Selling property in Malaysia in 2026 involves more than finding a buyer. This guide covers pricing, documents, legal transfer, RPGT, loan redemption, agent fees, and post-sale steps so you can avoid delays, stay compliant, and protect your final proceeds.

Selling property in Malaysia is not as simple as handing over the keys; it involves legal, financial, and administrative steps.

For sellers in 2026, understanding the up-to-date tax obligations, documentation, and regulatory requirements is critical to avoid surprises and maximise returns.

This guide covers how to sell house in Malaysia, from pricing and valuation to legal conveyancing, Real Property Gains Tax (RPGT), stamp duty, and post-sale matters.

While it reflects the current rules, remember that tax and duty frameworks can change, so always verify with official sources or a qualified adviser before proceeding.

Setting the Stage for a Successful Sale

Proper preparation not only expedites the transaction but also strengthens your position in negotiations with buyers.

Before you list your property or entertain offers, it’s essential to get the groundwork right:

Clear Outstanding Liabilities

- Pay all quit-rent, assessment taxes, and any maintenance/sinking-fund dues.

- For strata properties, obtain the latest maintenance statement and a certificate confirming there are no outstanding arrears; buyers will request these.

- For mortgaged properties, request a redemption statement from your bank, showing the outstanding loan balance.

Confirm Legal Title

- Check whether your property has a strata title, individual title, or master title.

- Determine whether it is freehold or leasehold; for leasehold, transferring title often requires state consent.

- Ensure you have a clean, certified copy of your title deed to avoid delays during transfer.

By getting these fundamentals in order early on, you’ll avoid unnecessary delays and set the stage for a smoother, more confident sales process.

How to Price Your Home for Maximum Impact?

Before listing your property, it’s essential to establish a clear valuation strategy that aligns with both market realities and your selling objectives:

Engage a Qualified Valuer

- Hire a valuer registered with the Board of Valuers, Appraisers and Estate Agents Malaysia (BOVAEA).

- The valuer will analyse comparable recent transactions, location, age, floor, and amenities to produce a valuation report.

Determine Your Asking Price

- Use the valuer’s report and comparable sales (“comps”) from property portals or transaction databases to set a competitive yet realistic price.

- Decide on your strategy: do you prioritise a quick sale (set below market) or are you willing to wait for a premium buyer?

- Leave room for negotiation; many buyers will request a 5-10% discount from your initial asking price.

By setting your price on solid valuation grounds, you create a stronger foundation for negotiations and improve your chances of securing the right buyer at the right time.

Preparing the Property for Viewings

Creating the right impression begins long before a prospective buyer steps through the door.

Thoughtful preparation can significantly influence how buyers perceive your property and, ultimately, how confident they feel about making an offer.

1. Staging Matters

A well-presented home communicates care, cleanliness, and good maintenance. Simple improvements go a long way:

- Apply a fresh coat of neutral-coloured paint to brighten spaces and make rooms feel larger.

- Clean floors, refresh grout, and ensure surfaces are clutter-free.

- Use minimal, neutral décor to help buyers visualise their own lifestyle within the space.

2. Optimise Lighting

Good lighting enhances ambience and helps buyers connect with the home.

- Maximise natural light by drawing curtains and cleaning windows.

- Supplement darker corners with warm but bright artificial lighting to create a welcoming, cohesive atmosphere.

3. Enhance Outdoor Appeal (for Landed Homes)

First impressions begin at the gate.

- Trim hedges, sweep pathways, and tidy the garden.

- Ensure the façade, porch, and entrance areas are clean and well-maintained, as curb appeal can strongly influence a buyer’s initial judgment.

4. Provide Supportive Documentation

Serious buyers appreciate transparency.

- Prepare copies of utility bills, maintenance statements, and evidence of recent repairs or servicing.

- These documents help demonstrate responsible ownership and reassure buyers about ongoing costs and upkeep.

Thoughtful preparation not only elevates your property’s appeal but also positions it favourably in a competitive market, helping you attract committed buyers with greater confidence.

What to Prepare Before the Sale Process Begins

To avoid delays, have the following ready before listing:

| Document | Purpose/Use |

| Title deed/strata title | Proof of ownership |

| Redemption statement | To pay off any existing mortgage at the sale |

| Identification (MyKad/passport) | Needed for legal and conveyancing documentation |

| Past utility, quit rent, assessment, and maintenance receipts | Demonstrates upkeep and has no outstanding liabilities |

| Valuation report | Supports your asking price and helps buyer confidence |

A complete, well-organised document set signals professionalism and helps pave the way for a confident, hassle-free sale.

