| Monthly Cash Flow = Rental Rate – [Monthly Fees (Home Loan Installment + Maintenance Cost)] – [Lump-sum Fees/12 months (Sewage Charge + Assessment Tax + Quit Rent + Insurance)] |

This guide details how you should conduct your due diligence and includes tips on cash flow management and investment opportunities.

READ AN UPDATED VERSION HERE: Property investment in Malaysia and everything you need to know

First of all, should you invest in property in 2022?

There are various investment vehicles out there – individual stocks, mutual funds, Index Funds or Exchange Traded Funds (ETFs), bonds, and stocks. However, these have been impacted by rising inflation, higher interest rates, and supply chain disruption caused by the zero-COVID strategy in China, as well as Russia’s invasion of Ukraine.

Enter real estate – it is a popular middle option for aspiring investors. Admittedly, the property market has its own fair of challenges (i.e. a residential property overhang). But if you buy the right real estate product which fits your purchasing power and needs, it could provide a healthy return on investment (ROI), either in terms of rental revenue or capital gain. According to the National Property Information Centre (NAPIC), the value of homes continued to appreciate in the past few years – from an average home price of RM417,974 in 2018 to RM432,111 in 2020 and RM434,758 in 2021.

And if nothing else, you will at least get a roof over your head or have a piece of property which you could hand down to your children, so chances of loss is not an option.

Let’s dive into the property investment guide for beginners:

1. Determine how much money you can afford for an investment property

Property investment Malaysia 101: The first step is to determine how much capital you have for property investment. This is important for you to secure a home loan – A true and tested way to determine your purchasing power is via the Debt to Service Ratio (DSR).

DSR = Debt/Net Income (after EPF, SOCSO and Income Tax deductions)

DSR is a measure of your debt against your net income, and the prudent benchmark is that your debt should not exceed 70% of your net income. All the banks in Malaysia use the DSR rule to ascertain if you are able to repay your monthly loan instalments.

A healthy DSR is especially important for those who are not first-time home buyers. Most second-time purchasers obtain a 70-80% home loan – the higher your DSR, the better your chances are at securing a higher margin of financing.

TIP: TIP: In September 2022, Bank Negara Malaysia increased the Overnight Policy Rate (OPR) to 2.25% from 2.50%. The OPR has a domino effect on home loan interest rates, hence you can expect to enjoy cheaper home loans in 2020. However, make sure to shop around and compare rates between banks before settling on a certain loan product, as a lower Base Rate offered by one bank does not necessarily mean that it has the lowest Effective Lending Rate.

2. Decide which property type to invest in

What are the different types of properties available in Malaysia? There is a diverse set of properties to pick from:

Residential property

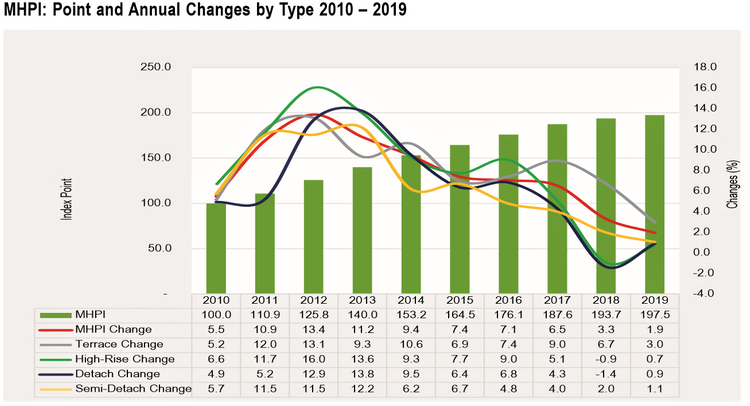

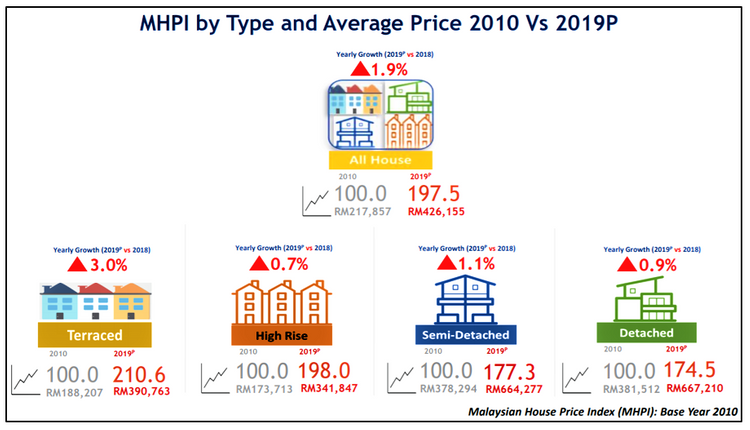

Under this sub-category, the 4 popular options are Terrace house, Semi-Detach House, Detach house (bungalows) and High Rise or strata residential properties such as condominiums, serviced residences and apartments. The chart below by NAPIC provides a picture of how residential property prices have grown over the years:

Malaysia’s average house prices grew by about 0.6% in 2021 compared to the previous year, although there are some difference in the performance per type of homes, and residential property prices can vary significantly across different states and housing suburbs.

