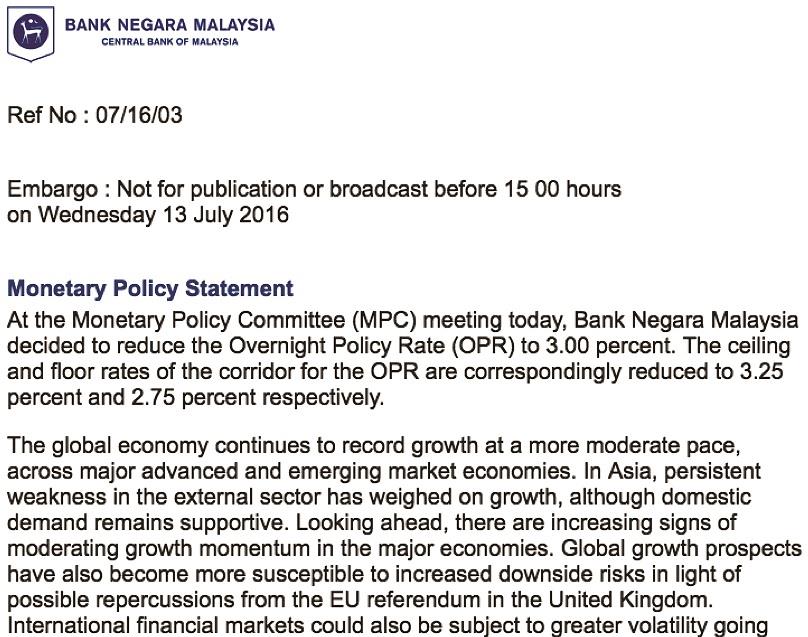

On 13th July 2016, Bank Negara Malaysia (BNM) announced a 25 basis point drop in the overnight policy rate (OPR) in their bi-monthly Monetary Policy Meeting. Most analysts were of the opinion that the OPR should be increased because of the impending uptrend of interest rates in the USA.

On 22 January 2020, Bank Negara Malaysia announced that the Overnight Policy Rate (OPR) is cut by another 25 basis points to 2.75% – the lowest OPR since 2011. Read the updated article here: BNM reduces OPR to 2.75% – How will it affect your home loan?

On 22 January 2020, Bank Negara Malaysia announced that the Overnight Policy Rate (OPR) is cut by another 25 basis points to 2.75% – the lowest OPR since 2011. Read the updated article here: BNM reduces OPR to 2.75% – How will it affect your home loan?

On the other hand, earlier this year, I had predicted that the OPR will see a reduction somewhere in Q3 or Q4 2016 – and this sentiment had, in fact, materialised.

WHAT IS OPR?

OPR is an interest rate/profit rate at which a bank lends to/receives from an investment with another bank. OPR is determined by Bank Negara Malaysia in the Monetary Policy Committee Meeting held throughout the year. In Malaysia, changes in the OPR trigger a chain of events that affect the base rate (BR), base lending rate (BLR), short-term interest rates, fixed deposit rate, foreign exchange rates, long-term interest rates, the amount of money and credit, and, ultimately, a range of economic variables, including employment, output, and prices of goods and services, which are micro and macroeconomic factors.

OPR has been trending at as low as 2% during the global financial crisis in 2009 and as high as at 3.5% in 2006-2008. Shown below is the OPR trend for the past 10 years. Does this spark the start of lower interest rates era or is it just merely a one-off change?

What are the resulting impacts of the OPR drop?

1. It has a direct influence on Base Rate (BR) & Base Lending Rate (BLR). When OPR is reduced, it is stated in the Reference Rate Framework that BR & BLR has to reduce in tandem in view of the OPR changes. This means a reduction of OPR will directly reduce our effective lending rate (ELR) on existing loans that are using this floating rate. In other words, we now enjoy a cheaper interest rate.

A list of the latest BLR and BR of major banks are shown below:

2. Lowering down the OPR reduces the ELR for existing loans and this means lower instalments. This lower instalment will lead to better affordability to the consumer. In banks, affordability is measured by using debt service ratio (DSR) and DSR will reduce in view of lower interest rate. This means that your affordability level has now increased and the chances of you getting your loan approved are improved!