Hiring an Agent Who Can Actually Deliver Results

Engaging a professional real estate agent can make the selling process significantly smoother, but choosing the right one is crucial.

Here’s what to consider:

- Verify Credentials: Ensure the agent is correctly registered with the relevant state or national real estate board. This guarantees they are legally and ethically licensed to handle property transactions.

- Local Expertise: Select an agent who has demonstrable experience in your specific locality. Familiarity with the neighbourhood allows them to position your property accurately, target the right buyers, and provide insights on local market trends.

- Property-Type Experience: Different property types, such as landed homes, condominiums, or strata units, require distinct marketing and sales approaches. Choose an agent experienced in selling your property type for optimal results.

- Track Record & References: Ask for evidence of their past sales, including average time-to-market and successful transactions. Request client references to verify their professionalism, negotiation skills, and ability to close deals efficiently.

- Commission & Terms: Clearly and formally negotiate the agent’s commission. While 2-3% is typical for most residential transactions in Malaysia, the contract should explicitly specify the agreed percentage, payment terms, and any additional fees to ensure compliance with regulatory standards.

- Marketing Approach: Discuss their strategy for showcasing your property, including professional photography, portal listings, staging advice, and open houses.

Choosing the right agent not only streamlines the selling process but also maximises your property’s visibility, buyer interest, and ultimately, its market value.

Marketing & Buyer Sourcing

To effectively attract potential buyers and streamline the selling process, focus on the following key marketing and buyer-sourcing strategies:

- List on Popular Portals: Use major property websites with high-resolution photos taken in optimal lighting to showcase your property.

- Offer Virtual Tours: Let buyers explore the layout remotely; it’s increasingly valued and helps pre-qualify serious enquiries.

- Hold Open Houses or Private Viewings: Schedule appointments and ensure your agent has all necessary documents on hand for transparency.

- Be Transparent About Issues: Disclose minor defects or maintenance matters upfront to build trust and reduce the risk of deal breakdowns.

A well-planned marketing approach ensures your property reaches the right buyers quickly and builds confidence throughout the sale process.

Handling Offers & Letter of Intent (LOI)

Before finalising a sale, it’s essential to manage buyer interest professionally and ensure all offers are properly documented:

- Request written Offers to Purchase (or Letters of Intent) from interested buyers.

- Typical earnest deposit in Malaysia is 1-3% of the asking price, depending on local practice and negotiation.

- Negotiate: deposit amount, time frame, whether the buyer is cash or financing, and what stays (furniture/fixtures).

- Once an offer is accepted in principle, both parties should instruct their lawyers.

Properly handling offers and Letters of Intent sets a clear foundation for smooth legal processing and reduces the risk of misunderstandings later in the transaction.

Legal Conveyancing & Transfer of Ownership

Selling a property in Malaysia involves a series of legal, financial, and administrative steps that must be carefully coordinated to ensure a smooth transaction.

From preparing the Sales and Purchase Agreement (SPA) to handling stamp duty, understanding each stage is essential for both efficiency and compliance.

Here’s a detailed guide on the process as of 2026:

1. Preparing the Sales and Purchase Agreement (SPA)

Before a property can officially change hands, the Sales and Purchase Agreement (SPA) must be carefully prepared to outline all terms and protect both parties:

- Engage a qualified solicitor or conveyancer to draft the SPA, which should clearly outline the purchase price, deposit, handover date, and any special conditions.

- Check if your property requires management or developer consent, particularly for master-title schemes or older strata developments.

- For leasehold properties, your lawyer must apply for state authority approval to transfer the title, as delays are common if this is overlooked.

- Agree on legal fees in writing. Costs are determined by the Solicitors’ Remuneration Order, which specifies tiered rates rather than a flat percentage.

2. Buyer Financing and Bank Processes

Once the SPA is in place, understanding how buyer financing and bank procedures work is crucial to ensure funds are properly disbursed and all parties are protected:

- If the buyer is securing a loan, their bank will usually appoint a panel valuer to verify the property’s market value.

- Upon loan approval, the bank disburses funds: first to redeem your existing mortgage (if any), then the remaining balance to you or your solicitor, as stipulated in the SPA.