To get a better idea of current sub-sale property prices, read: How much should your average household income be to afford a home in Klang Valley? and make sure to check out the Top 10 most searched areas by Malaysian homebuyers in 2019.

Commercial property

Commercial units such as shop lots and office lots require a much bigger downpayment as these units are usually priced over RM1 million. Should you have the cash capacity, commercial real estate can prove lucrative as the tenancy period tend to be longer – businesses set up in a certain location does not change their address frequently. If you are lucky and manage to secure a blue-chip tenant such as a bank, you won’t have to worry about your monthly cash flow for the next decade or so! Moreover, if you decide to start your own business in the future, you will have a ready place to begin your business operations.

Nevertheless, those with a smaller budget can consider investing in Small-office, Flexible-office (SoFos) or Small-office Versatile-office (SoVos). These commercial units provide a lower entry point from as low as RM300,000 – RM400,000. SoFos and SoVos are usually built within a mixed development near popular business district and are targeted towards individual business owners, small startups, etc.

MORE: 4 types of commercial properties investors can consider

3. Are you planning for short-term investment or long-term investment?

On determining the type of property you have set your eyes on, you should think about your investment strategy.

Though property purchase is considered as a long-term investment, it can be used for a short-term investment yield, think Buy to Sell properties. In such cases, you will be cashing out your money within 2-3 years’ time, sometimes even less.

Meanwhile, in long term investment, your “money” will be tied up for years. Considering you have the holding power to invest your monies for at least 5 years, your property will generate greater capital appreciation over the years as house prices grow substantially.

READ: What is the impact of COVID-19 on Malaysia’s property market?

4. What are the available investment opportunities and ways to make money?

Now, let’s look at the various ways you can make money based on your investment goals:

Buying property for rental return – Long term investment

Renting out your property for income is the default option for most property investors. A rental property is a great start for investment as you can enjoy positive cash flows while leveraging on the potential capital gains/growth from property appreciation – We will touch more on capital growth in the next point.

Given the slowing economy in the past couple of years however, the average rental yield in Malaysia lies somewhere between 2% to 4% for your typical rental property and 5%-8% for more in-demand units. Similar to property prices, rental yields will differ depending on the location of your house, nearby amenities and availability of public transportation.

There is no definite percentage that is considered as a ‘good rental yield’, but the golden rule for investors is to ensure that the rental income received would cover your monthly expense comprising of monthly and lump-sum expense, thus guaranteeing a positive cash flow. Hence a better way to determine if your property is able to generate a sufficient rental return is to ensure that your cash flow is in the black:

For example, say you purchase a serviced apartment costing RM 500,000. You managed to obtain a 80% home loan with a tenure of 30 years, hence your monthly instalment is RM1,360. According to property listings online, your expected rent is RM 2,200 per month. Assuming your maintenance cost is RM350 per month and annual lump sum fees are RM2,500, then:

Monthly Cash Flow = RM 2,200 – [RM1,360 + RM350] – [RM2,500/12] = RM 282

Of course, if the cash flow tabulation shows a negative figure, you should look for alternative investments.

Buy to sell (flip) properties – Short-term investment

Gone were the days of taking advantage of zero-downpayment deals and flipping properties overnight. This was especially rampant during 2012-2014 when the Developer Interest bearing Scheme (DIBS) was allowed – property speculators took advantage of the downpayment being born by the developer and sold off their properties for a big profit once it is completed. Also, now that the Real property Gains Tax (RPGT) has been increased to 5%, you have to be mindful of the additional cost involved when selling off your property.

Nevertheless, property investors should consider auction properties. There are numerous below-market deals in prime locations. These units may be older and are in the low to medium-cost category, but they provide tremendous potential should you put in the time and effort to refurbish and renovate them accordingly to secure a willing buyer. According to a property expert, there are over 2,000 properties going on auction each month!

Alternatively, invest in REIT stocks – Short term & Long term investment

If you are apprehensive of long-term commitments or do not wish to take on all the responsibilities that are associated with being a property owner, then real estate investment trusts (REITs) will suit you.

A REIT is a company that owns or finances income-producing properties. REITs are similar to unit trusts, where investors pool together their money and a manager decides which property to buy and/or sell. Returns are then provided to unitholders in the form of dividend payments from investment income such as rental, through capital appreciation from changes in market value as well as capital gains when a property is sold off at a profit.

Rent is usually the main source of income as a REIT holds many types of commercial real estate such as offices, shopping malls, factories and hotels.

REITs can generate high dividend yields with modest long-term capital appreciation – most of the REITs in Malaysia distributes at least 90% of its current year taxable income in the form of dividends to obtain the 25% income tax exemption. Nevertheless, the quality REIT assets is important, hence investors must do their homework and study factors such as the location and income generation of the REITs’ assets.

