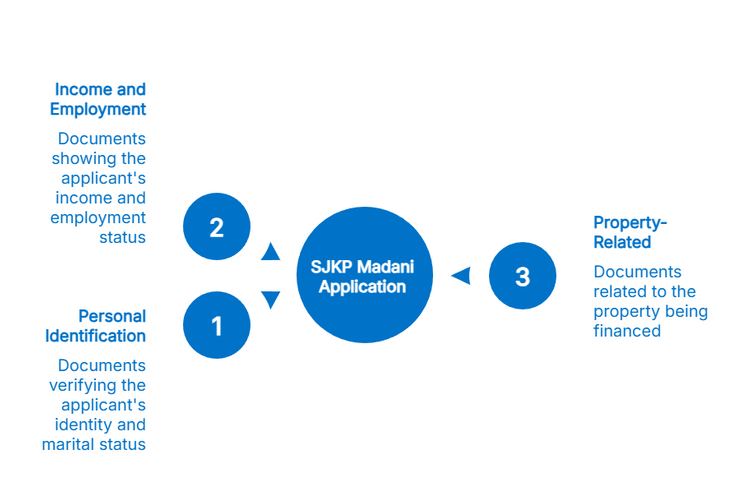

Documents Commonly Required For SJKP Madani Applications

When applying for home financing under SJKP Madani, applicants are required to submit a set of supporting documents to allow participating banks to assess eligibility, affordability, and repayment capacity.

While documentation requirements may vary between financial institutions, the scheme generally accommodates both fixed and non-fixed income profiles, with banks using these documents to conduct their standard credit and financing evaluations.

- Personal Identification Documents

- National identity card (NRIC)

- Proof of marital status, if applicable

- Income And Employment Documentation

- Salary slips or employment letters for fixed-income earners

- Bank statements or income declarations for non-fixed income earners

- Business registration documents for self-employed applicants

- Property-Related Documents

- Sale and Purchase Agreement

- Proof of booking or reservation

- Other legal property documentation as required

Documentation requirements vary by bank, and applicants should confirm with the bank’s home loan officer before submission.

Key Considerations Before Applying

Before applying under SJKP Madani, buyers are encouraged to review several practical and financial considerations to ensure that the financing aligns with their long-term affordability, repayment capacity, and homeownership plans.

- Important Factors Buyers Should Review

- Monthly Repayment Affordability: Ensure prospective instalments align with monthly income and expenses.

- Financing Tenure: Longer tenure may reduce instalments but increase overall repayment.

- Credit History: A clean credit profile may improve chances of approval.

- Bank-Specific Requirements: Each participating bank may have additional criteria beyond SJKP scheme eligibility.

Bank Negara Malaysia emphasises responsible borrowing, and buyers should factor this into their planning before applying for financing.

Benefits Of Applying to SJKP Madani

For eligible applicants, SJKP Madani offers several practical benefits:

- Broader Eligibility: It helps individuals without traditional proof of fixed income, such as slipless salaries, access housing financing.

- Structured Government Support: The Government guarantee reduces part of the risk for banks, potentially easing approval pathways for eligible applicants.

- Inclusive of Multiple Income Types: Self-employed, non-fixed-wage, and gig-economy earners are included under the scheme’s parameters.

- Government-Backed Guarantee Support: The presence of a Government-backed guarantee helps participating banks manage part of the financing risk, which may allow eligible applications to be assessed more flexibly, while still following standard credit and affordability checks.

- Support for First-Time and Transitioning Homebuyers: SJKP Madani may be relevant for first-time buyers and households transitioning into formal homeownership, particularly those without an extensive credit history or long-term salaried employment background.

However, it is essential to remember that loan approval is still subject to the participating bank’s internal credit and affordability assessment.

Is SJKP Madani Suitable For Your Homeownership Plans?

SJKP Madani continues to serve as a structured government-backed support mechanism in 2026 for Malaysians seeking home financing, especially those with diverse income profiles. By combining a government guarantee with bank-led assessments, it broadens access to funding while maintaining responsible lending practices.

For eligible buyers, SJKP Madani may represent an additional pathway to homeownership, but careful assessment of personal affordability, documentation readiness, and bank-specific terms remains crucial before applying.

Ready to explore your options? Browse residential properties for sale in Malaysia and identify homes that may align with your financing plans and homeownership goals.