3. However, this may not be good news for those who are yet to obtain a housing loan to finance their dream home. I foresee most banks will be adjusting their spread with their new BR loan offered to be similar or at the same ELR of 4.40% to 5.10%. This would mean that banks stand to enjoy a better profit margin on their housing loan business.

4. The fixed deposit (FD) rate usually moves according to the OPR and thus, we have since seen a reduction in banks’ FD rates. The lower FD rate may push consumers to look for other alternative investment tools that would give them better returns. A consumer who does not take such action will be impacted by the drop in deposit interest rates. This is in view that the price of goods and services will continue to soar due to inflationary pressures especially when the inflation rate is higher than 3%.

5. A reduction in instalment payments translates to consumers having additional cash on hand every month to spend on their needs and wants. Their spending power will increase and this, in turn, will potentially boost our economy.

6. In most instances, the OPR in other countries is normally used as a monetary policy tool to strengthen a country’s currency value. However, as we are experiencing a drop in OPR, it would weaken Ringgit against other currencies in the world.

Must Bank Reduces My Housing Loan Instalment?

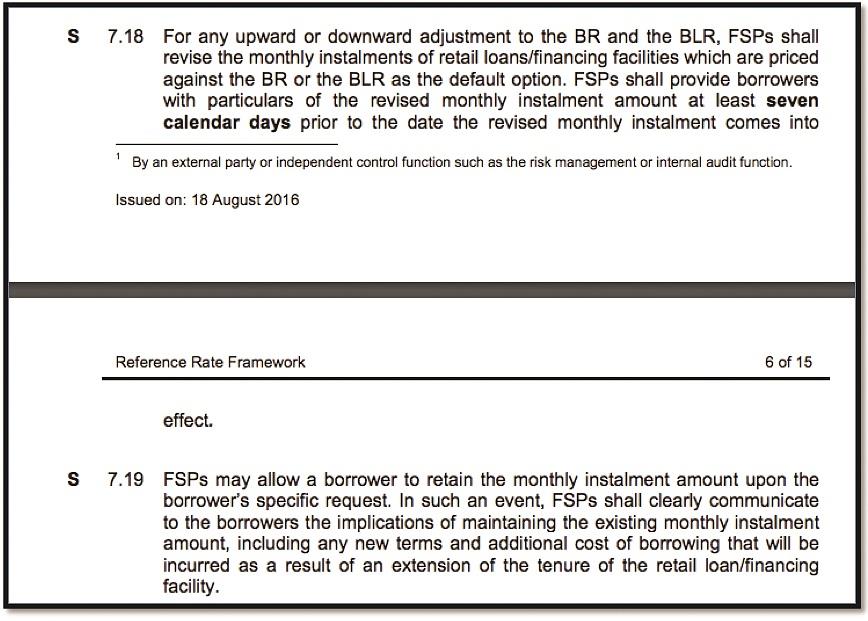

In view of the reduction of BR and BLR by 14bps to 25bps (varies by bank) on the existing floating rate housing loan, all banks are required to make an adjustment to consumers’ monthly instalments, and not make changes to the existing loan tenure instead. This is clearly stipulated in the BNM guidelines as shown in the snapshot below.

Even though by default, banks will be lowering the monthly instalment, they normally will still provide the option for consumers to select to shorten the loan tenure instead.

Conclusion

The OPR reduction is certainly good news for all. Given that an interest rates reduction should weaken our Ringgit, but we experienced otherwise – where the Ringgit rallied against other major currencies right after the OPR reduction is announced. Bursa rebounded from negative territory as well. This shows that the masses are delighted with the change. I foresee that BNM may further adjust the statutory reserve requirement in Q4 2016 and the OPR may very possibly be further reduced in Q1 2017.

This article was first published in the iProperty.com Malaysia October 2016 Magazine. Get your copy from selected news stands or view the magazine online for free at www.iproperty.com.my/magazine. Better yet, order a discounted subscription by putting in your details in the form below!