TIP: Popular REIT options are KLCC Stapled REIT, IGB REIT, Sunway REIT and Pavilion REIT as their property portfolios include prime shopping centres (Pavilion, KLCC, Mid Valley, etc) which continue to enjoy high tenancy amid a challenging economy.

5. Evaluate your property’s capital gain potential using CAGR

As mentioned above, a good investment property should give you 2 things; a steady rental income or a positive monthly cash flow and solid capital growth over the years. If you are thinking of investing in the subsale property market, this additional step will speed up your due diligence process – Conduct a quick litmus test to compare between a few investment property options using the Compound Annual Growth Rate (CAGR) formula.

CAGR = (Ending Value/Beginning Value)1 /* of years – 1

You can use one of the many free CAGR calculators available online, like this one.

Meanwhile, you can obtain the beginning value for the CAGR calculation for your target property (ies) or residential area (s) by extracting its median price from brickz.my. – this site provides the latest and actual transacted sub-sale property prices across Malaysia. You can filter the pricing data points by area, building type, unit size and specific date ranges.

TIP: Use CAGR to determine whether it is worth exploring the idea of investing in a property in the first place. Just compare the property’s CAGR with that of the typical mortgage interest rate in Malaysia which is 4.5%. This would tell you that a CAGR of at least 5% will put your property in the safe “ballpark” as your investment exceeds or justifies the interest paid on your property loan.

IN-DEPTH: What is capital growth & how to calculate it?

6. Key factors to consider when purchasing a rental property

When purchasing a rental property, it is imperative that you conduct sufficient research beforehand to ascertain that your property will be highly tenantable. The “location, location, location” mantra aside, here are a few core principles that you should be mindful of:

- Start with an area you are familiar with, preferably a location nearby as this facilitates maintenance of property and management of tenants. Research all the properties within the area and keep it under your radar for constant monitoring.

- Find the gap between supply and demand. Properties in areas with robust economic activities will always do well. Is there a hospital nearby? Nurses and doctors prefer to rent a place nearby to minimise their daily commute. Or is there a university/college in the neighbourhood? You can depend on the steady stream of students as your target tenants.

- When buying a landed property, the neighbourhood matters. Your target tenants will be families or young couples, so look for a unit in a friendly and secure neighbourhood with good primary and secondary schools nearby.

- Commute is king in the Klang Valley. Many working professionals these days prefer to ditch their cars and use public transportation to escape the rush hour traffic. Hence, they are more inclined to rent apartments or condominium units within walking distance to public transportation nodes, especially LRT and MRT stations. You can look forward to the upcoming MRT Line 2 and LRT 3; the surrounding areas will be ripe for rental demand.

TIP: Find out as much as possible from real estate agents – such as whether the owner is looking for a quick sale and how long the unit has been on the market. This will give you an upper hand when negotiating the property’s selling price.

7. Take note of the closing costs

In the heat of the moment, you might forget that there are additional costs involved when buying a property in Malaysia. Do not overlook these costs when drawing up your investment budget:

Legal Fees

The legal fee rates in Malaysia are as below:

| PRICE TIER | LEGAL FEE (% of property price) |

| First RM500,000 | 1% |

| Next 500,000 (RM500,001 – RM1 million) | 0.8% |

| Following RM2,000,000 (RM1,000,001 – RM3 million) | 0.7% |

| Next RM2,000,000 (RM3,000,001 – RM5 million) | 0.6% |

| Thereafter (> RM5 million) | 0.5% |

Stamp Duty

| Property Purchase Price | Stamp Duty |

|---|---|

| For the first RM100,000 | 1.00% |

| RM101,000 – RM500,000 | 2.00% |

| RM501,000 – RM1000,000 | 3.00% |

| Above RM1000,000 | 4.00% |

Real Property Gains Tax (RPGT)

If you intend to sell your house in the future, the profit made from the sale will be subjected to Real Property Gains Tax (RPGT). As announced during Budget 2022, those who sell off their property in the sixth (and subsequent) years of ownership will now have to pay RPGT.

| RPGT Rates | Individuals (Citizens & Permanent Residents) | Individuals (Non-citizens & foreigners) | Companies |

| Disposal in 1st year | 30% | 30% | 30% |

| Disposal in 2nd year | 30% | 30% | 30% |

| Disposal in 3rd year | 30% | 30% | 30% |

| Disposal in 4th year | 20% | 30% | 20% |

| Disposal in 5th year | 15% | 30% | 15% |

| Disposal in 6th year and beyond | 0% | 10% | 10% |

Property valuation costs

The valuation fee is calculated as a percentage of the purchase price:

For the first RM100,000 =0.25%

Next residue up to RM2 million = 0.2%

Other miscellaneous costs include real estate agent fees, renovation costs and home insurance. For the former, you can opt between MRTA, MLTA and Term Insurance.

Lastly, some departing tips! As with any venture which involves money, knowledge is power. Study market trends, educate yourself on the basics of real estate and keep abreast on the going-ons of our country’s economic and political landscape.

If you enjoyed this guide, read this next: Freehold, leasehold and Bumi Lot: The differences and limitations of each land title

Edited by G.Zizan

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.