- Factor in potential fees, including bank administration, redemption charges, or early repayment penalties, as these affect your net proceeds.

3. Signing the SPA and Receiving Payment

With financing secured, the next step is the formal signing of the SPA and the transfer of initial payments, marking a key milestone in the transaction:

- Both parties sign the SPA once all conditions are met.

- The buyer pays the down payment, minus any previously paid earnest deposit, at this stage.

- Your lawyer ensures the redemption of any existing mortgage and coordinates the disbursement of funds.

- After the bank disburses the remaining loan, the balance is transferred, and the property can be scheduled for handover.

4. Transfer of Ownership

After the SPA is signed and payments arranged, the legal ownership of the property must be formally transferred, requiring documentation and regulatory approvals:

- Your lawyer prepares and lodges the Memorandum of Transfer (MOT) or Deed of Assignment (DOA) with the relevant Land Office.

- Leasehold properties require state authority approval before registration.

- For master-title or strata developments, ensure management or developer consent is obtained early to prevent delays.

- Stamp duty on the MOT must be paid before the transfer can be officially recorded.

- Once stamped, the documents are registered, and ownership formally passes to the buyer.

5. Stamp Duty on Property Transfer (MOT)

No property transfer is complete without the correct stamp duty being paid, a legal requirement that finalises the change of ownership and ensures compliance with Malaysian tax regulations.

Malaysian citizens and permanent residents pay ad valorem stamp duty as follows:

- First RM 100,000: 1%

- RM 100,001-RM 500,000: 2%

- RM 500,001-RM 1,000,000: 3%

- Above RM 1,000,000: 4%

- Under Budget 2026, a proposal exists to impose a flat 4-8% duty on residential property transfers for non-citizens or foreign companies from 1 January 2026.

- Rates and exemptions may change, so always verify the latest updates from the LHDN or Stamp Office before completing a sale.

Understanding each step, from SPA preparation to stamp duty, is crucial for a smooth, legally compliant property sale.

Proper planning and coordination with your lawyer, buyer, and bank minimises delays and helps secure a successful transaction.

Calculate your instalments before choosing a property.RPGT Explained: Rates, Exemptions & What It Means for You

To understand your actual net proceeds from a sale, it is essential to know how Real Property Gains Tax (RPGT) works and your obligations under Malaysia’s updated self-assessment system.

- RPGT is charged on gains from the disposal of property under the Real Property Gains Tax Act 1976 (RPGTA).

- Since 1 January 2025, Malaysia has used a Self-Assessment System (STS): you, as the disposer, must compute gains, submit the RPGT return (Form CKHT) within 60 days of disposal, and pay the tax.

- Current RPGT Rates for individual Malaysian citizens/permanent residents (Part I, Schedule 5) as of late 2025:

| Holding Period | RPGT Rate |

| Within 1-2 years | 30% |

| 3rd year | 30% |

| 4th year | 20% |

| 5th year | 15% |

| 6th year & beyond | 0% |

Key Exemptions & Reliefs:

- Lifetime private residence exemption: If the property is your primary home, you may elect a once-in-a-lifetime RPGT exemption on the gain, subject to conditions (citizens/PR, building used as residence).

- Partial disposal exemption: If only part of your ownership share is sold, a partial relief may apply (10% of gain or RM 10,000, whichever is greater) under Schedule 4, Paragraph 2.

Important disclaimers:

- These rates and exemptions apply as of late 2025. They could change if the 2026 Budget proposes amendments.

- Because RPGT is now self-assessed, it is crucial to consult the latest HASiL (LHDN) guidance, use their approved forms, and, if needed, engage a tax professional to avoid under- or over-payment.

Navigating RPGT may seem technical, but with the correct information and timely filings, you can ensure full compliance while maximising the returns from your property sale.

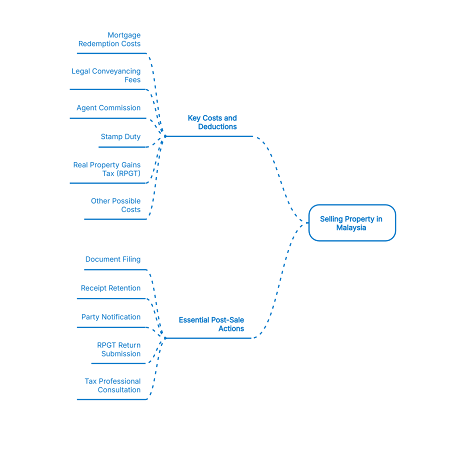

Seller’s Costs, Deductions & Post-Sale Actions

Selling a property in Malaysia involves more than securing a buyer and signing the agreement; there are several costs, administrative steps, and compliance obligations that every seller must plan for.

The following breakdown brings together all key financial considerations and post-completion tasks to help you manage your sale with clarity and confidence.

Key Costs and Deductions to Account For:

Before estimating your net proceeds, it helps to understand the main costs that typically arise during a property sale in Malaysia.

Below are the key items most sellers should factor in:

1. Mortgage Redemption Costs

- Your bank will issue a redemption statement showing the outstanding loan balance.

- If your mortgage package includes an early repayment penalty, it will be charged in accordance with your loan agreement.

- There may also be administrative or valuation fees involved in the redemption process.

2. Legal Conveyancing Fees

- Professional fees are calculated under the Solicitors’ Remuneration Order (SRO), which uses tiered rates rather than a flat percentage.

- Expect additional disbursements, including land searches, photocopying charges, Land Office fees, and other administrative costs.

3. Agent Commission

- Commission is regulated and must be agreed to in writing with your agent.

- While 2-3% is standard, the final rate may vary based on market conditions, service scope, and negotiated terms.

4. Stamp Duty

- Stamp duty on the Memorandum of Transfer (MOT) is payable according to the official rate bands outlined earlier.

- If the buyer is a foreign individual or entity, Budget 2026 proposes a higher flat rate from 1 January 2026; sellers should be mindful of this when estimating net proceeds.

5. Real Property Gains Tax (RPGT)

- RPGT may apply, depending on your holding period and the realised gain.

- Since Malaysia now uses a Self-Assessment System, incorrect or late filing of Form CKHT can result in penalties.

6. Other Possible Costs

- For strata properties, ensure all maintenance fees, sinking fund contributions, and outstanding charges are settled before completion.

- Any renovation or staging expenses undertaken to improve marketability.

- Miscellaneous documentation fees, such as certified true copies or management office consent letters.

Essential Post-Sale Actions

Once the sale is complete and funds have been fully disbursed, a few final administrative steps help ensure a clean handover and proper record keeping:

- Keep securely filed copies of the stamped MOT/DOA and all key sale documents.

- Retain receipts for legal fees, agent’s commission, disbursements, RPGT payments, and any other transaction-related costs.

- Notify all relevant parties, including your bank (upon loan redemption), strata management, utility providers, and service companies, so that accounts can be updated or closed.

- Submit your RPGT return (Form CKHT) within the mandatory 60-day window under the self-assessment framework.

- If you applied the lifetime exemption or made a partial disposal, consider consulting a tax professional to ensure full compliance with HASiL requirements.

By planning for these costs and keeping your post-sale obligations organised, you can complete your transaction smoothly and safeguard your financial and legal position long after the property is sold.

Selling Smarter: Tips Every Owner Should Know

Before you progress to listing or negotiating, it helps to be aware of the common missteps that trip up many sellers, and the practical habits that can keep your sale running smoothly.

- Don’t rely on outdated tax guides: always check the latest LHDN/Stamp Office circulars.

- Budget for all costs, not just agent commission or legal fees: redemption, staging, and compliance add up.

- Be realistic on pricing: overpricing often leads to slow sales and can erode buyer trust.

- Use a reliable, experienced agent: their local insight, negotiation skills, and track record matter.

- Engage a good lawyer early, especially for leasehold or strata properties that require multiple consents.

- File your RPGT properly: missing the form or miscalculating can lead to fines or excessive retention.

By keeping these pointers in mind, you place yourself in a far stronger position to navigate the selling process with confidence, clarity, and fewer unwelcome surprises.

What to Expect When Selling Property in 2026?

As of late 2025, selling property in Malaysia remains complex, involving multiple stakeholders, legal requirements, and tax considerations.

For sellers in 2026, preparing carefully, from valuation to consent, from documentation to tax filing. It is more important than ever, especially for those wanting to understand how to sell a house in Malaysia with full compliance and confidence.

This guide provides a realistic, up-to-date roadmap under the current legal and tax framework.

But keep in mind: tax laws and stamp duty regulations can change with new Budgets, so always double-check with official sources or qualified professionals at the time of sale.

Start with iProperty Malaysia’s latest sales listings to uncover floor plans, pricing details, and the newest developer offerings.